Visa’s stablecoin settlement hits a $4.6B annualized run-rate, reshaping payment rails

This story was published on Sentora Research

Visa’s Q1 FY2026 call added a new data point that matters beyond headlines: stablecoin settlement on Visa reached a $4.6B annualized run-rate, while Bessemer’s latest market map shows real-world stablecoin payments doubled to $400B in 2025.

This issue focuses on what changed in the last seven days, where these numbers sit in the broader payment stack, and what they imply for infrastructure builders, liquidity providers, and treasury operators. The core question is no longer whether stablecoins are useful, but where they can compound fastest relative to incumbent rails.

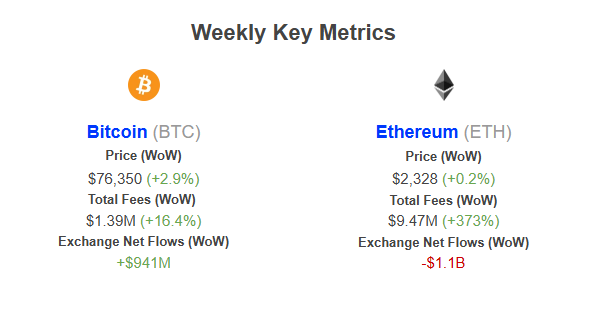

Network Fees:

- Bitcoin: On-chain fees increased by +16.4% to $1.39 million, accompanying a moderate +2.9% price climb to $76,350. This signals a healthy, proportionate uptick in transactional demand supporting the gradual price expansion, without indicating severe network congestion or retail speculative mania.

- Ethereum: In stark contrast, fees skyrocketed by +373% to $9.47 million while the asset’s price remained effectively flat (+0.2%). This explosive surge in blockspace demand is directly attributable to the fallout from the Kelp rsETH hack and Aave’s subsequent market freezes. The exorbitant fees reflect reactive panic unwinding, emergency collateral adjustments, and complex smart contract interactions, temporarily turning mainnet into a highly congested environment dominated by crisis management rather than organic growth.

Exchange Netflows

- BTC: The asset registered +$941 million in net inflows to exchanges. This influx suggests that a cohort of market participants is moving assets onto trading venues to capture liquidity or realize profits amidst the broader market uncertainty and the push past $76k, potentially introducing a short-term supply overhang.

- ETH: Conversely, Ethereum experienced aggressive net outflows totaling -$1.1 billion. Despite the severe DeFi turbulence, or perhaps directly because of it, users are rapidly withdrawing ETH from centralized venues. This massive outflow likely indicates a flight to self-custodial cold storage in response to counterparty and smart contract fears, fundamentally tightening the liquid supply even as on-chain dynamics remain highly stressed.

Stablecoins crossed the enterprise threshold

The weekly signal: Visa moved stablecoins from pilot language to operating language

This week’s most important shift is semantic and operational. On the Q1 FY2026 earnings call, Visa framed stablecoins as a live settlement rail with measurable throughput, not just an innovation initiative. The disclosed annualized run-rate of $4.6B is still small versus Visa’s total network scale, but it confirms a repeatable production flow with institutional counterparties.

Two details in management commentary are especially relevant:

- Geographic expansion: stablecoin card issuance expanded into additional countries, now above 50 markets.

- Treasury utility: USDC settlement capabilities were expanded into the US for banks and fintechs.

- Use-case concentration: Visa explicitly pointed to cross-border, remittances, B2B, and disbursements as the strongest product-market-fit zones.

That set of signals aligns with how payment adoption historically happens: new rails first win where existing systems are slow, expensive, or operationally rigid.

What changed in market structure over the same week

While the Visa disclosure is company-specific, the broader on-chain dollar base remained stable and liquid. Global fiat-backed stablecoin circulating supply closed this week near $319.1B, up about 0.29% over the last 7 days, based on DefiLlama’s daily aggregate series. The week-on-week move is modest, but the absolute base remains near all-time highs and provides the monetary substrate for payment settlement growth.

