Thesis & Key Findings

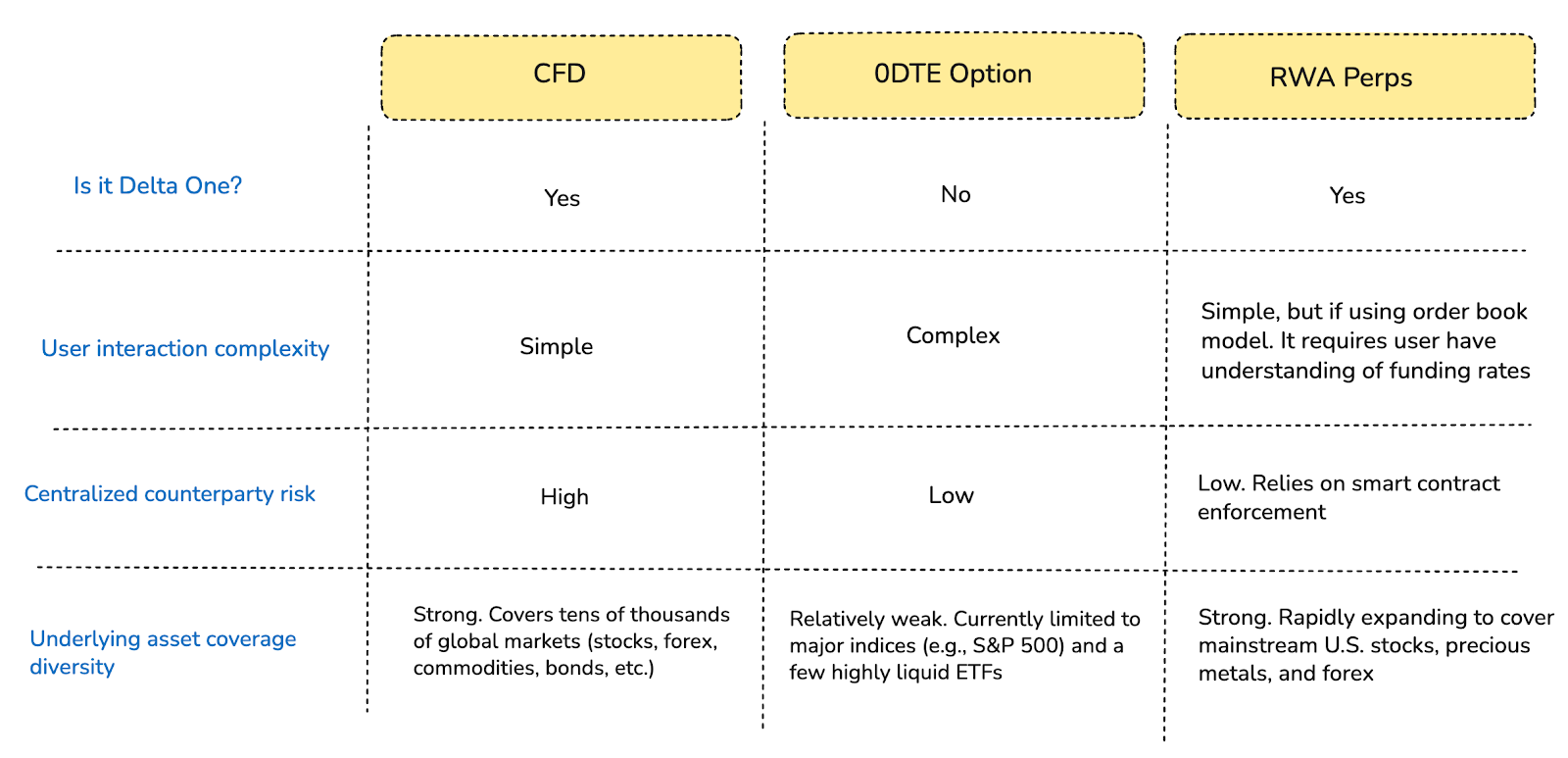

- A Structural Upgrade for Delta One Demand. Retail traders currently rely on inefficient vehicles for directional leverage. U.S. 0DTE options impose unwanted theta decay on pure directional bets, while the $30 trillion offshore CFD market introduces opaque broker mechanics and counterparty risk. RWA perpetuals strip out time decay and centralized risk, offering a transparent, mathematically linear onchain alternative for this proven demand.

- Architectural Trade Offs in Asynchronous Markets. Bridging 24/7 crypto rails with traditional market hours forces protocols to compromise between high leverage, continuous trading, and risk externalization. Two distinct models have emerged to manage market closures: Ostium’s active-hedged pool prioritizes solvency by halting trading during offline hours to eliminate gap risk, while Trade.xyz (Hyperliquid) preserves 24/7 execution by pricing weekend volatility into dynamic funding rates and maker spreads.

- Offshore Distribution Strategy. Dual SEC/CFTC jurisdiction makes compliant U.S. retail equity perpetuals highly impractical. As a result, the primary growth vector will lie offshore via Regulation S exemptions. Instead of acquiring retail users directly, RWA perp DEXs can scale as backend clearing engines for regional offshore brokers—outsourcing KYC and client distribution to TradFi entities while managing margin and atomic settlement onchain.

- Adapting to 24/7 TradFi Infrastructure. Legacy institutions like the NYSE are moving toward continuous U.S. equity trading, which will soon erode DeFi’s monopoly on 24/7 access. While this eliminates the weekend gap risk for onchain protocols, it forces a shift in competitive strategy. Long-term, RWA perps will differentiate strictly on permissionless access, capital efficiency, and higher leverage, serving as a high-velocity execution layer atop regulated TradFi spot markets.

Introduction: The Underserved Demand for Leveraged RWA Exposure

The prevailing approach to RWA has centered on tokenization, the mapping of real-world asset ownership onchain to improve settlement efficiency. While improving settlement is a valid goal, this focus overlooks the primary engine of global finance: leveraged directional trading and risk management.

Indeed, the fundamental driver of global liquidity is the demand for leveraged directional exposure. The scale of this demand is already proven. The U.S. options market generates monthly notional values as high as $89 trillion, while offshore CFD markets exceed $10 trillion in monthly volume. This confirms a persistent retail appetite for high leverage, short horizon risk. Yet, the primary instruments serving this demand are structurally inefficient. For the large segment of traders using them for simple directional bets, 0DTE options impose the cost of theta decay and non-linear vega exposure. At the same time, CFDs are hampered by opaque mechanics and centralized counterparty risk.

These traders are fundamentally seeking a clean Delta One payoff. Their objective is a linear and symmetric translation of price movement into P&L, free from the embedded value leakage of time decay or unintended volatility exposures. (Arthur Hayes’ Adapt or Die provides a helpful historical recap of why perpetuals emerged in crypto to solve this exact problem).

DeFi teams are now engineering solutions for this structural mismatch. RWA perps (RWA perpetuals) apply crypto’s most battle tested derivatives primitive to traditional underlyings. Operating as synthetic instruments, these protocols rely on oracle price feeds to establish and maintain exposure to traditional underlyings, eliminating the need for physical custody or delivery. This core synthetic design inherently enables 24/7 leveraged trading on equities, commodities, and FX with crypto native settlement.

This architecture delivers a step function improvement. RWA perps are a structural solution to the core physical constraints of traditional derivatives: T+2 settlement delays, fragmented trading hours, and high access barriers. This model achieves far more than simply replicating Nasdaq or CME prices. It fundamentally reconfigures pricing authority, liquidity distribution and risk transfer. As the inefficiencies in traditional instruments become more apparent, RWA perps with their linear payoffs and atomic settlement are positioned to become the optimal container for global spillover leverage demand. They may be the final piece required to move global derivatives infrastructure onchain.

1. Market Background and Key Entry Points

1.1 Analyzing the U.S. 0DTE Options Market

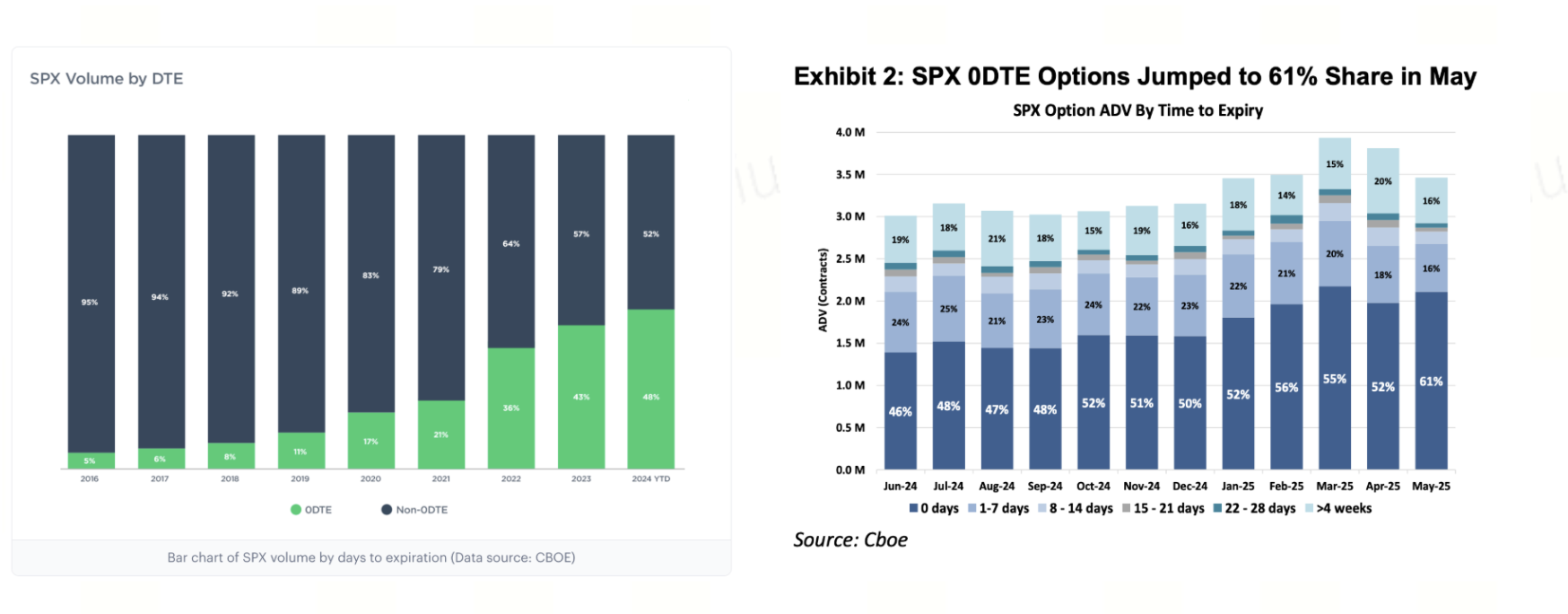

The U.S. options market has seen a significant structural transformation over the past decade. Data from Cboe Global Markets reveals a dramatic surge in 0DTE (Zero Days to Expiration) volume for S&P 500 index options, climbing from under 5% in 2016 to exceeding 60% today. This shift accounts for approximately $48 trillion in monthly notional value, underscoring a massive capital pool actively seeking extreme intraday leverage.

