The Eternal Rite

Sanctum7 min read·Just now

Sanctum7 min read·Just now--

A walk-through of the mechanism, the math, and the game theory behind a token whose floor only rises.

The Floor is Sacred. That is the brand line, and it is also the math.

SANCTUM is a reserve-backed ERC-20 on Ethereum mainnet, hard-capped at 462,500 tokens, whose floor — the on-chain redemption value of a single token — is a single ratio: USDC reserves divided by SANCTUM supply. Every protocol action either grows the numerator, or shrinks the denominator, or leaves both unchanged. There is no action that reduces the ratio. The rest of this essay is the proof, walked at reading pace, with the names the contract uses.

We will name the parts. We will move through them in the order a token does. Then we will look at the whole as a game, and ask the question that matters: given the incentives, what does every participant actually do — and where does it leave the floor?

The Doctrine

Three lines describe the entire protocol.

Supply rises and falls.

Reserves rise and fall.

The floor only rises.

The first two lines are the elastic surface. Supply was forged in Phase 1 and is now fixed; it falls when a Keeper surrenders or a vow burns. Reserves grow with every toll and shrink only when a Keeper redeems. The third line is the invariant.

Intrinsic value — reserves divided by supply — moves in only one direction, monotonically, by construction. The math of the contract makes this so. The rest of the essay is the why.

