The Gold Standard: Navigating the New SEC, BSP, and AFASA Reality in the Philippines

--

How Agentic AI is solving the “Triple Squeeze” of 2026’s dual-regulated crypto landscape.

The Philippines has officially graduated from the FATF “Grey List.” For those of us navigating the local fintech ecosystem, this is a moment of pride, but it is also a moment of unprecedented complexity. The “Gold Standard” of regulatory compliance has arrived, and it comes with a heavy operational tax.

In 2026, we find ourselves managing a web of dual sovereignty between the Securities and Exchange Commission (SEC) and the Bangko Sentral ng Pilipinas (BSP). The regulatory bar hasn’t just been raised, it has been completely redesigned. For leadership in the virtual asset and crypto-asset space, the challenge is no longer just “getting licensed.” It is about surviving a “triple squeeze” of overlapping mandates.

1. The Regulatory Siege: Three Fronts, One Mission

Compliance is no longer a back-office checklist. In the current landscape, it is a three-front war where automation is the only viable strategy for retreat-free growth.

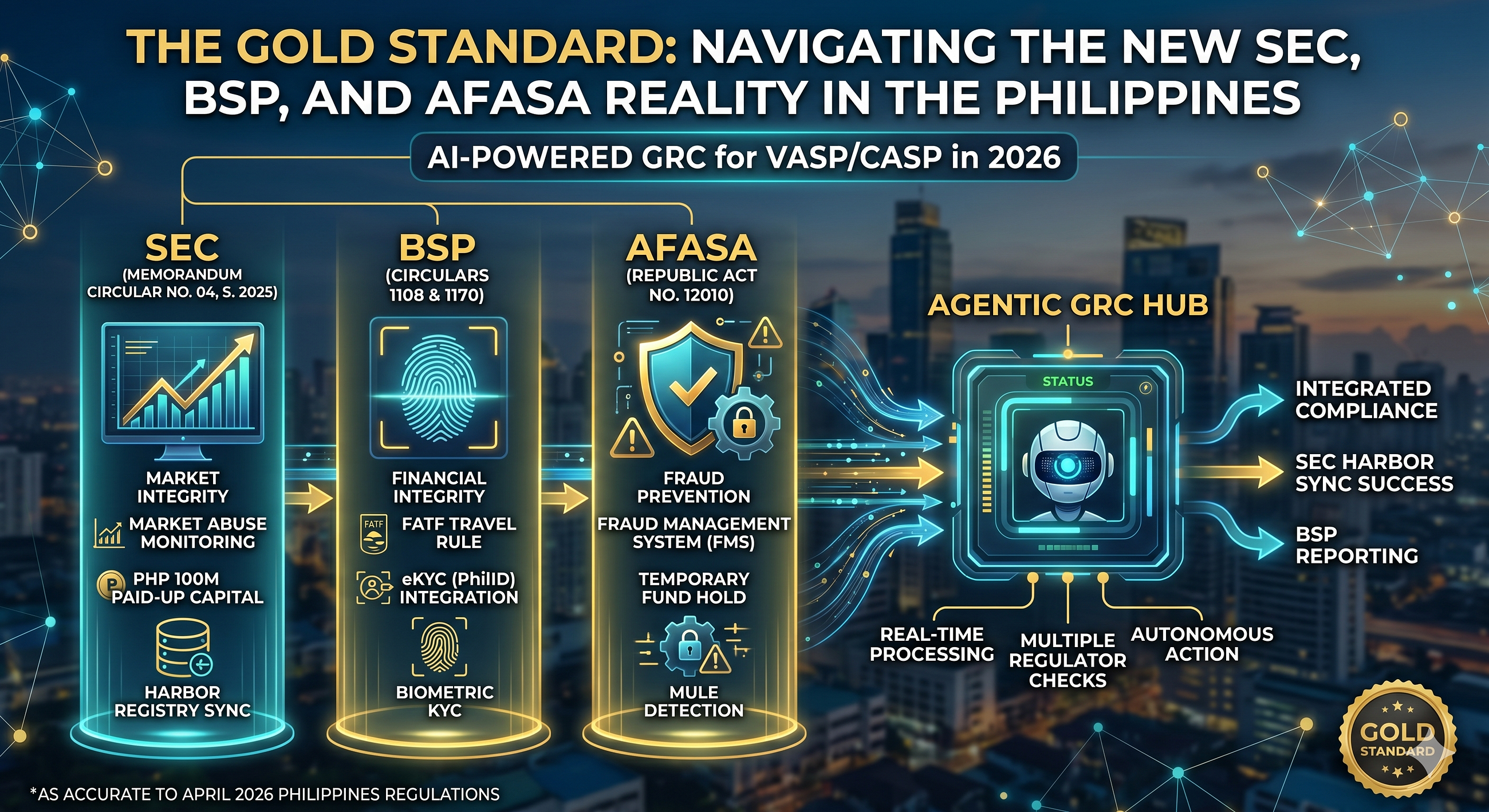

Front 1: The SEC’s Market Integrity Doctrine

With the full implementation of the CASP (Crypto-Asset Service Provider) framework under SEC Memorandum Circular №04 (Series of 2025), the SEC has established a clear barrier to entry: a PHP 100 million minimum paid-up capital requirement.

But the real hurdle isn’t the capital, it’s the transparency. The transition to HARBOR (Hierarchical and Applicable Relations and Beneficial Ownership Registry) is now mandatory. With the beneficial ownership disclosure page officially removed from the physical General Information Sheet (GIS), internal cap tables must be digitally synced with the SEC’s registry. If your data isn’t live, you aren’t compliant.

Front 2: The BSP’s Financial Gatekeeper Role

The Bangko Sentral continues to sharpen its oversight through a dual-lens approach:

- Circular 1108: Remains the bedrock for operations, mandating strict adherence to the FATF Travel Rule and real-time counterparty due diligence.

- Circular 1170: This has revolutionized digital onboarding by establishing the PhilID (PhilSys) as the “Golden Source” for eKYC. While it simplifies identity verification, it demands a tech stack capable of seamless, real-time integration with national systems.

Front 3: The AFASA Shield (RA 12010)

Republic Act №12010, or the Anti-Financial Account Scamming Act (AFASA), is perhaps the most urgent front. It mandates that all financial institutions operate a Fraud Management System (FMS) capable of detecting money muling and social engineering as they happen.

