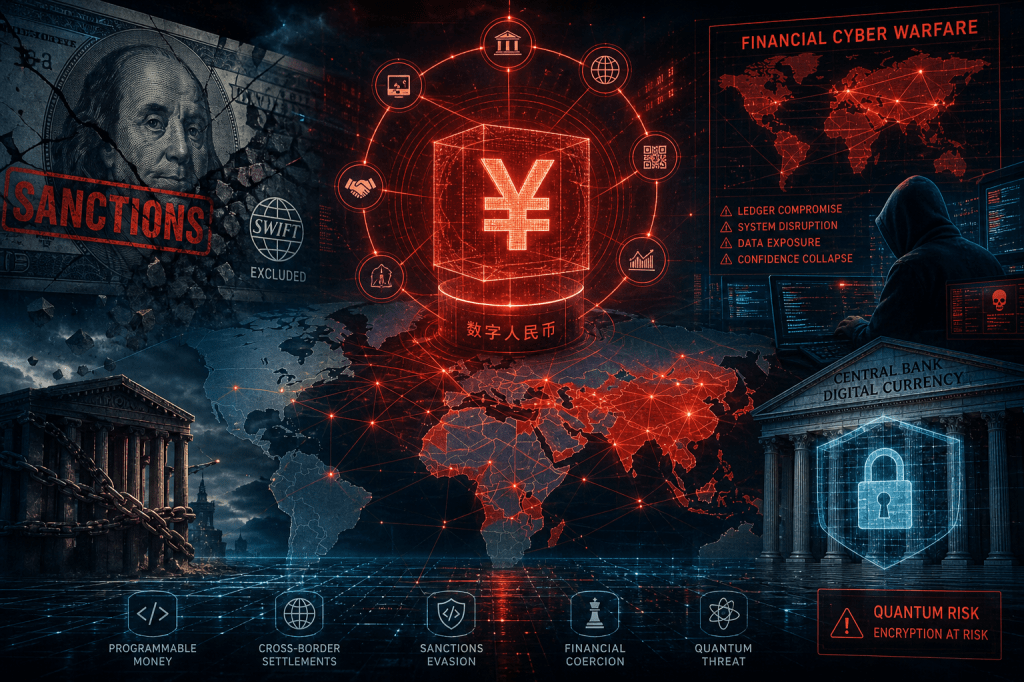

The CBDC Gambit: How Digital Currencies Are Becoming the New Tool of Financial Cyber Warfare

CCD-IS7 min read·Just now

CCD-IS7 min read·Just now--

More than 130 countries are developing digital versions of their currencies. They are also building the most centralised, most surveilled, and most attackable financial infrastructure in history.

By Vladimir Tsakanyan, PhD · Center for Cyber Diplomacy and International Security · cybercenter.space

In June 2025, the governor of a major central bank stood before a financial forum and declared, without naming its target, that in times of geopolitical tension, “the global dominant currency tends to be instrumentalized or weaponized.” He was describing the dollar. He was announcing an alternative. The digital currency his institution had been developing for over a decade had, by that point, processed more than $7.3 trillion in cumulative transactions across 29 cities, integrated with the settlement systems of ten regional neighbours and six Middle Eastern economies, and embedded itself into the daily payments infrastructure of the world’s most populous nation.

This was not a fintech announcement. It was a strategic declaration — the most consequential reshaping of the global financial architecture since Bretton Woods, delivered in the language of monetary policy and received, in most Western capitals, as a payments story.

It is not a payments story. It is a cyber warfare story. And the attack surface it is creating has no precedent in the history of financial conflict.

The New Geometry of Financial Power

The dollar’s dominance of the global financial system is not merely an economic fact. It is an instrument of state power — one that the United States has deployed with increasing assertiveness over the past two decades through sanctions, SWIFT exclusion, and asset freezes that can, with a decision made in Washington, cut a government off from the global economy with a speed no conventional military action can match.

That power depends entirely on the dollar’s centrality to international trade settlement. If cross-border transactions can be denominated, settled, and cleared in a digital currency that does not touch the dollar-denominated correspondent banking system, the enforcement mechanism dissolves. Sanctions become suggestions. Asset freezes apply only to the assets held within reach.

The digital yuan — fully programmable, interoperable across a growing network of allied and non-allied economies, and deliberately architected to settle transactions outside Western-controlled financial infrastructure — is designed, at its strategic core, to make this happen. Academic research published in late 2025 stated it plainly: the digital yuan functions both defensively, to insulate its issuing state from the risk of financial containment, and proactively, as a foundation for alternative settlement infrastructure that progressively displaces the systems through which Western financial coercion operates.

For sanctioned states that have shifted significant portions of their international commerce to yuan-based systems, the practical effect is already visible. Revenue streams that US financial surveillance cannot monitor. Trade flows that US authorities cannot interrupt. Oil settled outside the dollar system, generating income that sanctions were explicitly designed to deny.

The coercive power of Western financial statecraft is not being defeated militarily. It is being routed around digitally — one CBDC integration at a time.

Analyst note

The geopolitical significance of CBDC architecture is almost entirely absent from the public debate in Western democracies, which has focused overwhelmingly on domestic privacy concerns and the retail payments use case. These concerns are legitimate. They are also secondary to the strategic question, which is whether the global financial infrastructure through which democratic states project economic power will, within a decade, have been structurally bypassed by a parallel system whose design principles, governance standards, and data access regimes are set by a state with fundamentally different interests. The answer, on current trajectories, is yes. The conversation has barely begun.

