I Coded 3 Famous Trading Strategies in Pine Script and Backtested All of Them. None Passed.

--

EMA crossover, RSI mean reversion, Bollinger squeeze. Every beginner learns these. I put all three in the Strategy Tester on the same asset, same window. Here are the results — and why each one fails differently.

BTCUSDT Daily · Jan 1, 2025 → Mar 29, 2026 · $10,000 starting capital · 0.1% commission · All three strategies tested identically

There are three strategies that appear in almost every beginner Pine Script tutorial. The EMA crossover. RSI mean reversion. The Bollinger Band squeeze breakout. They are taught as foundational concepts — the building blocks you graduate from once you understand the basics.

I wanted to know what happens when you actually run them. Not on a cherry-picked chart with arrows drawn after the fact. In Strategy Tester, with commission, on the same asset and the same window, with the full results visible.

I coded all three from scratch and ran them on BTCUSDT daily from January 2025 to March 2026. None of them made money. But they failed in three completely different ways — and understanding why each one fails is more useful than any of the strategies themselves.

Strategy 1: EMA Crossover 9/21

Strategy 01 of 03 — Trend Following

The EMA crossover is the first strategy most Pine Script tutorials show you. When the fast EMA (9) crosses above the slow EMA (21), go long. When it crosses below, close. The logic is simple: follow the trend, enter when momentum shifts.

//@version=6

strategy("EMA Crossover 9/21",

overlay=true,

initial_capital=10000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=100,

commission_type=strategy.commission.percent,

commission_value=0.1)emaFast = ta.ema(close, 9)

emaSlow = ta.ema(close, 21)bullCross = ta.crossover(emaFast, emaSlow)

bearCross = ta.crossunder(emaFast, emaSlow)if bullCross

strategy.entry("Long", strategy.long)

if bearCross

strategy.close("Long")plot(emaFast, "EMA 9", color=color.orange, linewidth=1)

plot(emaSlow, "EMA 21", color=color.blue, linewidth=2)

plotshape(bullCross, style=shape.triangleup,

location=location.belowbar, color=color.green, size=size.small)

plotshape(bearCross, style=shape.triangledown,

location=location.abovebar, color=color.red, size=size.small)

bgcolor(strategy.position_size > 0 ? color.new(color.green, 92) : na)

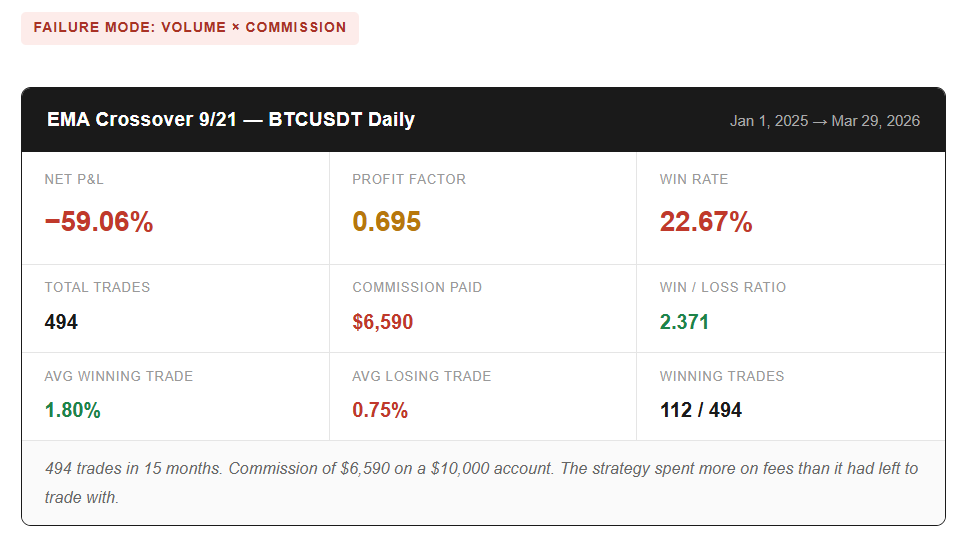

The win/loss ratio of 2.371 is not a broken number — when this strategy wins, it makes more than twice what it loses on average. The problem is 494 trades at 100% position sizing on a daily chart. That is more than one entry per trading day, which means the strategy is catching every EMA wiggle on BTC’s choppy 2025 price action.