Figure 1: The two charts above show the proportion of S&P 500 index options with different expiration times from 2016 to 2025. We can see that 0DTE options accounted for only about 5% of the options market in 2016, but by 2025, their market share has surged to 61%. This indicates that nearly half of all S&P 500 index options trading now consists of ultra-short-term bets on the same day direction.

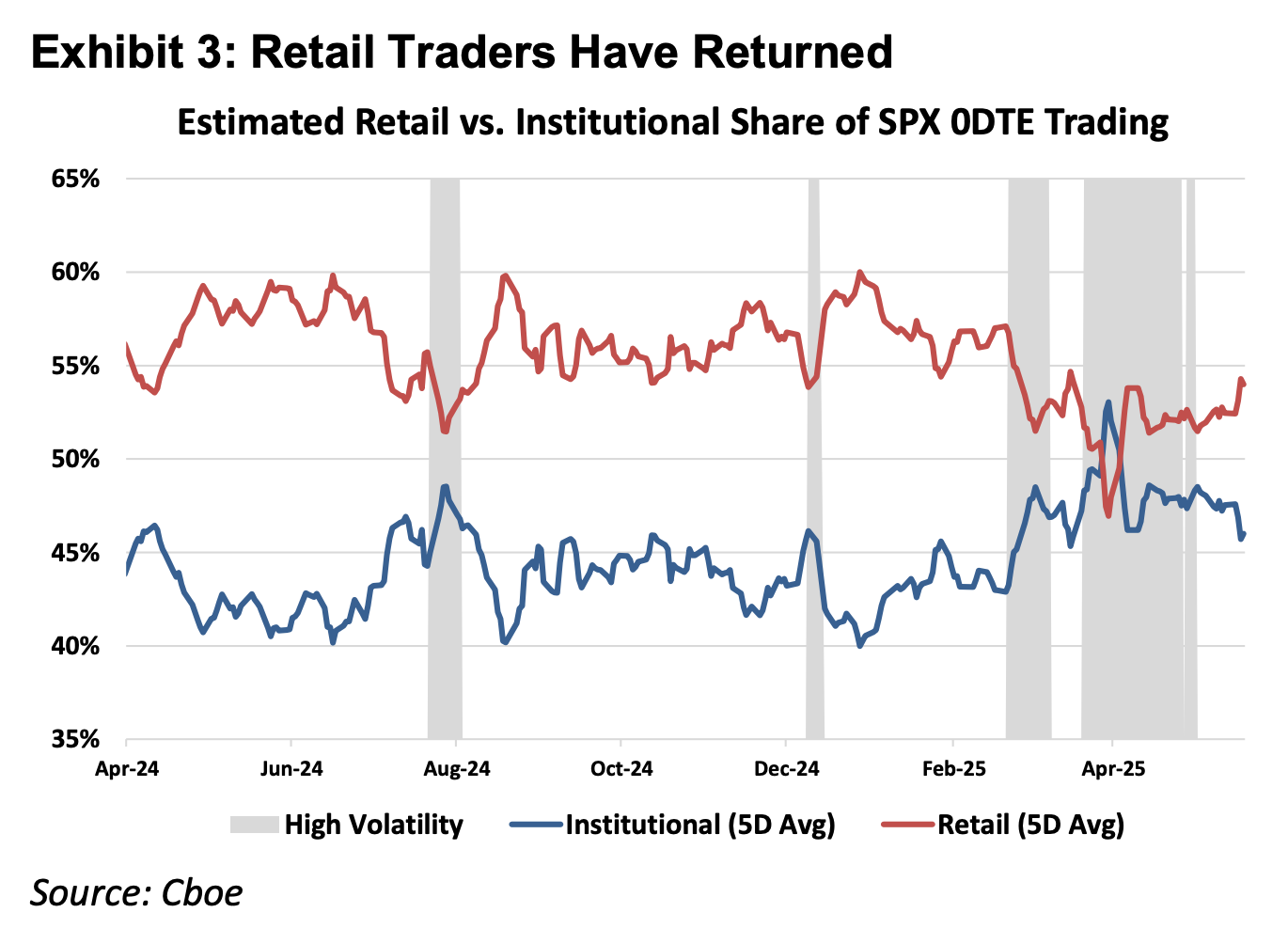

Figure 2: The chart above shows that retail investors are the absolute dominant force in the 0DTE market.

Understanding derivative instruments requires distinguishing between Delta One products and non linear instruments. Traditional assets like stocks and futures are Delta One, offering symmetric and linear profit and loss. Options, by design, manage asymmetric risk. For instance, a fund manager might purchase put options to hedge a large AAPL position against short term downsides, securing downside protection while retaining upside potential. This separation of rights and obligations, fundamental to options design, is key to managing asymmetric risk.

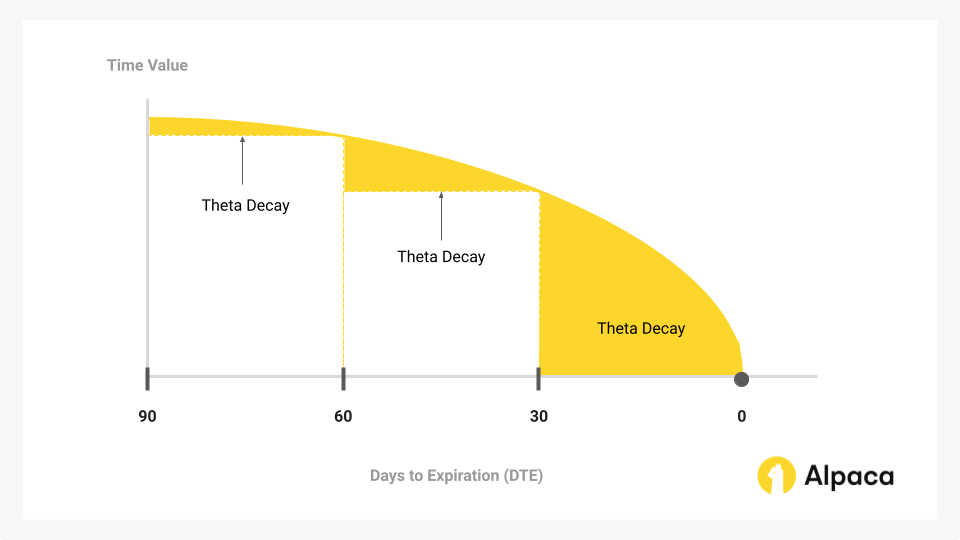

To achieve this risk hedging profile, option pricing inherently includes delta (directional exposure), convexity (gamma), and time value (theta). However, the rapid growth of 0DTEs highlights a paradox: many traders are not engaging in hedging or volatility strategies. Instead, they are leveraging options as the most accessible route for intraday directional leverage. This means they incur the cost of theta decay, an “insurance feature” they do not need. If the underlying asset’s price movement doesn’t sufficiently outpace this time decay, the trade can result in a loss, even if the directional bet was correct.

Figure 3: Time value is the main part of an option that decays over time and serves as the core battleground for 0DTE traders. Think of it as a “melting ice block”: the Y-axis shows the block’s size (the premium you paid), and the X-axis tracks time. The curve is relatively flat early on but becomes extremely steep near expiration (approaching 0 days), meaning time value evaporates very rapidly in the final hours. To profit, traders must count on the underlying price moving enough to outrun this accelerated decay.

In contrast, perpetual futures are pure Delta One instruments. By stripping away time decay and volatility costs, they offer clean, linear leveraged exposure, mathematically aligning more directly with this speculative demand than the mechanics of 0DTE options. Mathematically, this structure more directly aligns with this segment of speculative demand than the mechanics of 0DTE options.

1.2 Examining Offshore CFD Markets

Internationally, retail leverage demand is predominantly met by CFDs (contracts for difference). By 2025, this market was generating approximately $30 trillion in average monthly volume.

While CFDs offer a Delta One payoff, the market is largely broker-driven and suffers from significant transparency issues. The prevalent B-book model, where brokers internalize client flow and act as the direct counterparty, creates inherent conflicts of interest. Regulators like the UK’s Financial Conduct Authority (FCA) and European authorities ESMA have repeatedly voiced concerns over these embedded conflicts of interest and the pervasive lack of transparency in CFD markets, noting their vulnerability to misuse for insider dealing due to their speculative and highly leveraged nature.

RWA perps offer a DeFi native alternative. They function as contract enforced and transparent version of CFDs. By placing liquidation logic, funding calculations, and oracle pricing onchain, DeFi protocols eliminate the broker’s ability to interfere with trade outcomes. Furthermore, atomic stablecoin settlement dramatically improves capital velocity, enabling true self custody and nearly real time clearing.