In practical terms, a flat-to-slightly-rising supply during a strong adoption narrative is constructive. It suggests enterprise usage is increasingly tied to velocity and utility, not only speculative mint cycles.

Why the $4.6B number is important even though it is small

Many readers will correctly note that $4.6B is negligible against Visa’s annual payments volume ($14.2T in FY2025). That framing is mathematically true but strategically incomplete. The early phase of rail shifts tends to start as a thin overlay in underpenetrated corridors and treasury operations, then compound through:

- weekend/holiday settlement availability,

- reduced prefunding burdens,

- faster working-capital turnover,

- and simpler global dollar access in high-volatility FX regions.

Visa itself highlighted these exact mechanics on the call, including 7-day settlement access and improved liquidity timing. Those are not marginal UX gains; they are direct balance-sheet improvements for payment operators.

Bessemer’s $400B figure: crossing from crypto plumbing to enterprise behavior

Bessemer’s report adds the macro lens: real-world stablecoin payments reached $400B in 2025, roughly double prior-year levels, and the majority is estimated to be B2B. That composition matters. Consumer narratives are loud, but enterprise transaction flows are what usually anchor durable payment demand because they are process-driven and recurring.

The implication for DeFi-native participants is straightforward: the growth frontier is less about speculative transfer count and more about operational finance modernization. Stablecoins are increasingly functioning as programmable corporate cash in motion.

Reconciling datasets: $390B vs $400B does not change the conclusion

You will see adjacent figures across research providers. McKinsey + Artemis estimate ~ $390B in 2025 stablecoin payments, with B2B around $226B (~60%) and very high YoY growth (700%+ in their B2B estimate). Bessemer rounds the ecosystem number to $400B and presents a similar directional conclusion.

For strategy, this spread is not material. The central read-through remains:

- payments usage is no longer de minimis;

- B2B has become the primary growth engine;

- and stablecoin adoption is decoupling from pure crypto beta narratives.

Geography and corridor logic now matter more than chain tribalism

Visa’s own commentary emphasized stronger product-market fit in underpenetrated and FX-friction geographies rather than highly digitized domestic card markets. That tracks with what stablecoin adoption has shown repeatedly: usage accelerates where the status quo is expensive, delayed, or operationally brittle.

For analysts, this means corridor-level data is now more informative than generic chain-level throughput:

- settlement frequency by corridor,

- average ticket size by payment type,

- conversion and off-ramp depth,

- and fail/reversal rates in production flows.

The market is entering a phase where operational KPIs beat narrative metrics.

Portfolio and protocol implications for DeFi-native participants

There are three practical implications for DeFi power users over the next 2–4 quarters:

- Stablecoin liquidity quality is becoming a core macro variable. Depth, redemption reliability, and composability across rails matter more than nominal supply growth alone.

- Yield sources should be re-evaluated by payment adjacency. Revenue streams connected to settlement activity, treasury flows, and enterprise-grade transaction services may prove stickier than purely reflexive on-chain demand.

- Interoperability premiums likely rise. Systems that can bridge institutional compliance requirements with multichain liquidity routing should capture disproportionate transaction value.

This does not imply a one-way trade. It implies a shift in what fundamental diligence should prioritize.

Stablecoins are now behaving less like a sidecar to crypto markets and more like an incremental global payments layer entering production at scale. The key takeaway is that enterprise adoption has moved from isolated pilot announcements to measurable throughput across major networks and payment cohorts. Still, execution and policy risk remain high: liquidity fragmentation, compliance bottlenecks, and regulatory divergence can all slow or localize growth.