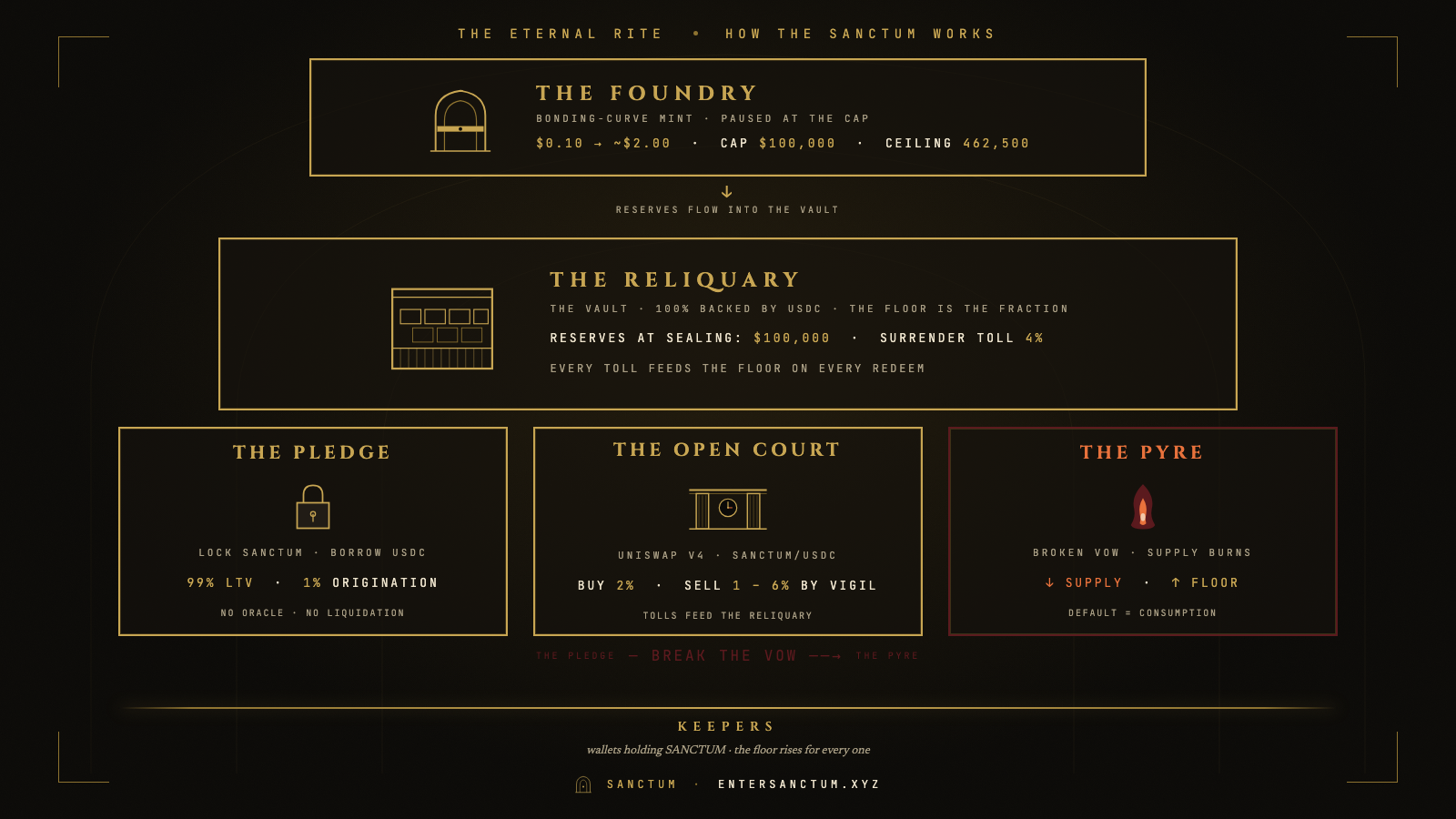

The Foundry and the Sealing

The Foundry is the bonding-curve mint that brought SANCTUM into existence. It is the only path through which the token has ever entered circulation. The mint price is a deterministic, monotonically-rising function of total supply forged so far. The first SANCTUM was forged at $0.10. The last was forged near $2.00.

The cap was $100,000 of cumulative buy-in. When that cap filled, the contract emitted a final event, paused itself at the cap, and locked the supply ceiling at 462,500. This moment is called the Sealing. From the Sealing on, supply can never exceed 462,500 — the cap is the absolute ceiling. The Foundry may reopen later, only to refill SANCTUM that has burned via default, never to mint past the ceiling. The cap does not move.

The Order — the team behind the protocol — seeded the curve at the opening with $25,000 of curve participation. Same contract. Same prices. No allocation outside the bonding curve, no minting from thin air. The remaining $75,000 of the cap was filled by public forgers. From the contract’s perspective, every SANCTUM in circulation was acquired by paying the curve price at the moment of its mint.

At the Sealing, intrinsic value was the average curve price weighted by buy-in:

$0.2162 per SANCTUM.

That is the floor as Phase 2 began. It has only risen since.

The Two Wards

The Reliquary is the on-chain vault. It is where the reserves live and where redemption is paid. The Wards are the Uniswap V4 hook that gates every swap in the SANCTUM/USDC pool — call it the Open Court. There are two of them.

The Ward of the Threshold is the entry toll. Every buy in the Open Court is charged 2% of the USDC paid in. The toll flows directly to the Reliquary at swap time. Reserves grow; supply is unchanged at the moment of the buy; intrinsic value rises before the trade settles.

The toll is flat. It does not depend on who you are, how long you have held, or what wallet you are using. The protocol does not classify Keepers; it charges entry.

The Ward of the Offering is the exit toll, and it is not flat. The toll on a sell is paid by the Vigil — the seller’s clock, which measures time since the wallet last sent SANCTUM out.

Same block: 6%.

Less than 7 days: 4%.

7 to 14 days: 3%.

14 days or more: 1%.

The Vigil has diamond-hand semantics. Buying more SANCTUM never resets it. Receiving from a friend never resets it. Only an outgoing transfer — a sell, a peer-to-peer send, a surrender to the vault — resets the clock to zero. Moving tokens to a fresh wallet does not help; the new wallet starts at the same-block tier, paying 6% on its first sell.

A flat sell toll would tax every exit equally, including patient ones. The Vigil rewards holding without rewarding speculation about holding. The math is permissive to long-term Keepers — anyone holding SANCTUM — and punitive to wallet-hop wash trading. There is no shortcut to the 1% floor toll except actually holding.

The Reliquary’s Promise

The Reliquary keeps a second door open. Beyond trading in the Open Court, a Keeper can surrender SANCTUM directly to the vault for redemption at intrinsic value minus 4%. The 4% is retained by the Reliquary; reserves fall by less than supply, so intrinsic value rises with every surrender.

This second door is the protocol’s promise. Market price on Uniswap can drift above intrinsic value freely — speculators can bid the token up — but it cannot trade meaningfully below intrinsic-minus-4% for long. The arbitrage is mechanical: if the market price drops to intrinsic-minus-5%, buy on the Open Court, surrender at the Reliquary, walk away with a 1% spread. Arbitrageurs close gaps like that in minutes.