2. Product Development Challenges

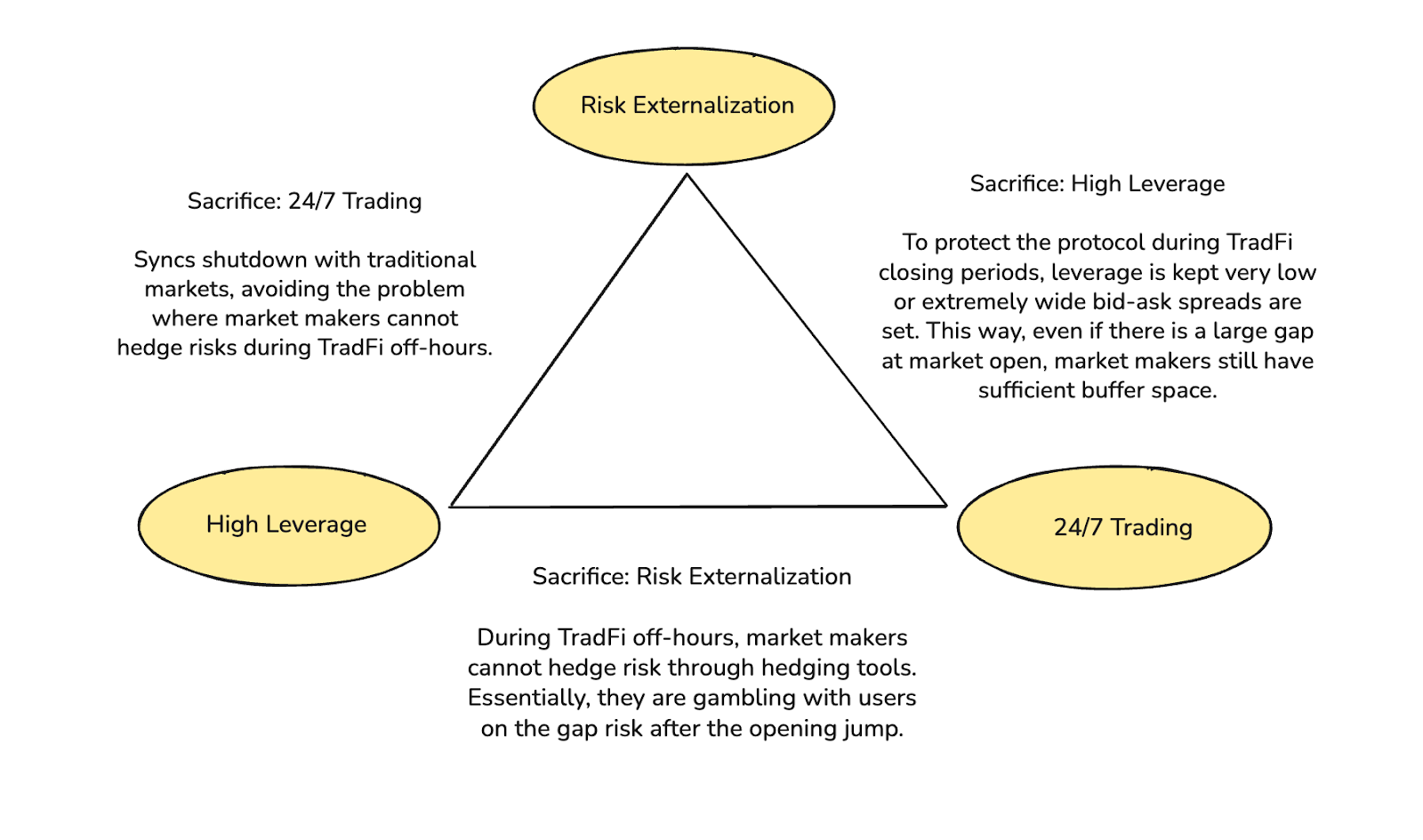

RWA perps are not a simple replication of crypto perps. While crypto assets trade 24/7 and settle T+0 onchain, traditional assets are bound by legal frameworks, market holidays, and slow banking settlement. This fundamental asynchrony creates a trilemma in RWA perp design:

- High Leverage: Meeting retail demand for amplified returns.

- 24/7 Availability: Preserving DeFi’s core value proposition.

- Risk Externalization: Preventing the protocol from absorbing directional risk.

Most designs can achieve two of these three critical objectives. Pursuing all three introduces significant risk, particularly during market closures and opening price gaps.

2.1 The Challenge of Onchain Price Anchoring During Market Closures

Perps function as a real time reflection of price discovery, requiring continuous spot price inputs. When Nasdaq or CME markets close, oracle data feeds become discontinuous, creating two core risks for onchain perpetuals:

- Risk 1: Market Maker Hedge Disruption. Professional market makers maintain delta neutral positions by hedging their onchain exposure in real time. If a maker sells $1 million of TSLA exposure onchain, they must immediately hedge by buying a comparable amount in the spot or futures market. When TradFi venues close, this essential hedge channel is unavailable. To avoid unhedged exposure, makers are forced to either withdraw liquidity or significantly widen their quoted spreads. This directly leads to the observed non linear expansion of CLOB spreads on weekends.

- Risk 2: The Impact of Monday Opening Gaps. Unlike the continuous price action in crypto markets, RWA price discovery accumulates pressure during closures and is released at the open via events like earnings reports or macro data. For a user trading at 100x leverage, where their margin buffer is often around 1%, a mere 2% opening gap can bypass liquidation engines. This price discontinuity prevents timely counterparty execution before insolvency, potentially leading to systemic bad debt for the protocol.

Two primary solutions have emerged to mitigate these risks. One approach is internal simulated pricing, employed by platforms like Trade.xyz. This method uses EMA style smoothing and internal order flow to allow prices to “drift” during oracle downtime, preserving a 24/7 trading surface. However, this creates a shadow market susceptible to gaming. The alternative is a forced risk downgrade, exemplified by platforms like Ostium. This pragmatic strategy imposes a 0DTE-like constraint: high leverage positions must be closed or delevered before the market closes. Only positions with substantial margin buffers, sufficient to absorb potential 5–10% gaps, are permitted to carry overnight. This approach sacrifices some “perpetualness” in favor of solvency.

2.2 Delivering TradFi Grade Market Depth Efficiently

Liquidity design and execution mechanisms are critical for capital efficiency, risk allocation and user experience. The two dominant architectural approaches are CLOBs and oracle based pools. Hyperliquid’s success with the order book model in crypto stems from near-zero-friction hedging: market makers can instantly hedge onchain fills on 24/7 CEXs. For RWAs, however, this hedge loop becomes high friction. Onchain settlement is T+0 via USDC, but hedging equities requires fiat settlement. Converting onchain P&L to fiat and transferring it to a broker involves delays, forcing makers to maintain large, idle USD balances. This reduces capital efficiency and increases opportunity cost. Moreover, banking systems close on weekends and holidays, hindering hedge adjustments during critical market events. This friction is a primary driver behind the ongoing debate about the optimal architecture for RWA perps.

2.3 Ensuring Solvency Amidst Sustained One Way Markets

The third challenge is ensuring long term solvency through effective hedging. GMX’s pool model functions effectively in crypto’s volatile, mean reverting environment by capturing revenue from time decay and liquidations. However, RWA risk distributions differ significantly. Major equity indices can exhibit multi year trends. Without robust risk externalization, sustained trader profits in these trending markets directly translate into LP pool losses, potentially draining capital and breaking protocol solvency. Even with external hedging, the aforementioned T+1/T+2 settlement mismatch between onchain and TradFi venues makes rapid, cost effective hedging difficult. Two distinct strategies have emerged: Ostium’s active hedging model, which offloads risk to professional capital via an OMM, and CLOBs’ risk premium model, where wider spreads compensate makers for hedging friction and settlement mismatches.

3. Navigating RWA Perp Architectures

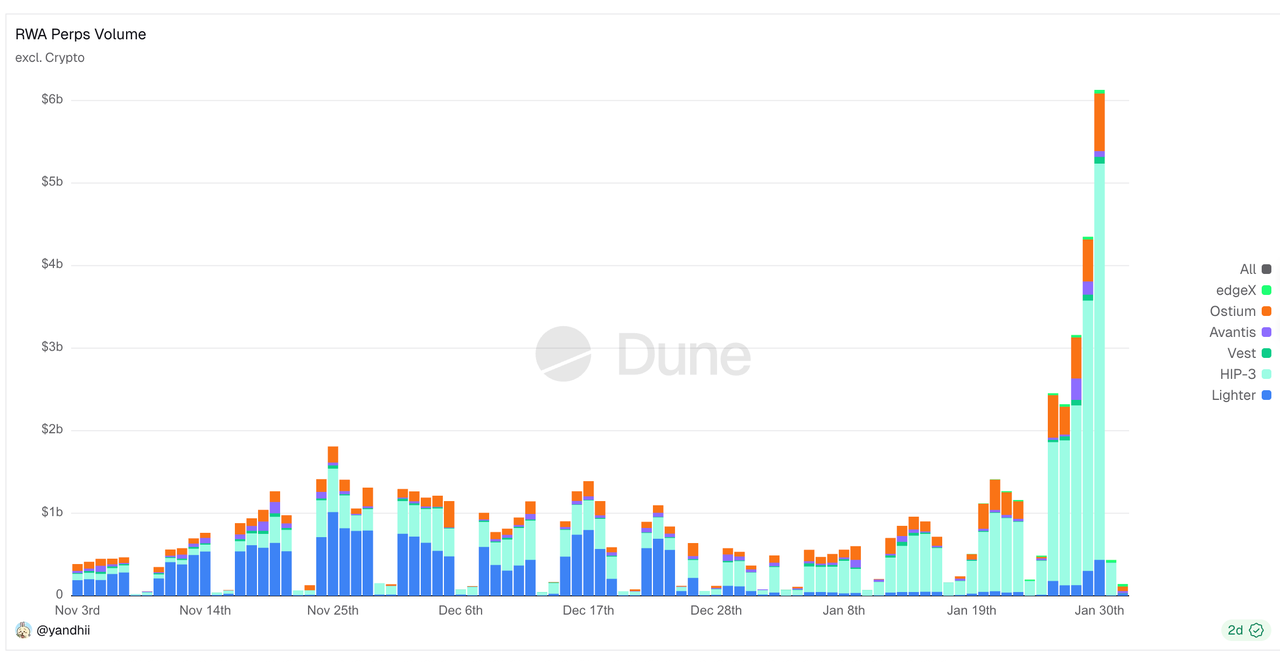

The core challenge in RWA perps stems from the asynchronous nature of traditional asset markets. Despite generating over $20 billion in volume over a recent 30-day window, weekend volume on RWA perp DEXs typically collapses by 70–90%. This reality underscores that DeFi liquidity remains highly anchored to TradFi trading hours. To navigate this fundamental constraint, two architectural paradigms have emerged: Ostium’s active hedge pool model and the internal pricing order book model, exemplified by protocols like Trade.xyz within the Hyperliquid ecosystem.

Figure 4: It is evident that trading volume experiences a sharp contraction on weekends.

3.1 Early RWA Perp Experiments: Synthetix and Gains Network

Before the current generation of protocols, the initial wave of synthetic asset experiments validated onchain demand for traditional asset exposure. These early efforts also exposed the limitations of first generation mechanisms in capital efficiency and risk management.

