TIYlab Macro vs 5 Black Swans: 8 Years of Discipline Tested

--

A backtest across COVID, Terra/Luna, FTX, SVB and the ETF rally — including the one window where the strategy underperformed Buy & Hold.

Why This Article Exists

On May 7, we published a piece on the “cost of discipline.” The core argument was simple: an algorithmic strategy that steps aside during prolonged bear markets will sometimes miss part of a recovery. Not every decision to go to cash will be vindicated by what follows. Sometimes the market recovers before the regime signal turns back, and you lag behind a passive investor who simply held through the chaos.

That article laid out a philosophy. This one tests it against five specific moments in Bitcoin’s history.

We took Macro v5.2 — the same strategy running live for TIYlab clients since April 2026 — and ran it through 5 historical stress windows. Five moments where the question was real: what would this algorithm have done during Bitcoin’s most severe crashes and most explosive rallies?

We present all five windows, including the one where the strategy produced a lower final return than Buy & Hold. That one is the most instructive.

*Backtest. Past performance does not guarantee future results. This is not financial advice. Cryptocurrency trading involves substantial risk of loss.*

— -

Methodology

Strategy: Macro v5.2, commit `fee1c3e`, deployed May 5, 2026.

Configuration:

- Trailing stop: 40% (activates after 20% gain from entry)

- Derisk tier 1 trigger: +170% from MA reference

- Hedge short trigger: -25% intra-drawdown from peak

- Bear market rally sleeve: 60% of equity

- DEV-1 stop loss: 12.5% maximum loss from entry

Capital reference: $1,200, equivalent to the 60% Macro allocation on a $2,000 total sleeve.

Anti-lookahead: For each scenario, spot data was loaded from January 2010 onward, ensuring the 200-day simple moving average was fully computed before the scenario window began. No future data was used in any calculation.

Fees and slippage: 0.10% taker fee + 0.02% slippage — identical to the production backtest configuration.

Source of truth: The same walk-forward validated configuration that produced Sharpe 1.14, +2,036% return, and -42% maximum drawdown over the 8.1-year full period (2018–2026).

