Stop living one crisis away from financial stress and start building real security

I used to believe that emergencies were only experienced by other individuals. Car breaks down? Insurance covers it. Unexpected medical bill? I’ll figure it out later. Life was predictable and I thought that my finances were stable to meet whatever comes. Then reality hit.

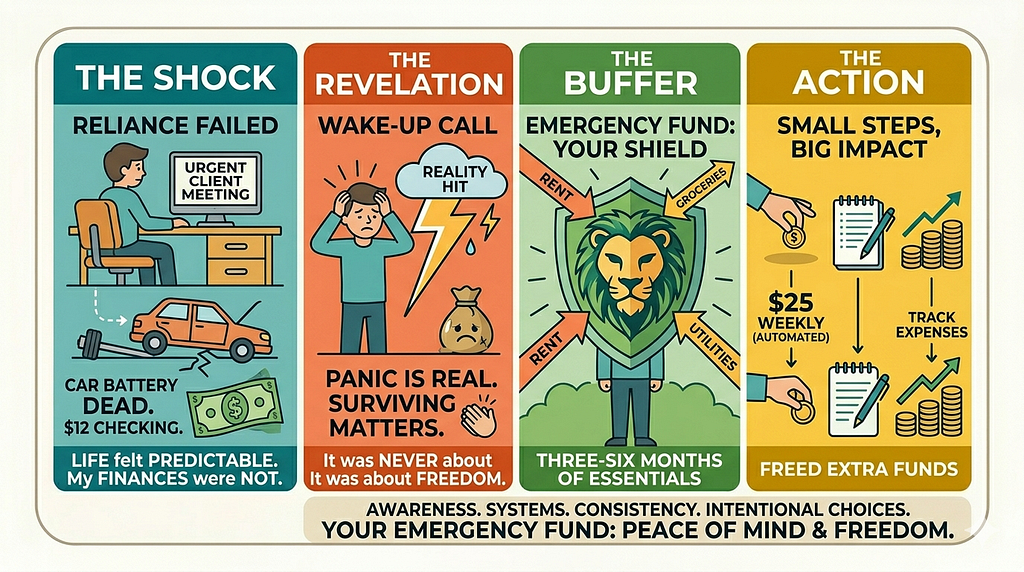

On a Tuesday morning, when I had a big meeting with a client, my car battery failed. My checking balance was 12 dollars, and I did not have any savings. I felt that sinking panic. You know how it feels when you have ever had an emergency involving money, even one of the minor ones. Clap to yourself because you have gotten through it.

The lesson of that time is the need of an emergency fund. I also had heard the word used but dismissed it as something that serious savers or financial planners use. I understood that it was not about luxury, but about freedom, security and peace of mind.

I began with a basic guideline: save three or six months of necessary costs. Rent, groceries, utilities, transportation — everything I would have to maintain my comfort to live. It was not about being perfect it was about forming a buffer that would cushion me against the uncertainties of life.

It was possible because of starting small. I started with $25 a week, and so I had to automate the transfer to ensure that I did not even see the money leaving my account. At first, progress felt slow. The prospect of a small balance in a separate account was not empowering to feel, yet the consistency is what is more important than the speed.

I also identified all the costs to know my base point. Making a list of all the things I bought, including a 3-dollar coffee and a 50-dollar a week groceries, allowed me to realize where my unwanted spending could be reduced. Saving little, insignificant costs released funds, which I could divert towards my emergency fund.

Automation became my secret weapon. Automate savings every payday, even if it’s small. That $25 per week grew without me thinking about it. After a few months, I began to see the balance climb. There’s something incredibly motivating about watching your safety net grow steadily, even in small increments.

Unexpected events kept happening, and I was ready this time. My car repair, a minor medical expense, and a broken laptop all could have been financial disasters, but they weren’t. My emergency fund absorbed the shocks, and I stayed calm. That sense of security is priceless.

I realized that building an emergency fund isn’t just financial; it’s emotional. It reduces stress, increases confidence, and gives me freedom to make choices without panic. I no longer avoid taking risks in life because money is always a looming worry.

I also learned to personalize my emergency fund. What’s essential for me might be different for someone else. I included travel insurance for work trips, car maintenance, and even a small buffer for friends and family emergencies. Tailoring it to my life made it practical,not theoretical.

Mistakes were inevitable. I occasionally dipped into the fund for non-emergency treats, gadgets, or impulse buys. Each time, I reminded myself that discipline matters. Replenishing the fund immediately became a rule, reinforcing the habit and keeping the fund intact.

I discovered that emergencies teach us priorities. When unexpected expenses hit, you quickly realize what matters most. Essentials first, savings second, wants last. This perspective helped me manage both my emergency fund and my regular budget more effectively.