- Synthetix: Global Debt Pool Model. Synthetix was an early experimenter in bringing RWA prices onchain, operating as a decentralized synthetic asset platform. Its core thesis was an “infinite liquidity” exchange without an order book, where synths could be exchanged at oracle prices. The counterparty was the collective SNX staker base, absorbing system wide P&L pro rata. This model addressed liquidity cold starts especially during liquidity mining incentives. Synthetix listed mirrored equities like sAAPL and sTSLA between 2020 and 2021. However, it later delisted most RWA assets primarily due to its lack of an active hedging layer at the protocol level. Oracle failures also led to incidents such as a misreported KRW exchange rate in 2019 that resulted in a significant arbitrage exploit. In general, Synthetix pioneered the oracle priced pool model in RWA perps but largely exited the this market around 2022.

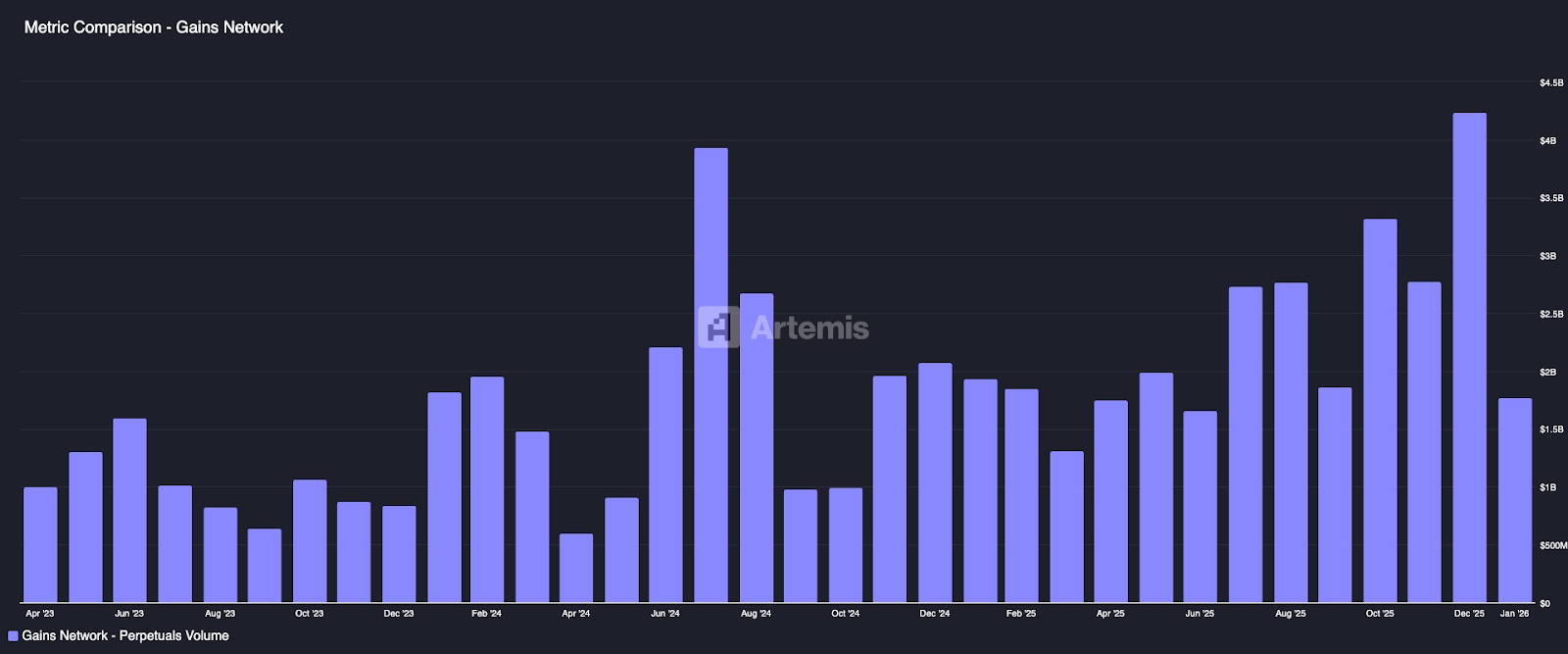

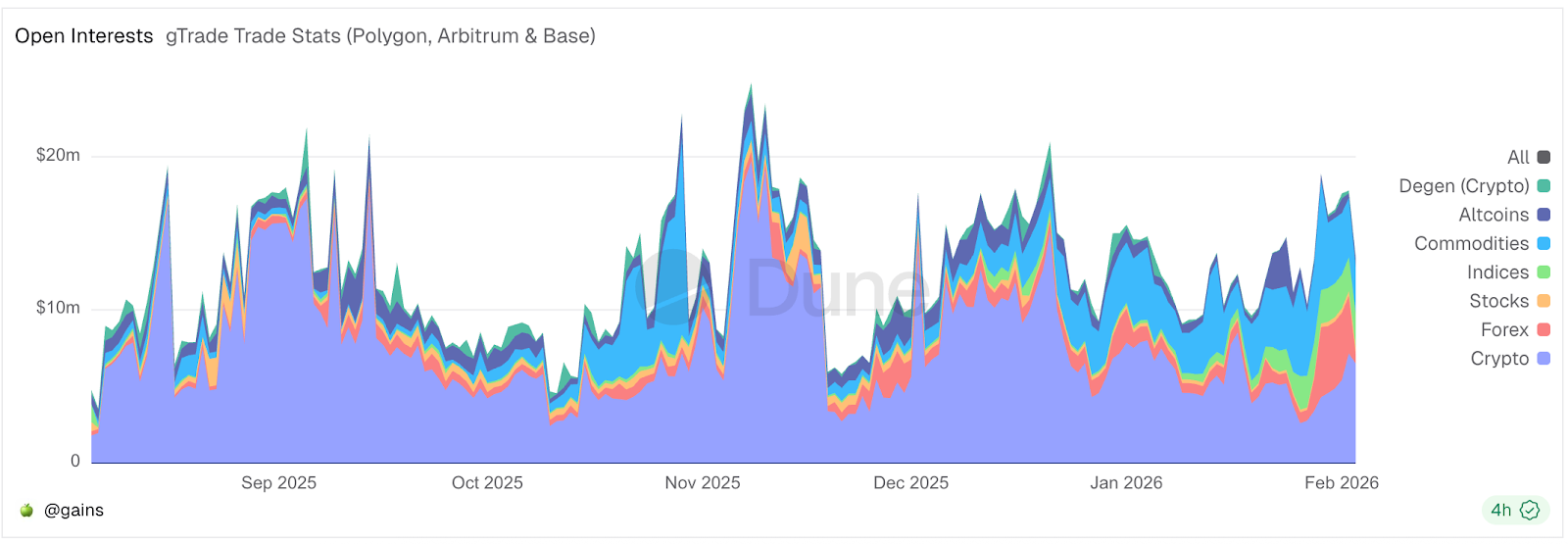

- Gains Network (gTrade): Oracle Priced Vault Model. Gains supports crypto, FX, and U.S. equities, operating across Polygon, Arbitrum, and Base. Unlike Synthetix, Gains utilizes an independent stablecoin vault as the counterparty. The GNS token acts as a risk buffer and the protocol mints GNS to recapitalize the vault during deficits and burns GNS with surplus profits. LP yield comes from fee sharing, but their P&L is inversely correlated with trader P&L. Gains employs a price impact fee model to simulate order book slippage and enforces automated safety mechanisms like profit caps. Its success validated the oracle based pool model at scale but highlighted the inherent challenge of pools bearing concentrated profitability risk without robust external hedging.

Data source: https://dune.com/gains/gtrade_stats

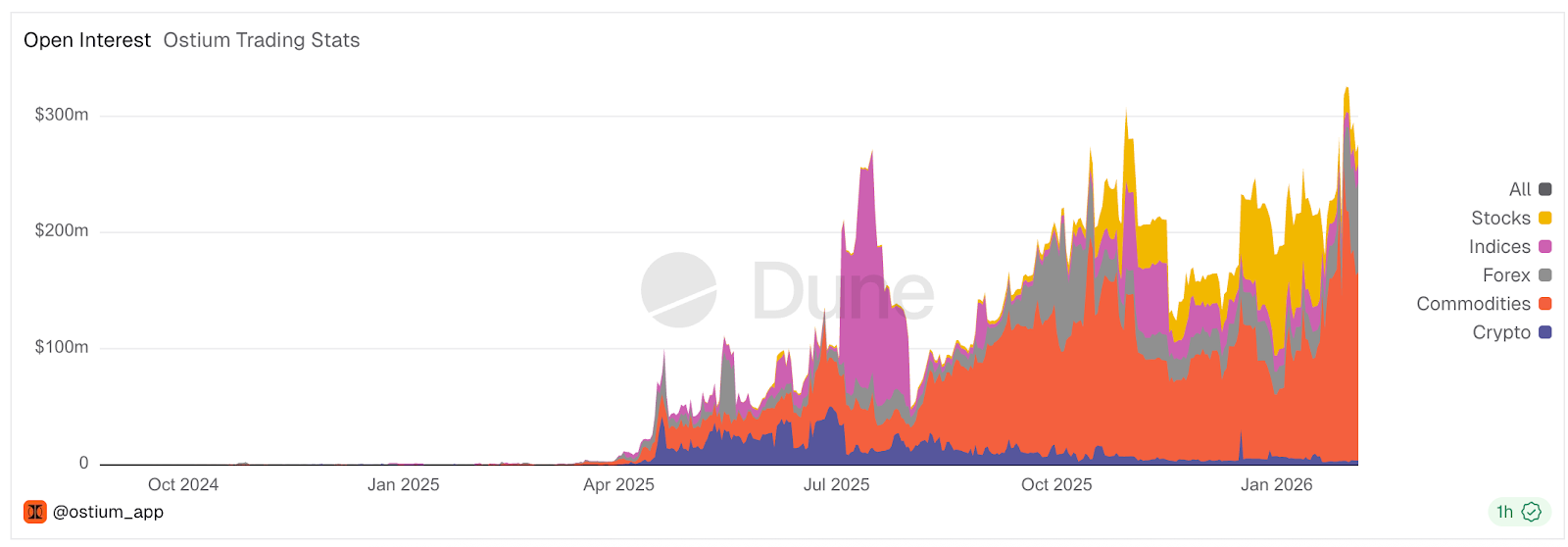

3.2 Ostium: Building an Onchain CFD Broker

Ostium was launched on Arbitrum mainnet in August 2025, builds upon the pool-based model but fundamentally rethinks its limitations. Recognizing that the “trader profit equals LP loss” dynamic is structurally unfavorable and caps market growth, Ostium integrates concepts from traditional brokers’ A-book (external hedging) and B-book (internal matching) directly onchain.