The Reliquary cannot become insolvent. USDC reserves and SANCTUM supply scale together; the redeemable value of all outstanding tokens is always at most equal to the reserves on hand. If every Keeper surrendered at once, each would receive their proportional share of reserves minus the 4%. The last to surrender would be paid at a floor that had been rising the entire time.

The Pledge and the Pyre

A Keeper can also lock SANCTUM as collateral and borrow USDC against it. This is the Pledge.

The terms are permissive. Borrow at 99% of the collateral’s intrinsic value, in USDC. Pay a 1% origination toll to the Reliquary at issuance. The toll feeds the floor. There is no oracle, no liquidation curve, and no margin call. There is only the vow’s expiry.

A global cap binds the system: no more than 50% of the vault’s reserves can be lent at any moment. This means a redemption rush always finds reserves waiting. It also means total outstanding loans never exceed the redeemable share of supply they were lent against.

The vow has two endings. A borrower can honor it: repay before expiry, the collateral unlocks, the toll has accrued. Or the borrower can break it: expiry passes, the locked SANCTUM is consumed by the Pyre.

The Pyre is the burn furnace. Default is not punishment. Default is consumption.

When SANCTUM burns at the Pyre, supply contracts. Reserves are unchanged from the burn itself — the loan principal was disbursed earlier — but the denominator of intrinsic value drops. The floor rises for every remaining Keeper.

The math of 99% LTV is permissive because SANCTUM is fully reserved. Lending USDC against a token whose backing is the same USDC carries no protocol-level risk, and the thin 1% margin gives the protocol an extra solvency cushion at every loan. If the borrower honors the vow, the protocol has been paid the origination toll. If the borrower breaks the vow, the protocol has been paid more — in supply contraction equivalent to the loan principal. Both endings serve the floor.

The Game Theory

Now look at every participant and ask: what is their best response?

The early forger paid $0.10 to $0.50 at the curve opening. They hold SANCTUM acquired below the eventual Sealing floor of $0.2162. They are the cohort whose Vigil has been ticking the longest. If they sell on the Open Court today, they pay the 1% floor toll. If they hold, the floor rises beneath them.

The late forger paid $1.50 to $2.00 in the last leg of the curve. They paid a premium for being last. If they sell early, they pay 6% on top of an entry price the market may not have caught up to yet. The Vigil rewards them for waiting until the market re-prices.

The panic seller dumps in the same block they bought. They pay 6%. That 6% feeds the Reliquary. Their panic raises the floor for every Keeper who did not panic. The Vigil ensures the cost of impatience is paid into the cohort, not extracted from it.

The patient holder waits. After 14 days of not transferring out, every sell costs them 1%. The protocol charges them less than the standard V4 LP fee on most chains.

The borrower locks SANCTUM, takes USDC at intrinsic, pays the 1% origination. The toll feeds the floor. If they honor the vow, the protocol has been paid.

The defaulter chose to walk away. The locked SANCTUM is consumed by the Pyre. They keep the borrowed USDC; the protocol gains the supply contraction. Their default is structurally identical to a surrender with the toll set to 100% — from the floor’s perspective, they paid the largest fee imaginable.

The arbitrageur keeps the Open Court tethered to intrinsic value. Every spread between market price and the redemption floor is closed for profit. The arbitrageur is paid for their work. The protocol is paid in tightened spread. The floor is unchanged by either, and rises every time a toll flows.

The liquidity provider earns the standard Uniswap V4 LP fee on every swap. The Wards’ tolls are separate from the LP fee and do not touch it.

There is no participant whose best response weakens the floor. There is no defection that costs the protocol. Defection costs the defector — and pays the cohort.

What if the price drops below the floor?

It can’t. That’s what floor means.

The Renouncement

The last move is the Renouncement. After Phase 2 stabilizes — once the Open Court is liquid, redemption has been exercised, and the Pledge market has cycled through its first vows — ownership of the contracts is permanently surrendered. The owner address is set to 0x000000000000000000000000000000000000dEaD. From that moment forward, no privileged caller exists. The contracts have no pause function, no mutable fees, and no upgrade path.

The view operatorRenounced() returns true after the transition. Anyone can verify the state, directly on Ethereum, without trusting the Order's word. The contract becomes the contract.

Close

Hard-capped at 462,500. Net deflationary. The floor only rises.

SANCTUM is novel on-chain software on Ethereum mainnet. Capital is at risk of total loss. Read the Codex at entersanctum.xyz. Follow the Crier at @EnterSanctum.