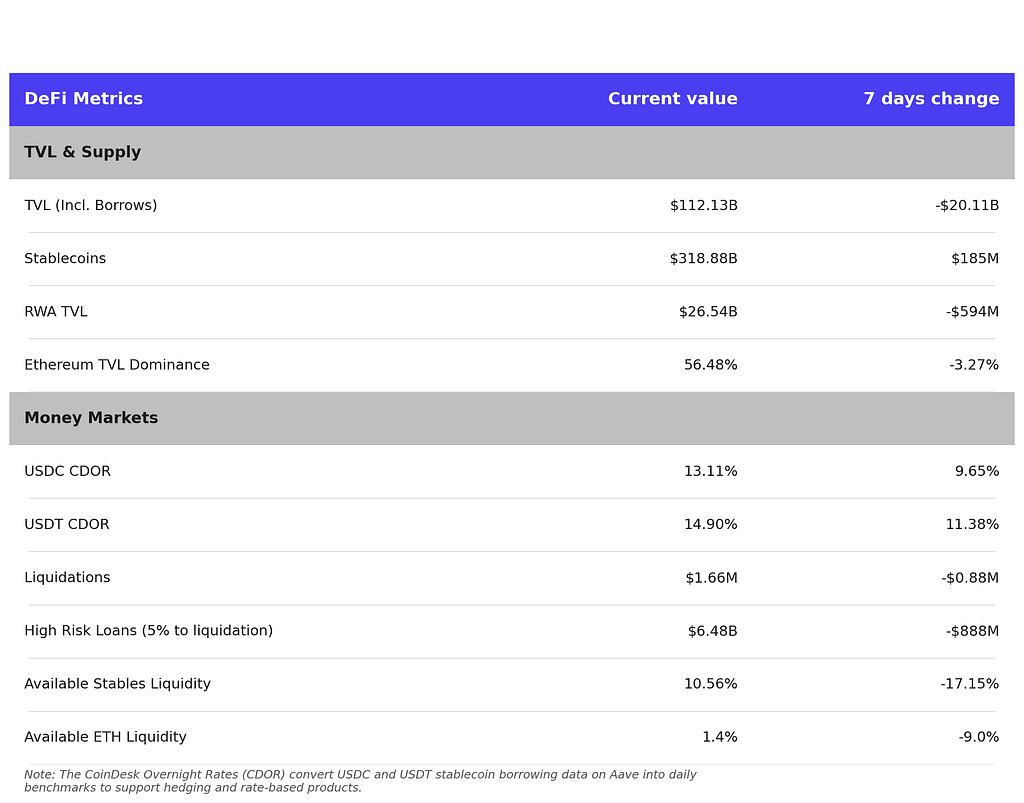

Key Weekly DeFi Metrics

Key takeaways for this week:

- DeFi-wide risk-off: TVL dropped $20B (-15%) and Ethereum dominance fell 3.27pp, as the rsETH exploit caused unwinds and derisking to avoid contagion effects.

- Lending markets drained: ETH liquidity crashed to 1.4%, stables to 10.56%, and CDOR spiked from 3.4% to 13–15% as loopers exited.