Data source: Defi Llama, https://dune.com/ostium_app/stats

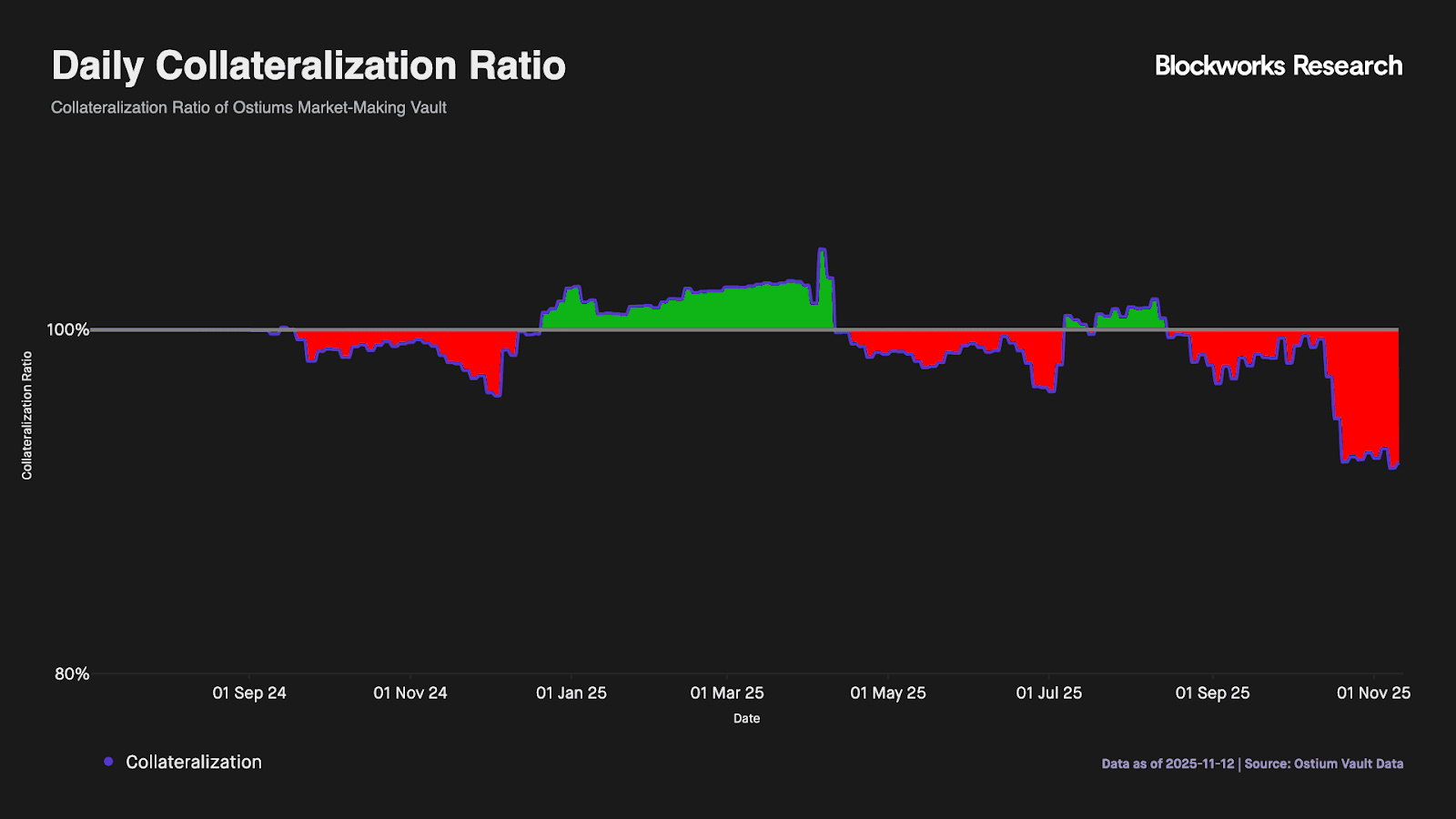

- Liquidity Model and Incentive Mechanics. Ostium employs a two-layer pool architecture. The first layer, the “Liquidity Buffer,” consists of protocol owned capital that absorbs initial P&L variance. The second layer, the “OLP Vault,” is LP provided capital that acts as a counterparty only when the Liquidity Buffer is depleted. The core innovation is the separation of “settlement” from “market making.” Ostium understands that simple two-layer buffers cannot handle long run directional imbalances. Its design separates these functions, preventing the passive LP pool from being the long term risk warehouse. While the OMM (market-making and hedging) vault is not yet alive, we think its ability to operate successfully at scale hinges on professional grade execution for low latency hedging, robust collateral routing across fiat and stablecoins, and dynamic delta monitoring. Crucially, the OMM operator will need a legal TradFi entity and institutional accounts to interface with venues like CME.

Data source: Blockworks (According to Blockworks’ research, Ostium v1 product without the MM vault design alive yet also met the similar directional risk problem that all other pool model projects have)

- Risk Controls during Market Closures. Ostium aligns tightly with U.S. equity trading hours, ensuring market orders execute only when the underlying market is open, avoiding pricing vacuums. To mitigate gap risk, the platform enforces strict liquidation checkpoints. In the final 15 minutes before market closes, positions exceeding a leverage threshold (e.g., 10x) are forced to close. This process removes overnight leverage, protecting traders from insolvency and eliminating LP exposure during non-trading hours. Ostium also introduced 0DTE Perps, a hybrid product combining 0DTE style leverage with linear perp payoffs and automatic rolling, simplifying user workflow and improving capital utilization.

- Ostium’s Thesis: Why Pools Over Order Books for RWAs. Founder Kaledora argues that replicating on chain order books for RWAs is capital inefficient because global price discovery already thrives on venues like Nasdaq and CME. Rather than rebuilding this infrastructure, protocols can use pools combined with external hedging to transfer risk to deep global markets. Under this model, volume is limited by distribution in a manner comparable to CFD brokers instead of being restricted by the size of the on chain pool.

- Why haven’t established pool based projects like GMX adopted similar designs for directional risk? We think the reason might because the trade offs are too high. Its system already maintains balance through internal tools like adaptive funding fees and price impact. Adding external hedging would only sacrifice returns and introduce unnecessary complexity or centralization. Furthermore, the GMX pool serves as the aggregate counterparty for all traders. Highly volatile crypto markets statistically follow the Law of Large Numbers, where individual random bets trend toward negative expected value, enabling the pool to capture positive expected value as the universal counterparty. In contrast, Ostium focuses on RWA markets (such as stocks) where volatility is significantly lower.

Notably, the “Global Hedge Vault (GHV)” proposal appearing on the GMX governance forum in August 2025, which seeks to introduce external market making mechanisms to achieve delta neutrality indicates that even established pool-based projects are closely monitoring this new trend.