Under AFASA, institutions are authorized and expected to execute a temporary hold on disputed funds. In a market where scams move at the speed of light, a system that isn’t fast enough to flag a “mule” at 3:00 AM creates a massive liability for the institution.

2. The Compliance Tax: Why Manual is Dead

A PHP 100 million capital requirement creates a massive “compliance tax.” Attempting to satisfy the SEC, BSP, and AFASA using traditional, human-heavy GRC (Governance, Risk, and Compliance) teams is a recipe for capital depletion.

In 2026, manual GRC will be:

- Too Slow: AFASA requires instant intervention. Humans take minutes, scams take seconds.

- Too Fragmented: A human officer might check a BSP blacklist but miss an SEC market-abuse flag or a behavioral anomaly.

- Too Expensive: Scaling a 24/7 compliance desk to meet these specific standards is a luxury few can afford while maintaining a healthy bottom line.

3. Weaponizing Agentic AI: The 2026 Competitive Moat

The winners in the Philippine market are shifting from “Generative AI” (writing reports) to “Agentic GRC.” These are AI agents that don’t just alert a human, they take action.

“In 2026, your GRC stack is your tech stack. You can no longer separate compliance from code.”

The Regulatory Translator

Modern firms use NLP-driven agents to map overlapping rules. Instead of three separate audits, an AI “translator” identifies common controls, ensuring that a single verified action satisfies the SEC’s market abuse rules, the BSP’s AML standards, and AFASA’s fraud requirements simultaneously.

The Real-Time Fraud Sentinel

To satisfy AFASA, AI agents monitor behavioral biometrics. If a user’s transaction velocity or device fingerprinting shifts, indicating a potential scam, the AI executes a temporary hold immediately. This fulfills the legal mandate of RA 12010 without the latency of human intervention.

Automated HARBOR Filings

AI agents now sync internal records directly with the SEC’s HARBOR system. This ensures that beneficial ownership data is always live and the digital GIS is filed without the technical rejections that plagued manual entries in 2025.

4. The End of the “Wild West”

The entry of the SEC and the weight of AFASA have created a high barrier to entry, but this is a net positive for the industry. It filters out “fly-by-night” players and protects the Filipino investor.

However, it also signals a fundamental shift in leadership. The “Gold Standard” will not be won by the firm with the most capital but by the firm with the smartest agents. As we move forward, the question for the community remains: Are we seeing the birth of the most secure crypto ecosystem in Southeast Asia, or are we risking “regulation by exhaustion”?