Member-only story

The Mirage of PTC: When a Beautiful Backtest Hides a Broken Strategy

A story about a strategy that looked perfect — until reality tested it.

Kryptera9 min read·Just now

Kryptera9 min read·Just now--

Act I: Love at First Backtest

Every quant knows the feeling. You run the numbers, the equity curve climbs, and for a moment, you believe you’ve found something real.

import pandas as pd

import numpy as np

import yfinance as yf

import vectorbt as vbt

# -------------------------

# Download Data

# -------------------------

symbol = "PTC"

start_date = "1960-01-01"

end_date = "2030-01-01"

interval = "1d"

df = yf.download(symbol, start=start_date, end=end_date, interval=interval, multi_level_index=False)

df.reset_index().to_csv("PTC_clean.csv", index=False)

# -------------------------

# Necessary Parameters

# -------------------------

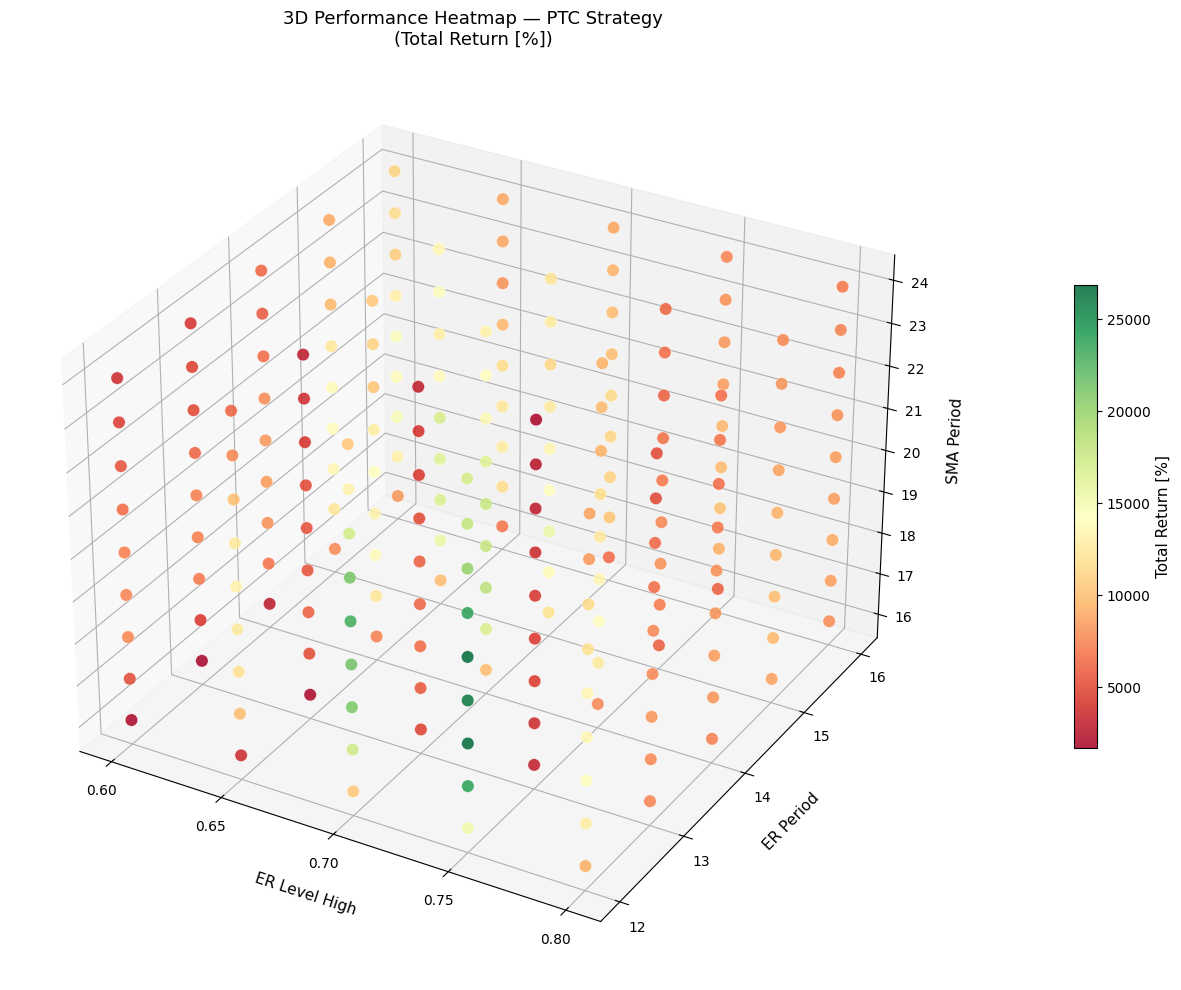

ER_LEVEL_HIGH = 0.7

ER_PERIOD = 14

SMA_PERIOD = 20

# -------------------------

# Indicator Functions

# -------------------------

def close_cross_below_sma(df, period=SMA_PERIOD):

"""

Close price crosses below the SMA

"""

df = calculate_sma(df, period)

return (df['Close'] < df['SMA']) & (df['Close'].shift(1) >= df['SMA'].shift(1))

def calculate_sma(df, period=SMA_PERIOD):

"""

Calculate Simple Moving Average (SMA) of the Close price.

"""

df = df.copy()

df['SMA'] =…