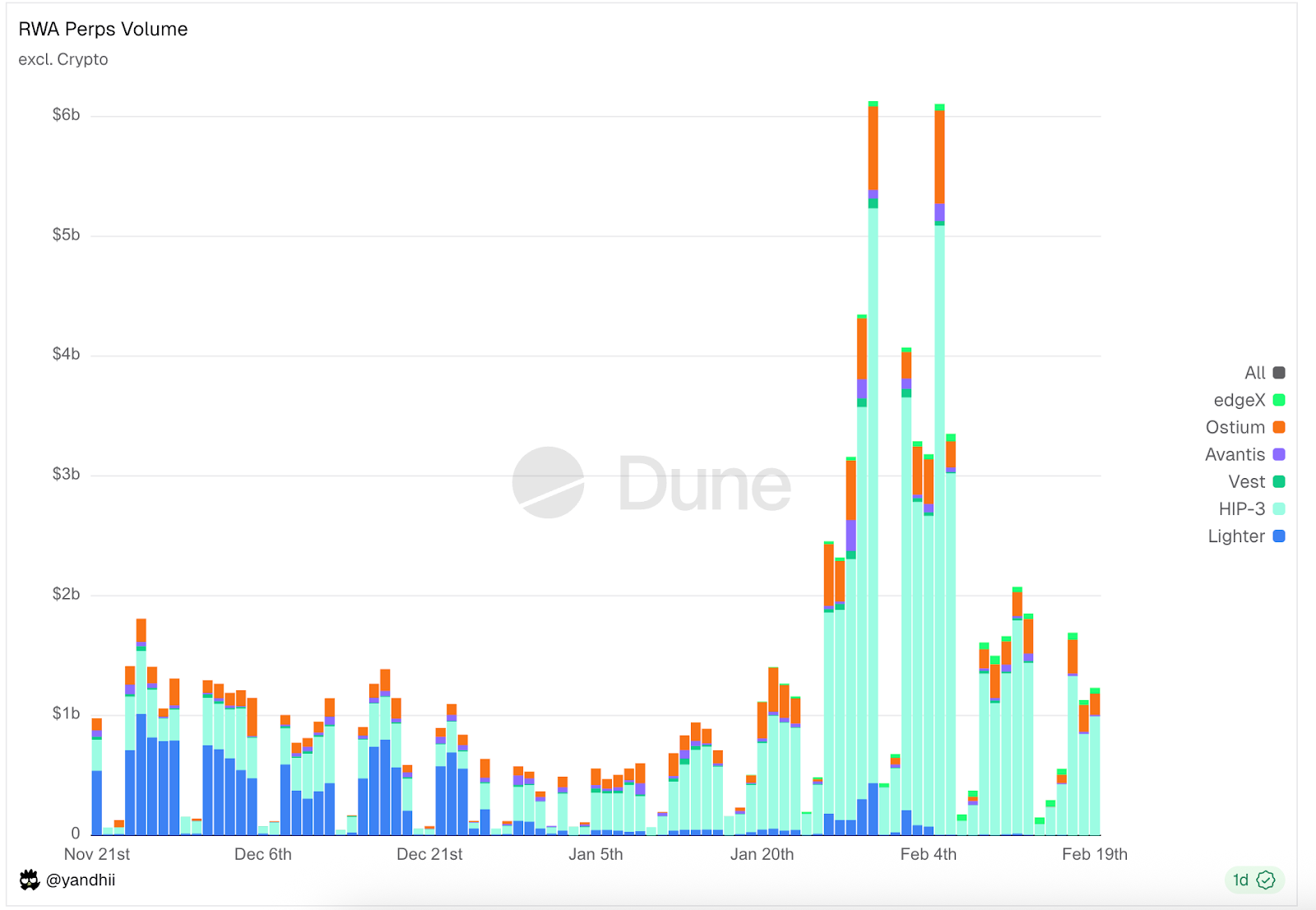

3.3 Order Book Model: HIP-3 Leads in the Early Competitive Landscape

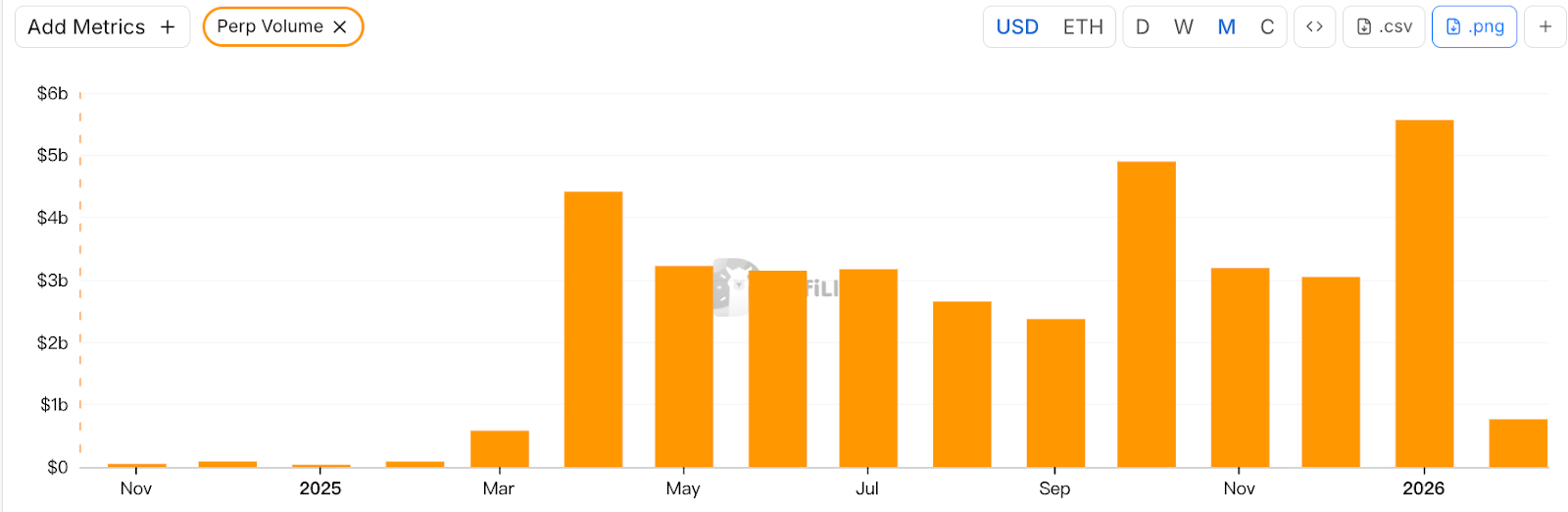

Data Source: https://dune.com/yandhii/rwa-perps

Within the order book sector, the Hyperliquid HIP-3 ecosystem accounts for the bulk of trading volume and open interest. Nevertheless, the sector remains structurally competitive, with protocols such as Lighter and Vest Markets emerging as key challengers in the RWA Perps CLOB segment.

Technically, The HIP-3 upgrade evolved the platform into a high-performance onchain execution and clearing engine, positioning “HyperCore” as its core matching and settlement infrastructure layer. Its vision is to split the roles of a Designated Contract Market (DCM) and Derivatives Clearing Organization (DCO) onchain. The Hyperliquid chain acts as the unified DCO, while third party “Deployers” take on the DCM role.

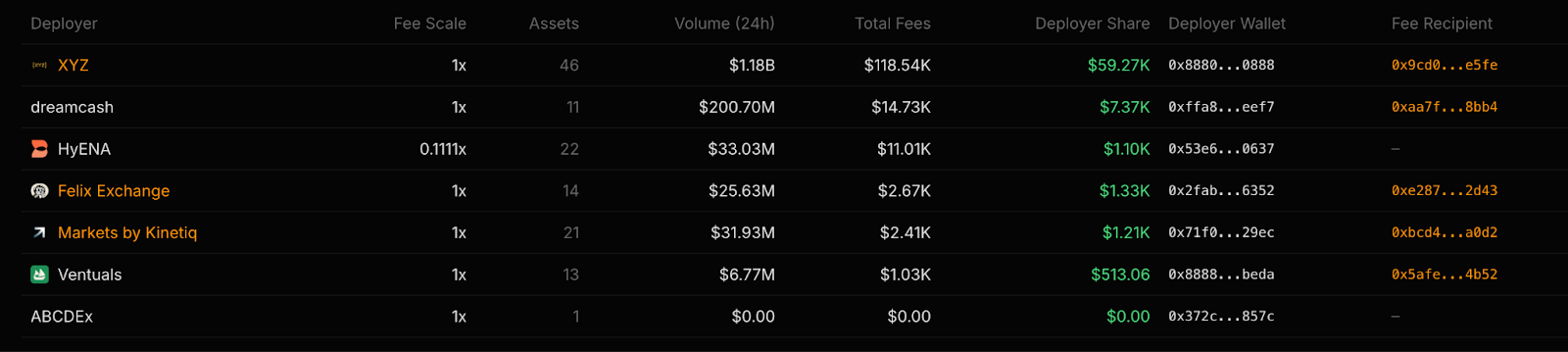

- Project Overviews: The HIP-3 ecosystem includes several RWA perp deployers, each differentiating through execution mechanisms, asset sets, and settlement currencies.