— -

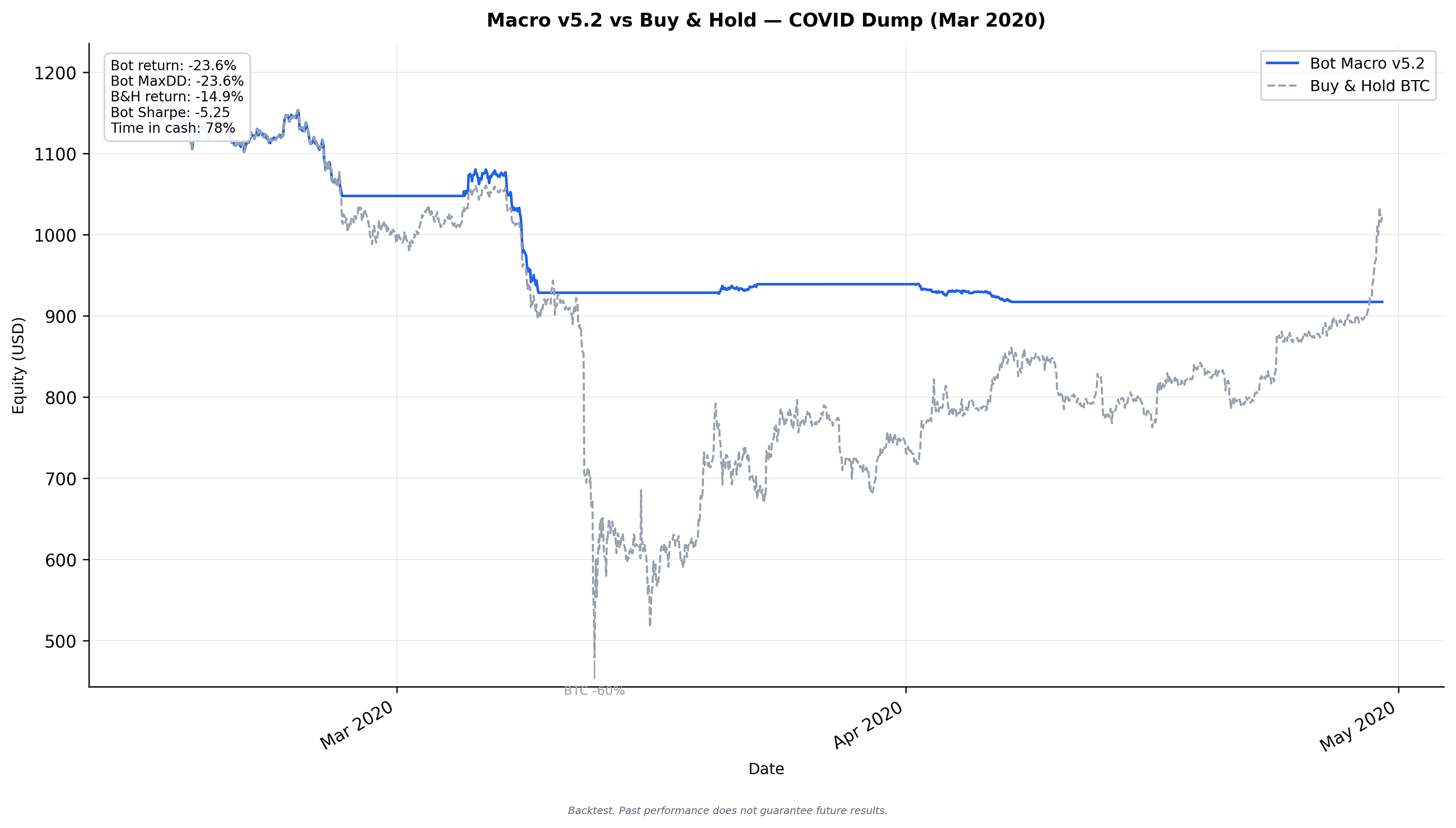

Black Swan #1 — COVID Dump (February–April 2020)

Bot Macro v5.2: -23.6% | Buy & Hold: -14.9%

Bot MaxDD: -23.6% | B&H MaxDD: -60.0% | Time in cash: 78%

This is the most complex result in this series, and we are presenting it first.

The strategy produced a lower final return than Buy & Hold by approximately 9 percentage points. That is accurate, and it belongs at the top of this scenario.

Here is what the window looked like. On February 15, 2020, Bitcoin was trading near $10,000. The strategy was in confirmed BULL regime — the 200-day SMA signal was positive, a long position was held. On March 12, Bitcoin fell approximately 50% in a single session, reaching a low near $3,800. The strategy moved toward cash and a BEAR regime posture.

The problem was what followed. Bitcoin recovered from $3,800 to approximately $8,800 by April 30 — a +130% move in roughly seven weeks. Buy & Hold participated in the full journey: the crash, the bottom, the recovery. Net result: -14.9% from the February 15 starting price. The strategy, having shifted to BEAR mode during the crash, did not fully re-enter before the window closed. Seven trades were executed; two long positions and five bear-market rally attempts. Net result: -23.6%.

The key number to hold alongside that is the intra-window maximum drawdown.** Buy & Hold’s maximum drawdown during this window was -60.0%. An investor who simply held watched $1,200 fall to approximately $480 at the bottom. The strategy’s maximum drawdown was -23.6% — it never experienced that trough.

The V-shaped recovery that followed is historically anomalous in its speed. A -62% intraday crash followed by a full recovery in seven weeks reflects the specific circumstances of March 2020: central bank balance sheet expansion and fiscal stimulus on a scale and pace not seen before, compressing what in prior cycles had been a multi-month recovery process into weeks. That context existed outside the price signal. The algorithm had no mechanism to anticipate it.