The Attack Surface Nobody Is Discussing

The strategic ambition of CBDC development is matched, in equal measure, by the cybersecurity risk it creates — and the two are inseparable. The same centralisation that makes a CBDC a powerful tool of state financial power makes it an extraordinarily attractive target for state-level cyber operations.

Physical cash cannot be hacked. A distributed correspondent banking system, with its thousands of nodes, redundant infrastructure, and decades of security architecture, is difficult to attack at scale. A CBDC, by design, consolidates national monetary infrastructure into a centralised digital system — one that, if successfully penetrated, compromised, or disrupted, could produce consequences ranging from the exposure of every citizen’s financial transaction history to the operational paralysis of a nation’s payment system at a moment of the attacker’s choosing.

The IMF, in its assessment of CBDC cyber risk published in 2024, noted that digital currencies are materially more attractive targets for sophisticated cyber attackers — including nation-states — than existing payment systems, for three compounding reasons: the complexity of their interconnections increases the likelihood of exploitable vulnerabilities; their status as the national currency in digital form makes them uniquely high-value targets; and their wider, less cyber-risk-aware user base expands the attack surface through the human element that remains the most reliably exploitable entry point in any system.

A successful cyberattack against a CBDC does not need to steal funds to be strategically decisive. It needs only to compromise the integrity of transaction records — to introduce doubt about whether the ledger accurately reflects what it claims to reflect — to produce a crisis of confidence with systemic consequences. A population that cannot trust that its digital currency accurately records its balances has, in practical terms, no functioning currency. The attack is not on the money. It is on the trust that makes the money work.

Analyst note

The centralisation paradox is the feature of CBDC design that no issuing central bank has resolved. The same architecture that makes a CBDC governable — that allows the issuing state to monitor transactions, implement policy, and maintain control — is the architecture that makes it maximally vulnerable to a single point of catastrophic failure. Privacy-preserving designs that distribute data and reduce the central bank’s visibility reduce the attack surface but sacrifice the control that makes the instrument strategically useful. Every CBDC design decision is a trade-off between power and resilience. No issuer has found a configuration that preserves both.

Programmable Money as a Weapon

The most strategically significant feature of CBDC design is one that receives the least public attention: programmability. A CBDC is not simply digital cash. It is, by design, money that can be coded with conditions — constraints on how it can be spent, where it can be used, when it expires, and by whom it can be received.

In its defensive domestic application, programmability enables precise monetary policy transmission: stimulus funds restricted to domestic purchases, welfare payments limited to approved categories, negative interest rates applied directly to currency holdings rather than bank accounts. These are the applications that central bank economists discuss in published research.

In its offensive geopolitical application, programmability is a coercion tool with no analogue in conventional financial statecraft. A state that has established a CBDC as the settlement currency for bilateral trade relationships with dependent economies holds, in the programmability of that currency, a lever that can be activated remotely and with surgical precision. Trade flows can be suspended, credits can be voided, access to payment infrastructure can be revoked — not through the slow, negotiated, institution-dependent process of conventional sanctions, but through a code change executed at the central bank’s discretion and propagated instantaneously through the integrated network.

This is not a theoretical capability. It is the logical extension of the design principles that every CBDC issuer is currently implementing, applied to the international context that the most strategically ambitious CBDC programmes are explicitly designed to occupy.

The Quantum Horizon

Layered beneath all of the near-term cyber risks of CBDC deployment is a threat that most central bank security frameworks acknowledge but none has resolved: quantum computing’s implications for the cryptographic infrastructure on which digital currency security depends.

CBDC systems, like all digital payment infrastructure, rely on cryptographic mechanisms to protect transaction data in motion and at rest. Current encryption standards, which are computationally impractical to break with classical computers, become tractable problems for sufficiently advanced quantum computers. A state actor that achieves meaningful quantum advantage before CBDC cryptographic standards are updated holds the capability to intercept CBDC transactions, impersonate participants in the payment system, and potentially reconstruct historical transaction records that were encrypted under now-broken standards.

The timeline for quantum threat materialisation is contested, but the direction is not. The World Economic Forum has assessed that central banks must begin embedding cryptographic agility — the capacity to update encryption standards rapidly as threats evolve — into CBDC architecture now, because the infrastructure being deployed today will still be operating when quantum capabilities mature. Most central banks are not there yet.

A CBDC built on cryptographic standards that a future adversary can break is not a secure monetary system. It is a deferred vulnerability — one whose consequences, when they arrive, will be systemic.

Bottom Line Assessment

The global race to deploy central bank digital currencies is being conducted primarily as a monetary policy and financial inclusion exercise. It is, in its strategic dimensions, the construction of new infrastructure for financial warfare — infrastructure that can be used to project coercive power, to evade the coercive power of adversaries, and to attack the monetary systems of states that have made their currencies the foundation of their international influence.

The attack surface being created is without precedent. Centralised digital monetary systems, integrated across borders through interoperability arrangements that are being built faster than the security standards that should govern them, represent a target whose compromise would produce consequences — paralysis of payment systems, destruction of ledger integrity, exposure of the complete transaction histories of entire populations — that no previous financial cyberattack has approached.

The strategic competition over CBDC standards, architecture, and interoperability is a competition over which state’s financial coercion capability survives the digital transition and which state’s does not. It is being conducted in the open. Most of the governments whose interests are most directly at stake are not yet treating it as the security issue it is.

Digital money is the new battlefield. The fortifications have not been built. The adversary is already inside the perimeter.

CBDC · Financial Cyber Warfare · Digital Yuan · Dollar Hegemony · Sanctions Evasion · Financial Coercion · Cyber Risk · Monetary Policy · Vladimir Tsakanyan

Originally published at http://cybercenter.space on May 4, 2026.