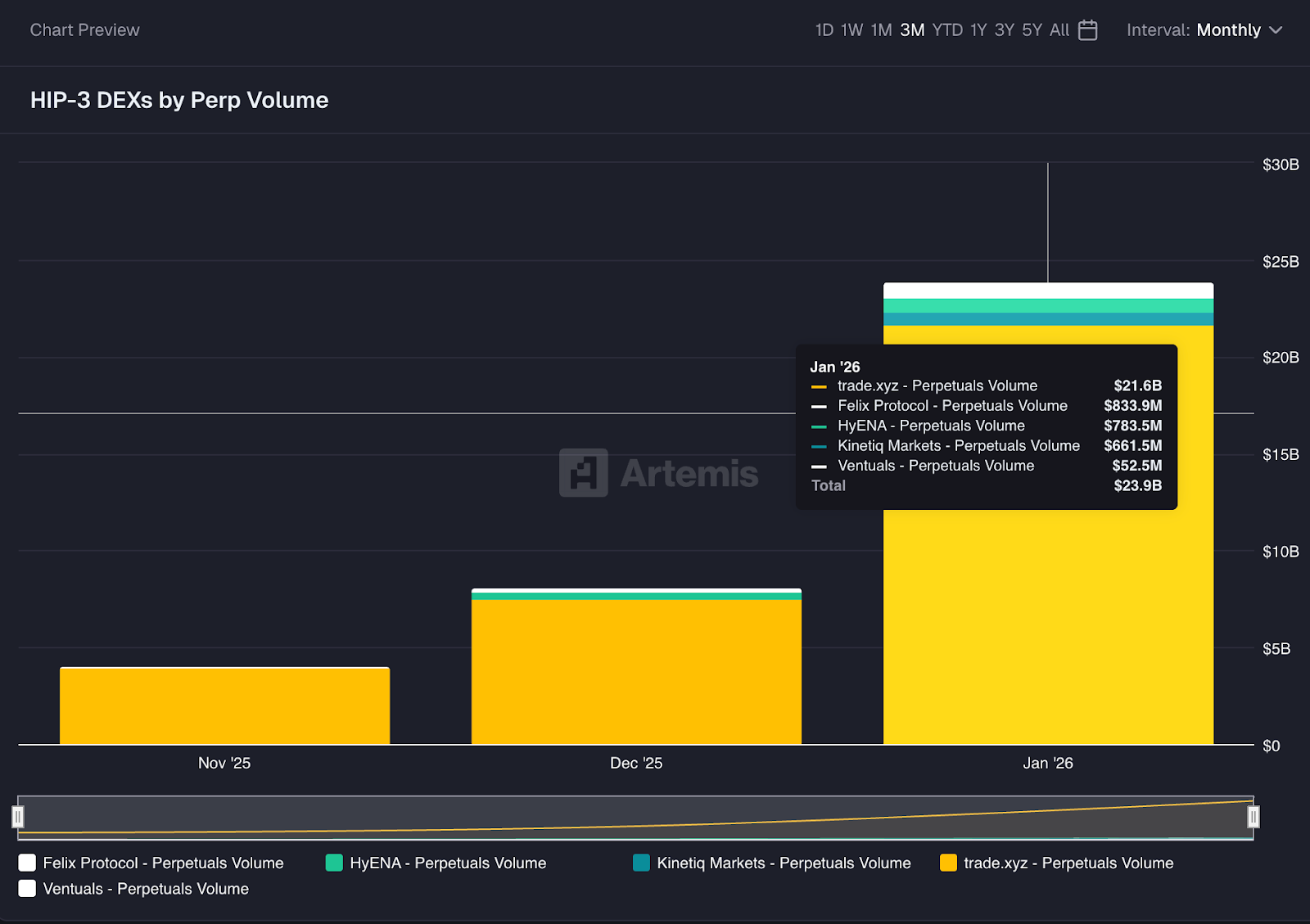

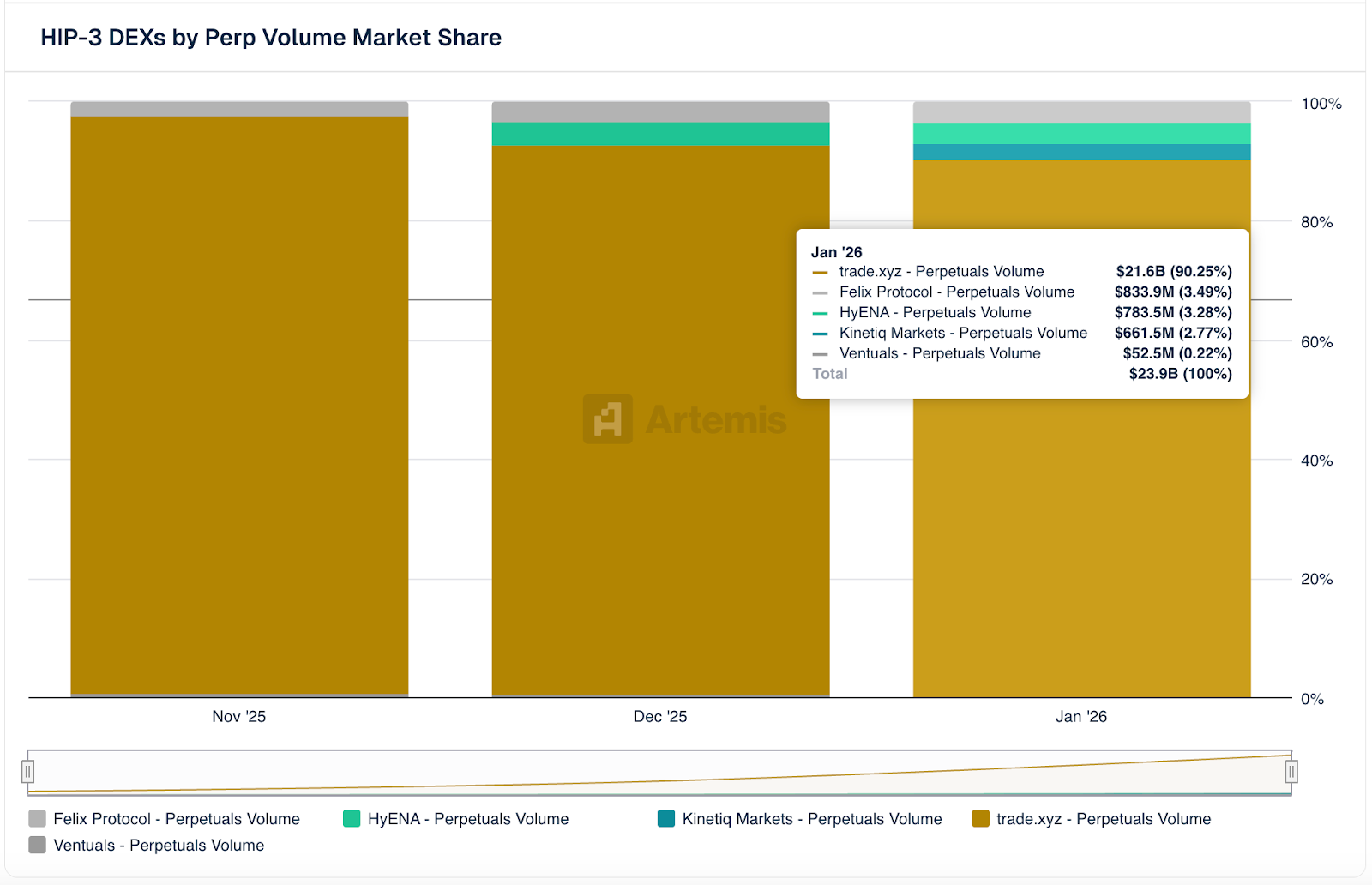

- Trade.xyz: A leading RWA perp DEX within the HIP-3 ecosystem developed by HyperUnit which is an asset layer team partnered with Hyperliquid. Trade.xyz emphasizes 24/7 trading for U.S. equities and other traditional assets. It initially launched the XYZ100 perpetual, which tracks the Nasdaq-100 index, alongside several U.S. tech leaders. By late January 2026, Trade’s monthly volume had grown to over $21 billion, up nearly 10x from around $2 billion in November 2025. Currently, Trade.xyz leads all HIP-3 perpetual venues by a significant margin, contributing around 90% of the total market volume.

Data Source: Artemis

- Markets.xyz: Launched by the Kinetiq team (a Hyperliquid liquid staking project) in mid January 2026, Markets focuses on global equity indices and macro assets. A key differentiator is its use of USDH as collateral, which reduces trading fees and increases rebates, allowing it to compete on cost (20% lower taker fees, 50% better maker rebates and 20% more volume contribution toward fee tiers)

- Felix: Originally a lending and stablecoin protocol on Hyperliquid, Felix issues the synthetic dollar feUSD via CDPs and operates a matched lending market. Following HIP-3’s launch, Felix expanded into perpetual markets as a Deployer, listing U.S. equities. Felix also uses USDH as its settlement collateral.

- Dreamcash: A project developed by Beam. Dreamcash is specifically focused on the mobile product positioning itself as a mobile trading terminal for RWA perps.

Data Source: Stonksonchain.net

- Core Pricing Mechanism: For 24/7 RWA perps built on an order book model, the primary technical challenge is maintaining fair and robust pricing when the underlying market is closed. Platforms like Trade.xyz employs a dual-track system where execution price is determined by order book dynamics. Oracles serve as referees for risk controls. Their data is primarily used for funding and liquidation checks. The mark price, critical for P&L and liquidation calculations, is computed as the median of three inputs: the oracle price (the macro anchor), a persistent deviation mean (oracle price plus an EMA basis over 150 seconds), and the immediate order book price (median of bid, ask, last trade). This median calculation aims to smooth noise and reduce manipulation risk.

- Oracle Source Switching. To enable 24/7 operation, oracle data sources dynamically switch based on U.S. equity trading regimes. This includes aggregated spot references during regular hours, ATS prints after hours, and an internal pricing mode on weekends utilizing EMA, discovery bounds and funding rates. For equity indices, Trade.xyz references index futures with longer trading hours rather than the spot index to support dynamic pricing. The operationalization of these varied pricing strategies across different timeframes is supported by active oracle usage from providers such as Pyth, Chainlink, Redstone, Seda, and Chaoslabs.

3.4 A Comparison of Pricing Mechanism and the roles of Oracle in two systems

The divergence between Ostium and Trade illustrates a fundamental design choice in RWA perp architecture: whether to internalize or externalize the cost of weekend risk. Ostium externalizes this cost by halting operations, thereby ensuring price integrity and protecting LPs from the unhedgeable risk of market gaps. Trade internalizes the cost through its dynamic funding rate. This structure allows for uninterrupted trading, but crucially, the funding rate itself becomes the market’s price for weekend liquidity and directional risk to market makers. For market makers, this rate represents a necessary premium for operating without real time hedging capabilities during the weekend.

| Metric | Ostium | Trade.xyz |

| Core Model | Pool based, Peer to Pool. Oracle price is execution price. Passive, zero slippage fills. | Orderbook, Peer to Peer. Price discovery via matching. Active, potential for slippage. |

| Pricing Authority | Oracle Driven. The oracle feed dictates the execution price. | Market Driven. Execution price is set by order book dynamics. Oracle is for risk parameters. |

| I. During Normal Trading Hours (9:30 AM – 4:00 PM ET) | ||

| Oracle Data Source | Stork (Live Bid/Ask). Pulls top of book quotes directly from Nasdaq/NYSE. | Pyth (Aggregated Spot). Pulls an aggregated reference price from multiple sources. |

| Pricing & Execution | CFD like model. Users trade directly at the oracle price, regardless of order book depth. Pro: No slippage for large orders. Con: Completely dependent on oracle quality. | Exchange Model. Users must be matched with a maker on the order book. Pro: True price discovery. Con: Might have slippage when depth is low. |

| Counterparty & P&L | The counterparty is the liquidity pool (OLP). P&L is calculated based on the change in oracle price. Hedging is managed by an off-chain MM for the entire pool. | The counterparty is another user or market maker. P&L is calculated based on execution prices. Hedging is the responsibility of the MM for each fill. |

| II. During After-Hours (4:00 PM – 9:30 AM Next Day) | ||

| Operational Status | Closed for trading. | Open for trading (After-Hours Mode). |

| Data Source & Pricing | No new data. P&L is frozen at the 4:00 PM closing price. | ATS Data (e.g., Blue Ocean). Pulls real execution prices from after-hours trading systems. |

| Risk Management Logic | A risk-averse strategy. The protocol assumes after-hours liquidity is too thin and prone to manipulation, choosing to halt trading to protect LPs. | A liquidity premium strategy. The protocol allows trading but spreads typically widen to compensate for lower liquidity. |

| III. During Weekends (Friday Close to Sunday) | ||

| Operational Status | Closed for trading. | Open for trading (Internal Pricing Mode). |

| Data Source | No external data. | No external data. The system generates an internal price. |

| Core Pricing Mechanism | N/A | A Game-Theoretic Model based on: 1. EMA of recent on-platform trades. 2. Discovery Bounds (e.g., ±5%) to limit deviation from Friday’s close. 3. Funding Rates to economically incentivize convergence. |

| MM Hedging Strategy | No hedging required as no trades occur. | Unhedged exposure. Market makers run naked risk over the weekend, compensated through extremely wide spreads and high fees. |

PS: It is important to note that Trade.xyz uses a different pricing logic for equity indices (like XYZ100, tracking the Nasdaq-100) compared to single stocks. For indices, it does not reference the spot index price directly. Instead, it uses index futures contracts (like CME’s NQ futures) which have much longer trading hours (nearly 23 hours a day). This design is necessary because spot indices stop updating after the market closes, whereas futures remain liquid. Trade then applies a cost-of-carry model to the futures price to derive a theoretical spot price.

4. Centralized Exchanges: The Pivot Toward Multi-Asset Liquidity Hubs

CEXs are accelerating a strategic transition from crypto native platforms toward “all-asset exchanges,” integrating traditional financial underlyings through RWA perpetuals. Bitget’s TradFi expansion typifies this trend, now supporting over 100 equities, FX pairs, and commodities. In 2025, its tokenized U.S. equity futures reached $10 billion in cumulative volume, with peak daily turnover exceeding $2 billion following the full launch of its TradFi section. Gate.io has similarly diversified into U.S. Treasury ETFs (TLT), gold ETFs (IAU), and 45 U.S. equities, driving platform-wide open interest to $10.4 billion by early 2026. Other major venues, including Binance, OKX and Bybit, have expanded their offerings to include high leverage precious metals and equity-linked CFDs, with OKX specifically rebranding its metals suite to anchor directly to spot gold and platinum prices.

