Member-only story

The Trader Who Never Starts

Javier Santiago Gastón de Iriarte Cabrera17 min read·Just now

Javier Santiago Gastón de Iriarte Cabrera17 min read·Just now--

How a 2026 Math Paper Exposes the Hidden Enemy Inside Every Discretionary Trader — and What to Do About It

12 min read·May 2026

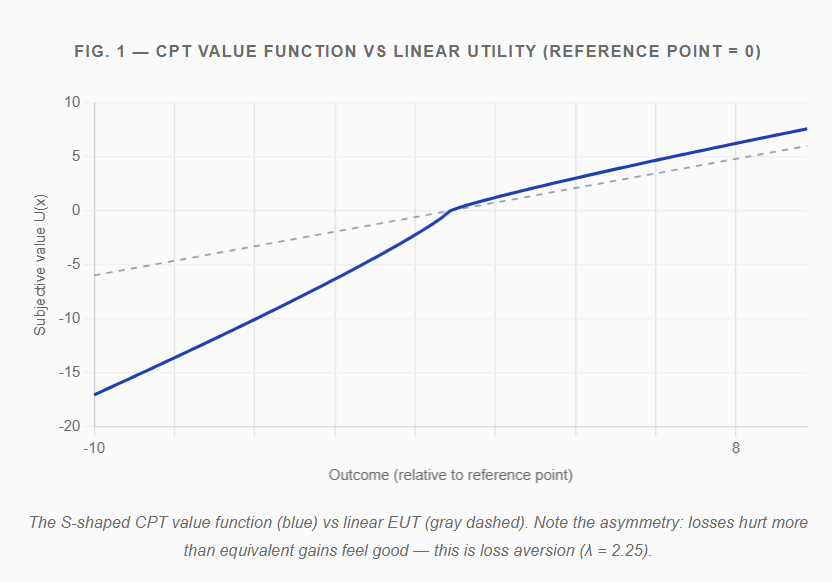

“A sophisticated prospect theory agent never gambles — even if expected gains are arbitrarily high.” — Ebert & Strack, Mathematical Finance, 2026

You’ve done your analysis. The setup is clean. Risk/reward looks great. And yet… you don’t pull the trigger.

Or worse: you enter, the trade goes your way, you’re sitting on a nice profit — and something makes you close it early. Then it keeps going without you.

Behavioral finance has a name for the second pattern: the disposition effect. But what about the first — the trader who never starts? Until recently, no one had a rigorous mathematical explanation for it.

In March 2026, Sebastian Ebert (Heidelberg University) and Philipp Strack (Yale University) published a result that should shake every discretionary trader. Their paper, “Never, Ever Getting Started: On Prospect Theory Without Commitment,” proves — formally, mathematically — that a rational prospect theory agent aware of their own biases will never enter a trade, even when expected profits are enormous.

This article explains why. Then it shows how building an algorithmic EA in MQL5 solves the problem entirely — and why that solution is itself implied by the mathematics.

· · ·

Part 1