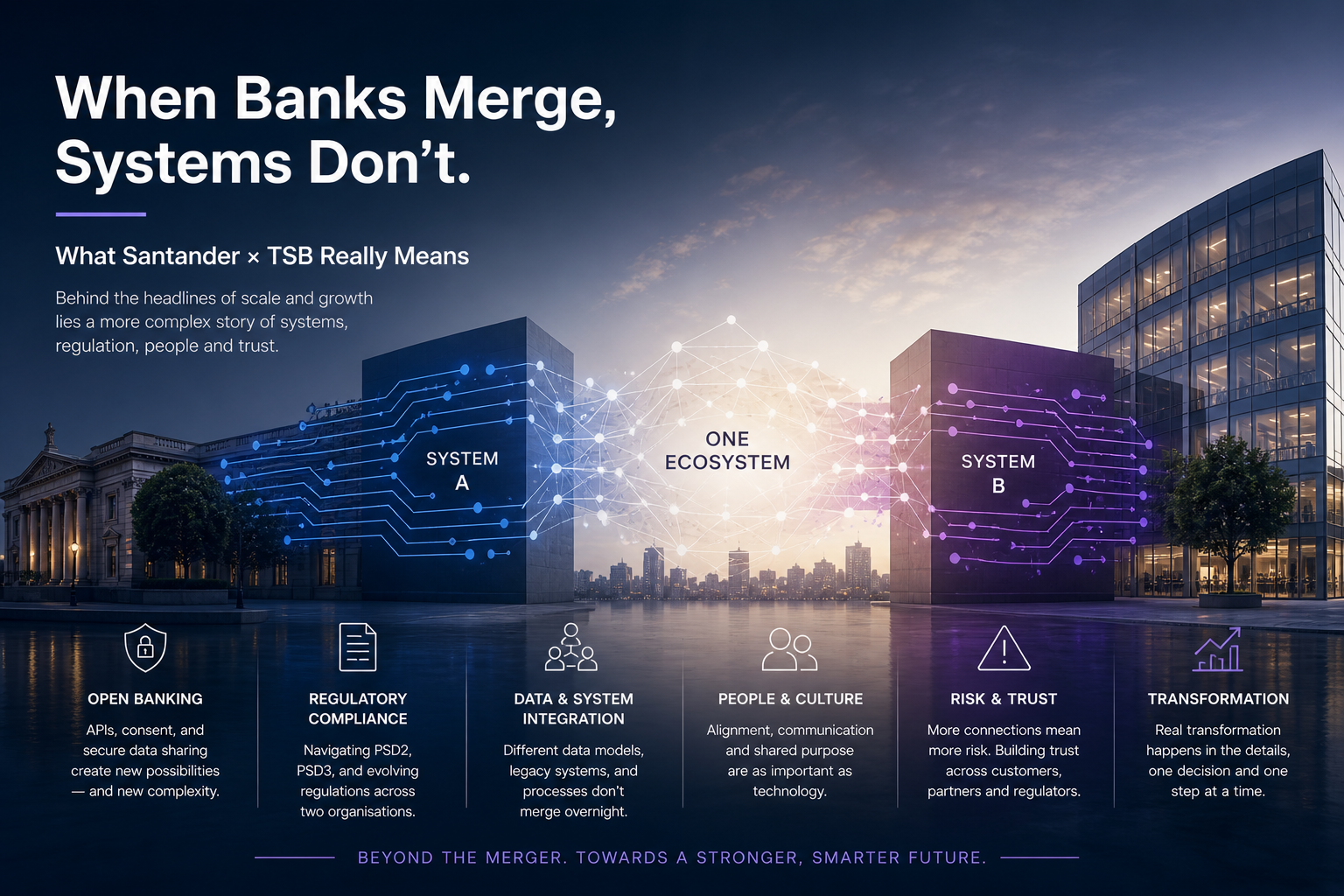

When Banks Merge, Systems Don’t. What Santander × TSB Really Means

Jennifer D3 min read·Just now

Jennifer D3 min read·Just now--

When news broke that Santander UK completed its acquisition of TSB Bank, most headlines focused on scale.

Bigger customer base.

Stronger market position.

One of the largest banks in the UK by current account balances.

But that’s not the part I keep thinking about.

Because acquisitions in banking are never just about size

On paper, it’s straightforward:

One bank acquires another.

In reality, it’s two completely different systems, cultures, and regulatory interpretations being asked to become one.

Especially in a world moving toward open banking

Today, banks aren’t just managing internal systems anymore.

They’re part of a much larger ecosystem:

- Third-party providers accessing data via APIs

- Consent-driven data sharing frameworks

- Regulations like PSD2 (and soon PSD3) shaping how data flows

- Increasing expectations around transparency, security, and control

So when an acquisition like this happens, the challenge isn’t just integration.

It’s integration in an already open, interconnected system.

What that actually looks like inside

Imagine trying to align:

- Two different KYC and AML frameworks

- Two sets of customer data structures

- Two interpretations of the same regulation

- Two technology stacks built over years (sometimes decades)

And now layer on:

- Open banking APIs

- Third-party integrations

- Ongoing regulatory updates

There’s no “clean merge.”

Only careful, continuous alignment.

This is where strategies like “ONE Transformation” come in

At Banco Santander, initiatives like ONE Transformation are about standardising systems across geographies.

From the outside, it sounds efficient.

And it is.

But from the inside, it’s a constant balancing act:

- Standardising without oversimplifying

- Scaling without increasing risk

- Moving fast without misinterpreting regulation

The part we don’t talk about enough

Open banking is often framed as innovation.

And acquisitions are framed as growth.

But the intersection of the two is where things get complex.

Because now banks are dealing with:

- More data flowing across systems

- More dependencies on external providers

- More regulatory scrutiny

- More pressure to get things right, the first time

A more human perspective

Behind this acquisition, there are teams asking questions like:

- How do we merge customer journeys without breaking compliance?

- Which system becomes the source of truth?

- Are we interpreting regulations consistently across both entities?

- What happens to existing integrations and third-party access?

These aren’t just technical problems.

They’re coordination problems.

And they’re deeply human.

What we’ve been seeing while building Comply2Reg

While working on Comply2Reg, we’ve spent a lot of time looking at how financial institutions deal with regulatory interpretation in real workflows.

And one thing stands out:

The challenge isn’t just understanding regulation.

It’s aligning how different teams interpret and apply it, Especially during change.

Acquisitions like this amplify that challenge.

Because now it’s not just teams within one bank.

It’s two organisations trying to operate as one.

Where this goes next

If open banking is about making financial data more accessible…

Then integrations like Santander × TSB are about making financial systems more unified.

But getting there isn’t instant.

It’s iterative.

It’s complex.

And it requires constant alignment between technology, regulation, and people.

Final thought

From the outside, this looks like growth.

From the inside, it’s transformation.

And somewhere in between, there’s a lot of invisible work happening to make it all function as one system.

That’s the part I find most interesting.