Why Lending is Moving Away From Shared Pools

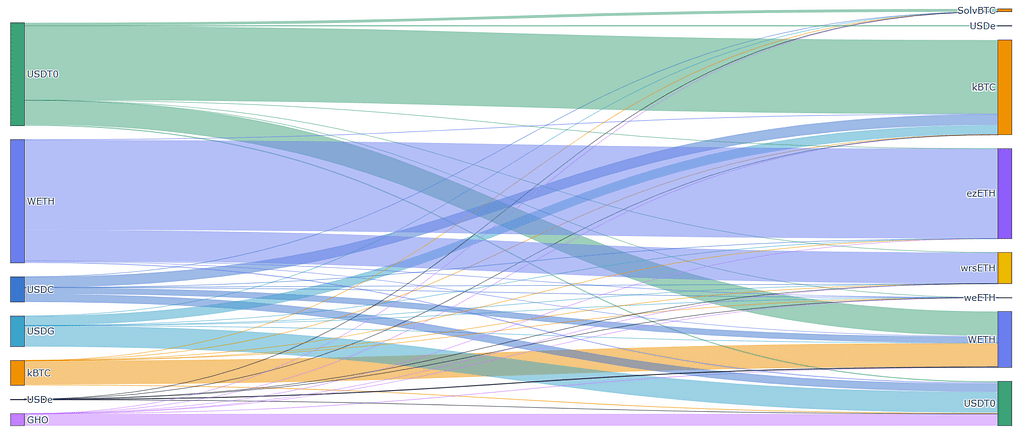

Lending market design has been shifting away from shared pools toward isolated markets and vaults for several years. Morpho’s isolated markets, Aave’s e-mode and isolated asset modes, and Euler V2’s vault architecture all point in the same direction: pricing and containing risk asset-by-asset rather than socializing it across a single liability pool. The shift is a response to how collateral composition and composability have evolved, not a reaction to any single exploit.

The shared-pool structure shown above illustrates the scaling problem. A broad set of base assets routes into an almost equally broad set of yield-bearing derivatives, with flows crossing between counterparties multiple times before reaching a terminal collateral. Every asset accepted into the pool widens the shared risk surface for every lender and borrower already inside it. Recent incidents involving KelpDAO rsETH and Resolv USR have shown that exploits now propagate past the originating protocol through wrapped, restaked, and synthetic representations that already sit inside lending markets as accepted collateral.

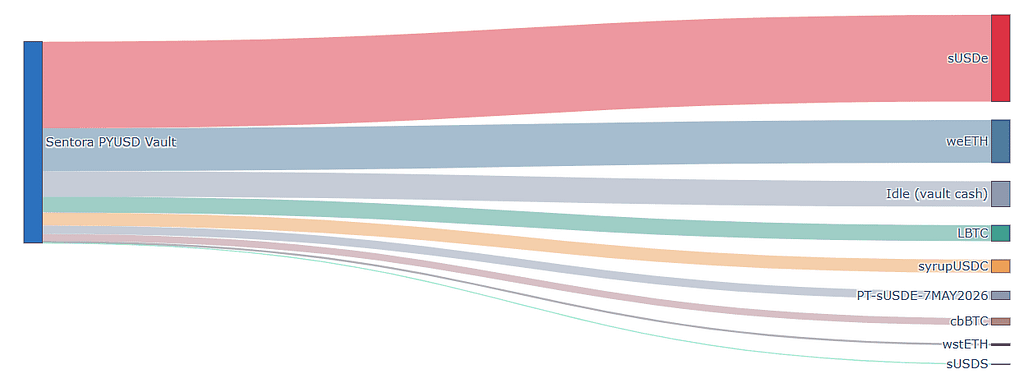

The isolated-vault structure shown above presents a different surface. A single vault allocates into a discrete, curator-defined set of roughly nine exposures spanning stablecoin derivatives, liquid staking tokens, wrapped BTC, a fixed-rate principal token, and idle cash, with each exposure ring-fenced from the others. That scope allows per-asset monitoring, contagion tracking bounded by the vault’s own positions, and controls such as circuit breakers on specific legs when upstream issuers behave unexpectedly. As backing reserves grow more heterogeneous in composition and in location, spanning on-chain instruments and off-chain custodied assets, and as access-control designs diverge across issuers, curators need this kind of isolation to monitor exposures with any precision.

The implication for institutions is that heterogeneous risk mandates across distribution channels can be expressed directly in vault parameters, rather than compromising against a shared pool’s lowest common denominator. For on-chain users, the apparent fragmentation is addressable at the allocation layer: meta-vaults and allocator contracts can route deposits across multiple isolated markets while preserving a single user-facing deposit surface. The direction of travel is toward more choice, more explicit curation, and clearer segmentation of where risk sits and who is monitoring it.

Real-world stablecoin payments double to $400B in 2025 was originally published in Sentora on Medium, where people are continuing the conversation by highlighting and responding to this story.