This is the cost of discipline in a V-shaped recovery. The strategy limits the depth of the drawdown at the expense of full participation in a rapid rebound. Over a 74-day window ending at an unusual inflection point, that tradeoff shows up as underperformance. Over a full cycle with prolonged bear markets — which is what most bear markets are — the calculus is different.

— -

Black Swan #2 — Terra/Luna Collapse (April–July 2022)

Bot Macro v5.2: +0.0% | Buy & Hold: -49.0%

Bot MaxDD: 0.0% | B&H MaxDD: -58.3% | Time in cash: 100%

By April 2022, Bitcoin had already been in a prolonged structural downtrend since the November 2021 peak. The strategy’s regime signal had confirmed BEAR well before this scenario window opened.

When UST depegged on May 9, 2022 — triggering one of the most rapid collapses in crypto market history, with over $40 billion in value erased within days — the strategy was already in cash. Not because it anticipated UST. Because the SMA200 regime filter had already concluded, from price alone, that sustained long exposure to Bitcoin was not warranted.

The strategy maintained 100% of starting capital throughout the full three-month window. Zero trades, zero fees, zero drawdown. Buy & Hold ended at $612 on a $1,200 starting position — a -49.0% return, with a maximum intra-window drawdown of -58.3%.

This is what the regime filter is designed for: not to predict specific events, but to identify when the structural trend has deteriorated sufficiently that BTC long exposure carries heavily asymmetric risk. Terra/Luna was confirmation of a signal already present, not the cause of a new one.

The flat blue line in the chart below tells the full story.

— -

Black Swan #3 — FTX Collapse (October–December 2022)

Bot Macro v5.2: +0.0% | Buy & Hold: -13.9%

Bot MaxDD: 0.0% | B&H MaxDD: -27.0% | Time in cash: 100%

Seven months after Terra/Luna, FTX filed for bankruptcy on November 11, 2022. Bitcoin fell approximately 25% in a single week — from near $21,000 to $16,000 — before continuing lower through December.

The mechanism was identical: the strategy had confirmed BEAR regime in early 2022 and remained in cash throughout the FTX window. A second stress test of the same signal, on a market already under structural pressure.

The strategy maintained full starting capital. Buy & Hold ended the window at $1,033 — a -13.9% return, with a maximum intra-window drawdown of -27.0%.

What the FTX result illustrates is that the regime filter does not require the strategy to identify the specific catalyst. It does not need to know what FTX is, or that it is about to fail. The price-based signal had already concluded that the environment was structurally adverse for a long-only position. The specific event became irrelevant to the position state.

The bot’s equity line was flat from October 15 to December 31. The B&H line peaked briefly, then dropped sharply as the news broke.

— -

Black Swan #4 — SVB Banking Crisis (February–April 2023)

Bot Macro v5.2: +26.7% | Buy & Hold: +36.8%

Bot MaxDD: -15.2% | B&H MaxDD: -21.8% | Time in cash: 0%

The SVB scenario is structurally different from the previous three. By February 2023, the strategy’s regime signal had confirmed BULL. The strategy was fully invested throughout the 59-day window — 0% time in cash.

When Silvergate, Silicon Valley Bank, and Signature Bank failed across a single week in March 2023, Bitcoin initially fell alongside traditional risk assets. The strategy, holding a BULL long position, experienced a maximum drawdown of -15.2% during the correction phase — lower than Buy & Hold’s -21.8%.

What followed was a sharp BTC recovery, driven in part by a narrative shift toward Bitcoin as an asset outside the traditional banking system. The strategy captured +26.7% over the window. Buy & Hold captured +36.8%.

The difference is explained by the derisk mechanism. As BTC moved higher, the strategy partially reduced exposure at certain price levels, then did not fully re-add at the lows before the rally accelerated in April. This produced a different return profile from Buy & Hold: lower maximum drawdown (-15.2% vs -21.8%), and lower final return on this specific window (+26.7% vs +36.8%).

Both lines end above the starting capital. The strategy was not in cash when the BULL window arrived.