Commission at 0.1% per trade on a full-equity position compounds the destruction. By trade 200, the account has been reduced enough that each subsequent trade has less capital to recover with. $6,590 paid in commissions on a $10,000 starting account is not a rounding error — it is 65% of the entire starting capital consumed by fees before any trading loss is calculated.

The EMA crossover isn’t wrong in principle. It is wrong at this frequency, on this asset, at this position size. A slower EMA pair (50/200 instead of 9/21), lower position sizing (25% of equity), and a volatility filter to avoid ranging markets would change this result materially. The concept survives. The default settings do not.

Strategy 2: RSI Mean Reversion (14)

Strategy 02 of 03 — Mean Reversion

RSI mean reversion buys when the market has fallen enough to look oversold and sells when it recovers. RSI below 30 with a 200 MA filter to avoid entering during bear markets. Exit when RSI crosses above 70. Standard setup, used by countless traders.

//@version=6

strategy("RSI Mean Reversion 14",

overlay=false,

initial_capital=10000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=100,

commission_type=strategy.commission.percent,

commission_value=0.1)rsiLen = input.int(14, "RSI Length", minval=2)

oversold = input.int(30, "Oversold", minval=10, maxval=49)

overbought = input.int(70, "Overbought", minval=51, maxval=90)

maLen = input.int(200, "MA Filter", minval=50)rsiVal = ta.rsi(close, rsiLen)

maVal = ta.sma(close, maLen)aboveMa = close > maVal

entrySignal = aboveMa and ta.crossunder(rsiVal, oversold)

exitSignal = ta.crossover(rsiVal, overbought)if entrySignal

strategy.entry("Long", strategy.long)

if exitSignal

strategy.close("Long")hline(overbought, "Overbought", color=color.red, linestyle=hline.style_dashed)

hline(oversold, "Oversold", color=color.green, linestyle=hline.style_dashed)

plot(rsiVal, "RSI", color=color.purple, linewidth=2)

bgcolor(entrySignal ? color.new(color.green, 85) : na)

This result is almost the opposite problem from the EMA crossover. Where Strategy 1 fired 494 times, Strategy 2 fired 17. The 200 MA filter combined with RSI(14) needing to reach 30 on BTC — which spent much of 2025 in a range rather than a clean downtrend — produced an entry signal that almost never triggered.

17 trades is not a backtest. It is a sample so thin that the results — positive or negative — tell you almost nothing about the strategy’s actual edge. Flip a coin 17 times and the result is meaningless as evidence. You need a minimum of 100 trades, ideally more than 200, before the win rate and profit factor carry statistical weight.

The deeper problem is the win/loss ratio of 0.608 — losers are 3.81% on average versus winners at 2.57%. For a mean reversion strategy with no stop loss and a fixed RSI exit at 70, this is structurally inevitable. The strategy holds through drawdowns waiting for RSI to recover, which means losses compound while winners get capped by the exit level. On BTC in a choppy period, those drawdowns are large.

Strategy 3: Bollinger Band Squeeze Breakout

Strategy 03 of 03 — Volatility Breakout

The Bollinger squeeze identifies periods of low volatility compression — when the Bollinger Bands contract inside the Keltner Channels — and enters when the squeeze releases with upward momentum. The theory: compression precedes expansion. Catch the breakout early.

//@version=6

strategy("Bollinger Squeeze Breakout",

overlay=true,

initial_capital=10000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=100,

commission_type=strategy.commission.percent,

commission_value=0.1)bbLen = input.int(20, "BB Length", minval=5)

bbMult = input.float(2.0, "BB Multiplier", minval=0.5, step=0.1)

kcLen = input.int(20, "KC Length", minval=5)

kcMult = input.float(1.5, "KC Multiplier", minval=0.5, step=0.1)

maLen = input.int(200, "Trend Filter", minval=50)basis = ta.sma(close, bbLen)

dev = bbMult * ta.stdev(close, bbLen)

bbUpper = basis + dev

bbLower = basis - devkcBasis = ta.ema(close, kcLen)

kcRange = kcMult * ta.atr(14)

kcUpper = kcBasis + kcRange

kcLower = kcBasis - kcRangesqueeze = bbUpper < kcUpper and bbLower > kcLower

maVal = ta.sma(close, maLen)