Even modest contributions add up over time. Saving $25 a week might seem trivial, but compounded over months, it becomes significant. The habit of contributing regularly matters more than the initial amount. Consistency beats speed.

I also realized that knowledge compounds like money. Reading about financial planning, insurance, and investment options allowed me to make smarter choices for my fund. Choosing a high-interest account for savings, setting up automatic transfers, and using budgeting apps all amplified the growth of my safety net.

Talking to friends about emergency funds was revealing. Many of them didn’t have one, and the anxiety showed. Sharing my strategy created accountability and sometimes inspired them to start their own fund. If you’ve ever avoided a conversation about money out of fear, clap for yourself — you’re learning.

Tracking progress visually helped keep me motivated. Seeing my emergency fund grow on a chart or app transformed abstract numbers into tangible results. I celebrated milestones, like reaching $500, $1,000, and eventually three months of expenses. These celebrations reinforced the habit.

I discovered the power of discipline over motivation. Motivation ebbs and flows, but discipline keeps you consistent. Automating transfers, tracking expenses, and adhering to my fund rules created a sustainable system that worked even when I wasn’t feeling motivated.

Unexpected financial shocks continued, but each time, my response was calmer. I could pay bills, fix problems, and handle stress without panic. That security isn’t just about money; it’s about reclaiming mental energy and confidence.

Building an emergency fund also reshaped my other financial habits. I began saving more, investing more confidently, and budgeting more realistically. With a solid safety net, I wasn’t afraid to take calculated risks or explore opportunities I might have avoided before.

I realized that this fund was a freedom fund, not just an emergency fund. It allowed me to pursue opportunities, take small risks, and live life without constant money stress. I could invest, travel, or switch jobs without the panic that money might run out.

I also learned the emotional value of a fund I could never have anticipated. Knowing I could handle unexpected events freed me from anxiety, allowed better decision-making, and improved relationships because I wasn’t constantly stressed about money.

For anyone starting, I recommend a phased approach. First, save a small starter fund, maybe $500 or $1,000. Next, aim for three months of expenses. Finally, target six months or more if possible. Each stage provides tangible security and builds confidence.

I found that personal goals drive saving behavior. I saved not only for emergencies but also for career transitions, potential home repairs, and even family support. Linking the fund to meaningful goals made it easier to stay disciplined and consistent.

Apps and tools helped me track progress effortlessly. Whether using Mint, YNAB, or a simple spreadsheet, visualizing growth made saving satisfying. Automation, combined with visualization, created habits that didn’t require constant effort but delivered consistent results.

Mistakes happened along the way, but the key was not to give up. Occasionally, an unexpected expense temporarily reduced my balance. Instead of feeling defeated, I replenished it immediately. Each setback was an opportunity to reinforce discipline.

I also began planning contingencies. Beyond the basic fund, I learned about insurance, warranties, and community resources that could supplement my emergency planning. Combining these strategies enhanced security without needing excessive cash on hand.

Sharing my story helped others. Friends and family started their own emergency funds, and discussing progress created accountability. If you’ve ever felt embarrassed about your finances, clap for yourself — you’re taking control by learning.

Over time, the fund became a foundation for all other financial strategies. With emergencies covered, I invested more confidently, budgeted more effectively, and even started a side hustle, knowing that unexpected expenses wouldn’t derail progress.

I realized that emergency funds are not optional, they’re essential. They aren’t about wealth, status, or perfection. They’re about security, control, and peace of mind. Even a modest fund offers disproportionate benefits in mental and emotional stability.

Starting today is better than waiting. You don’t need a massive contribution to begin. Even $10 or $20 a week, automated and consistent, sets the foundation for long-term resilience. Consistency compounds, just like your investments.

I built a system that works for me: track spending, automate savings, personalize my fund, visualize growth, celebrate milestones, and educate myself continuously. Each step reinforced the habit and increased my confidence.

Reflecting, I see that my emergency fund changed more than my finances. It changed my mindset, reduced stress, and gave me freedom to pursue opportunities. What started as $25 per week became a lifeline of confidence, security, and control.

If you’ve read this far, consider giving this article a clap 👐. Every small gesture supports writers, helps others discover practical strategies, and reinforces the importance of financial empowerment. Even one insight can transform your relationship with money.

Start small, stay consistent, automate your savings, and personalize your fund. Celebrate every milestone, even tiny ones, and build the mental habit alongside the financial one. Over time, an emergency fund stops being just “money in an account” — it becomes freedom, confidence, and peace of mind.

Why You Need an Emergency Fund — Now was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.