Market performance indicates that macro volatility remains a primary driver of demand; for example, the 67% appreciation in gold prices during 2025 catalyzed a surge in monthly RWA perp volumes, which surpassed $20 billion by early 2025. These instruments maintain price parity with underlyings via funding rate mechanisms and apply tiered leverage caps tailored to asset class volatility: FX up to 500x, precious metals at 50x, and U.S. equities between 5x and 20x.

From a regulatory and risk perspective, these products are usually structurally managed as CFDs. Operations are typically localized within compliant subsidiaries in jurisdictions such as Abu Dhabi or Mauritius to minimize direct securities regulatory exposure.

5. Navigating Regulatory Constraints for RWA Perps

5.1 Understanding U.S. Derivatives Regulation

Within the U.S. regulatory framework, the classification of an underlying asset is the primary determinant for a derivative’s compliance path. This classification dictates jurisdiction and the necessary licensing for any venue. For assets generally treated as commodities such as gold, silver, FX, and Bitcoin—perpetuals on these underlyings fall under CFTC jurisdiction. This path is relatively straightforward, typically requiring registration as a Designated Contract Market (DCM) or Swap Execution Facility (SEF).

However, the regulatory landscape shifts dramatically when the underlying asset becomes a single stock or a narrow based security index. Derivatives on such assets must navigate joint jurisdiction between the SEC and CFTC. This dual regulatory oversight is the fundamental reason compliant retail stock perpetuals are effectively absent in the U.S. market. The historical precedent is the 1982 Shad-Johnson Accord, stemming from an SEC and CFTC jurisdictional dispute over stock futures. This accord broadly banned exchange-traded single-stock futures and narrow-based index futures. While the Commodity Futures Modernization Act of 2000 (CFMA) later permitted “Security Futures Products” (SFPs), it imposed stringent conditions: these products must be jointly regulated by both the SEC and CFTC. This dual-regulation requirement has become a significant legal impediment to equity derivatives innovation.

Any platform aiming to offer equity perpetuals to U.S. retail clients must therefore secure two distinct registrations:

- Register with the CFTC as a DCM or SEF.

- Register with the SEC as a National Securities Exchange.

Complying with two sets of potentially conflicting standards for margin methodology, disclosures, and trade reporting creates substantial burdens. The cumulative compliance and operating costs effectively act as a de facto barrier to entry, explaining the scarcity of compliant U.S. retail equity perpetual products.

5.2 Compliance Hurdles: The Friction of Legacy Tiered Frameworks

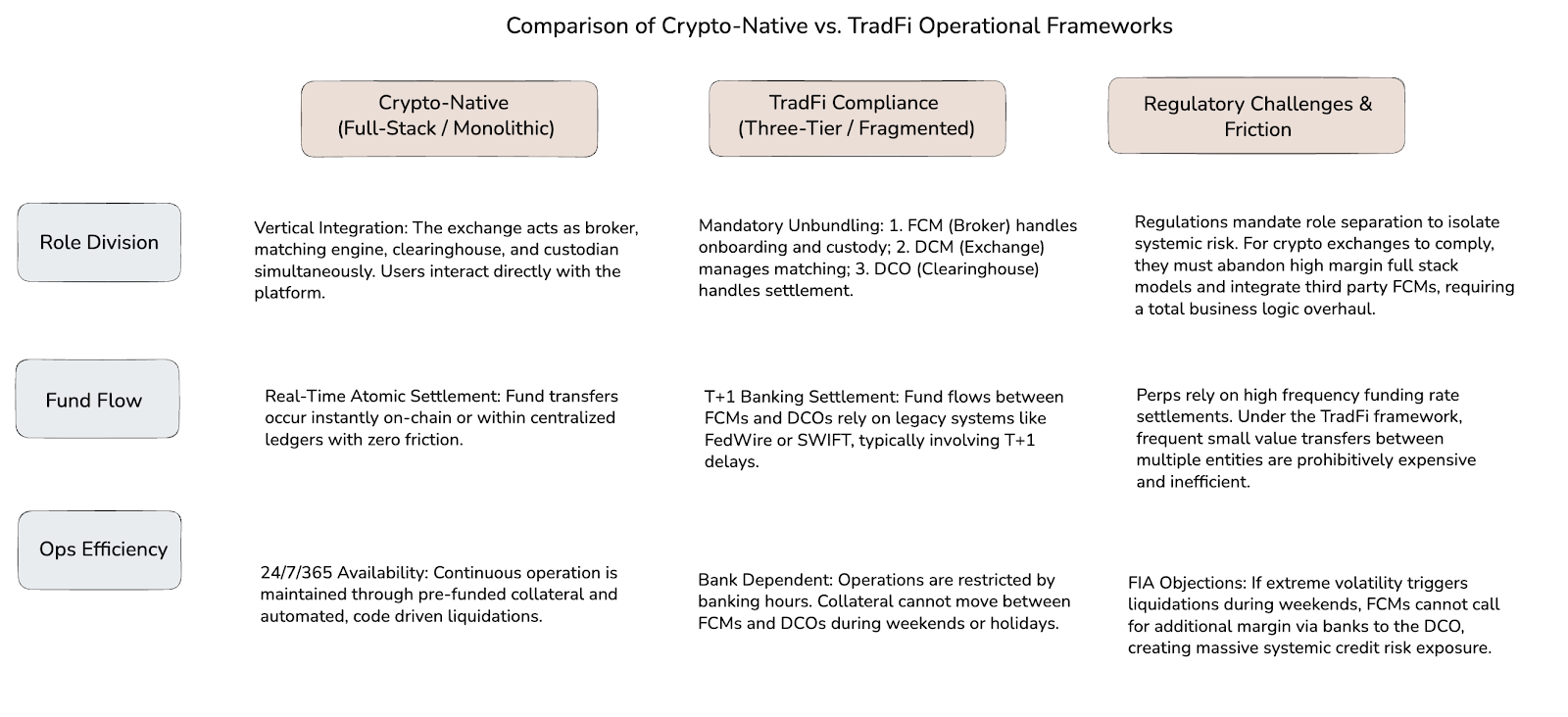

Beyond licensing, U.S. venues like Coinbase or Robinhood would face a fundamental infrastructure architecture conflict when considering equity perps. Crypto exchanges typically operate with vertically integrated, monolithic systems. U.S. regulations, conversely, emphasize a risk-isolated “three-layer separation.” To become compliant, a crypto exchange would need to unbundle its integrated stack and adapt to traditional clearing workflows.

The core mismatch lies between crypto’s native real-time systems and TradFi’s layered, batch-processed, and risk-isolated structures. Launching equity perps in the U.S. thus requires solving not only the dual-licensing issue but also the physical incompatibility between 24/7 trading demand and non-24/7 banking settlement. This infrastructure divergence represents a major bottleneck.

5.3 The Offshore Window: Leveraging Regulation S

Given the significant hurdles to U.S. domestic compliance, most equity perp liquidity has gravitated offshore. Offshore exchanges, serving non U.S. clients, often leverage Regulation S to obtain exemptions under U.S. securities law. This regulation permits securities offerings outside the U.S. without SEC registration, provided there are no directed selling efforts to U.S. persons. Effectively, platforms must implement strict geofencing and legal terms prohibiting U.S. users.

This regulatory environment creates a unique opportunity for RWA perp DEXs. They can partner with offshore long-tail brokers, establishing a mutually beneficial distribution model. Brokers facing tightening leverage restrictions in their home markets can leverage onchain perpetuals, which often exist in a definitional gray zone and can offer higher leverage.

More importantly, brokers can retain client relationships while outsourcing complex margin management, liquidation, and hedging risks to onchain protocols, significantly reducing their back-office burden. The DEX’s self-custody design also addresses trust concerns regarding smaller brokers mismanaging client funds. For an equity perp DEX, this model resolves a critical distribution challenge, as crypto-native users often have less interest in U.S. equities than traditional retail investors. By serving as the technical backend, the DEX remains technology-neutral, while compliant brokers handle KYC/AML, facilitating scaled growth.

Despite the commercial logic of the offshore + DeFi model, it remains exposed to U.S. “long-arm jurisdiction.” If an offshore protocol cannot technically or compliantly sever ties with U.S. users, or if its commercial activities are deemed to target the U.S. market, it can still face significant enforcement risk.

6. The Long Game: Market Convergence and the 24/7 Future

ICE’s plan to launch a 24/7 trading market for U.S. equities forces a structural shift in the RWA perpetuals sector. Some people are concerned continuous trading on regulated incumbent venues might remove DeFi’s exclusive advantage on always-on liquidity. As this baseline advantage normalizes, onchain protocols must shift their focus toward features legacy systems cannot structurally support.

The impending arrival of 24/7 TradFi infrastructure outlines a clear roadmap for ecosystem evolution and integration:

- Differentiation Beyond Availability

Traditional exchanges are moving toward tokenized infrastructure, including stablecoin funding, multi-chain custody, and T+0 settlement. To maintain product-market fit, RWA perps must compete on structurally distinct variables. The DeFi value proposition will narrow to areas where incumbent compliance frameworks restrict innovation: offering higher leverage, maintaining permissionless global access, and enabling cross-protocol composability. - Solving the Pricing Discontinuity

A continuous, regulated spot price stream directly addresses the primary headwind for synthetic RWAs: weekend liquidity vacuums. An open underlying market eliminates Monday opening gaps, reduces oracle manipulation risks, and compresses arbitrage costs. This continuous feed allows onchain market makers to hedge effectively at all hours, driving tighter spreads and deeper liquidity across decentralized order books. - A Coopetitive Financial Stack

The medium-term outlook points to deep structural integration. The market is configuring into a tiered ecosystem. Compliant, institutional venues like the NYSE are positioned to provide high-trust, foundational spot liquidity and pricing logic. Concurrently, DeFi protocols will operate as the high-velocity execution layer for directional risk and global portfolio construction. - Forward Outlook

The migration of financial infrastructure onchain remains a definitive trend. The window before potential legacy launches in 2026 is critical for crypto native projects to establish distribution moats and refine their execution engines. As traditional and crypto markets converge through atomic settlement and real-time pricing, RWA perpetuals will transition from a niche derivative to the permanent, underlying layer connecting global liquidity pools with Wall Street.

The post Trade Everything, Always: RWA Perpification as the Missing Layer Between DeFi and Wall Street appeared first on BeInCrypto.