aboveMa = close > maVal

momentum = close - ta.sma(close, bbLen)

squeezeRelease = squeeze[1] and not squeeze

entrySignal = squeezeRelease and momentum > 0 and aboveMa

exitSignal = ta.crossunder(close, basis)if entrySignal

strategy.entry("Long", strategy.long)

if exitSignal

strategy.close("Long")plot(basis, "BB Mid", color=color.gray, linewidth=1)

plot(bbUpper, "BB Upper", color=color.blue, linewidth=1)

plot(bbLower, "BB Lower", color=color.blue, linewidth=1)

plotshape(entrySignal, style=shape.triangleup,

location=location.belowbar, color=color.green, size=size.normal)

bgcolor(squeeze ? color.new(color.orange, 88) : na)

bgcolor(strategy.position_size > 0 ? color.new(color.green, 92) : na)

The Bollinger squeeze is the most structurally interesting result of the three. A win/loss ratio of 1.992 — nearly 2:1 — means the exit logic is working. When trades win, they win big relative to what they lose. The trade count of 160 is reasonable for a daily chart. Commission at $2,841 is high but not catastrophic.

The failure is the win rate: 24.38%. Only 39 of 160 squeeze releases produced a profitable long trade. The reason is conceptually simple: volatility squeezes release in both directions. The strategy identifies compression correctly but assumes the breakout will be upward. In a market where BTC spent significant time ranging and reversing in 2025, roughly three out of every four squeezes resolved to the downside or reversed immediately after release.

A long-only squeeze strategy needs a trending bull market to work. In a sustained uptrend, most squeeze releases continue upward because the underlying momentum is already established. In a sideways or oscillating market, squeeze releases are noise — the compressed energy dissipates in whatever direction the latest catalyst pushes price, which is random relative to any directional assumption.

All three side by side

Look at the three failure modes column by column and a pattern emerges:

The EMA crossover has the best win/loss ratio (2.371) but the worst trade count and commission. Too many signals, not enough selectivity. The RSI strategy has the most reasonable win rate (41%) but the worst win/loss ratio and a sample size too small to mean anything. The Bollinger squeeze sits in the middle on most metrics but fails on direction — it finds real compression events and then guesses wrong on direction 75% of the time.

Every strategy has one metric that looks defensible and one that explains why it still loses. That is not a coincidence — it is what you should expect from untested default settings on a single asset in a single market regime.

Three different failures, one shared lesson

The three strategies fail in three different directions. That is the point. There is no universal strategy that survives all market conditions at default settings. The value of backtesting is not finding the one strategy that passes — it is understanding precisely why each one doesn’t.

What “passing” a backtest would actually require

None of these strategies passed. But “passing” is worth defining. A backtest result that earns serious attention has a few minimum requirements: a profit factor above 1.2 (not just above 1.0), a sample size above 100 trades, a win rate and win/loss ratio that compound positively in the math, a max drawdown that a real trader could survive without abandoning the strategy, and results that hold across more than one asset and more than one time window.

None of the three tested here meet all five criteria simultaneously. The EMA crossover has sample size but fails on frequency and profit factor. The RSI strategy fails on sample size fundamentally. The Bollinger squeeze has a reasonable sample and decent win/loss ratio but fails on win rate and single-regime performance.

That is not a verdict against the underlying concepts. EMA crossovers, RSI mean reversion, and volatility squeeze breakouts are all real market phenomena. The strategies coded here are the textbook versions — first implementations, not finished ones. Every parameter choice (9/21, RSI 30/70, 200 MA filter) was made by convention, not by testing what actually works on this asset in this timeframe.

The next step for any of these is not to find a different strategy. It is to understand why each one fails on this specific asset and adjust exactly that variable — position sizing for the EMA crossover, entry frequency for the RSI system, a trend confirmation filter for the squeeze. One change at a time, one variable at a time.

If you want to write and run these strategies yourself, the Pine Script Beginner’s Guide covers the language fundamentals from scratch — syntax, how series data works, variable types, and the beginner mistakes that make strategies silently misbehave. It’s a starting point for writing code, not a trading system. Includes a Bonus ZIP Toolkit of ready-to-use scripts.