— -

Black Swan #5 — ETF Approval Rally (December 2023–April 2024)

Bot Macro v5.2: +52.9% | Buy & Hold: +73.4%

Bot MaxDD: -21.4% | B&H MaxDD: -20.2% | Time in cash: 0%

The fifth scenario is deliberately a strong bull rally. It is here to answer a direct question: does the strategy participate when the BULL confirmation arrives?

The strategy was in confirmed BULL regime entering December 2023 and held a single long position throughout the full 137-day window. Bitcoin moved from approximately $38,000 to a peak near $73,000 before pulling back to approximately $63,000 by April 15. Buy & Hold captured the full round trip: +73.4%.

The strategy returned +52.9% — approximately 72% of Buy & Hold’s gain over the window.

The maximum drawdown figure warrants a note. The strategy’s MaxDD (-21.4%) was marginally wider than Buy & Hold’s (-20.2%). The difference is attributable to nine bear-market rally short trades executed during the significant correction in late January and early February 2024. That correction, which approached -20% from the local peak, proved temporary. The short trades, sized appropriately for a bear-regime context, were less effective inside a sustained bull market. The additional 1.2 percentage points of drawdown is the observable cost.

The strategy captured 72% of Buy & Hold’s upside during one of the strongest four-month BTC rallies since 2021. Fully invested from day one of the confirmed BULL window through the full duration.

— -

What This Means

Five windows. One where the strategy produced a lower final return than Buy & Hold. Two where it maintained full starting capital while Buy & Hold lost between 14% and 49%. Two where it held exposure through confirmed bull markets, capturing between 73% and 72% of Buy & Hold’s upside.

The pattern is consistent with the design.

The strategy is not optimized for V-shaped recoveries. The COVID result makes that explicit. A crash followed by a complete recovery in seven weeks — before the regime signal has time to confirm the new trend — produces underperformance. That is a genuine cost, and it is bounded by what we can observe: the strategy’s maximum drawdown in that window was -23.6%, while Buy & Hold’s was -60.0%. The cost of missing the V-recovery is approximately -9 percentage points in final return. The cost of riding the full crash, if the recovery had not materialized in that window, would have been significantly larger.

The strategy is designed to reduce exposure during prolonged structural bear regimes. Terra/Luna and FTX occurred inside a twelve-month crypto bear market. The signal had time to confirm. In those windows, maintaining cash for the full duration meant not participating in losses of -49% or -14%.

SVB and ETF show the other side of the same mechanism: when the regime confirms BULL, the strategy deploys capital. It does not generate identical returns to Buy & Hold over short windows — the derisk mechanism and trailing stop cost some percentage points at the edges. But the position is held through the core of the trend.

The honest framing is not that this strategy produces better returns than Buy & Hold in every window. It does not. The framing is that it produces a different return profile across market regimes — one that historically, over a full 8.1-year cycle including multiple prolonged bear markets and multiple confirmed bull runs, has generated a Sharpe ratio of 1.14 and a cumulative return of +2,036% on a $1,200 starting sleeve.

That is a backtest result. It covers one specific historical period. The next eight years will have their own V-recoveries, their own prolonged bears, their own black swans that the regime signal will handle well and some it will handle poorly.

The cost of discipline is real. So is the alternative.

— -

Disclaimer

Backtest. Past performance does not guarantee future results. This is not financial advice. Cryptocurrency trading involves substantial risk of loss. Results presented here are simulated using historical data and the Macro v5.2 configuration deployed May 5, 2026. Live trading results will differ due to execution conditions, exchange-specific fees, slippage, and market liquidity. The strategy involves derivative positions and short-selling risk not fully captured by simulation.

— -

About TIYlab

TIYlab is an algorithmic trading service for Bitcoin. The TIYlab Pack combines three automated strategies — Macro (60%), DCA (10%), and Funding Rate Harvester (30%) — running on a single capital sleeve with live execution since April 6, 2026.

[tiylab.com](https://tiylab.com)