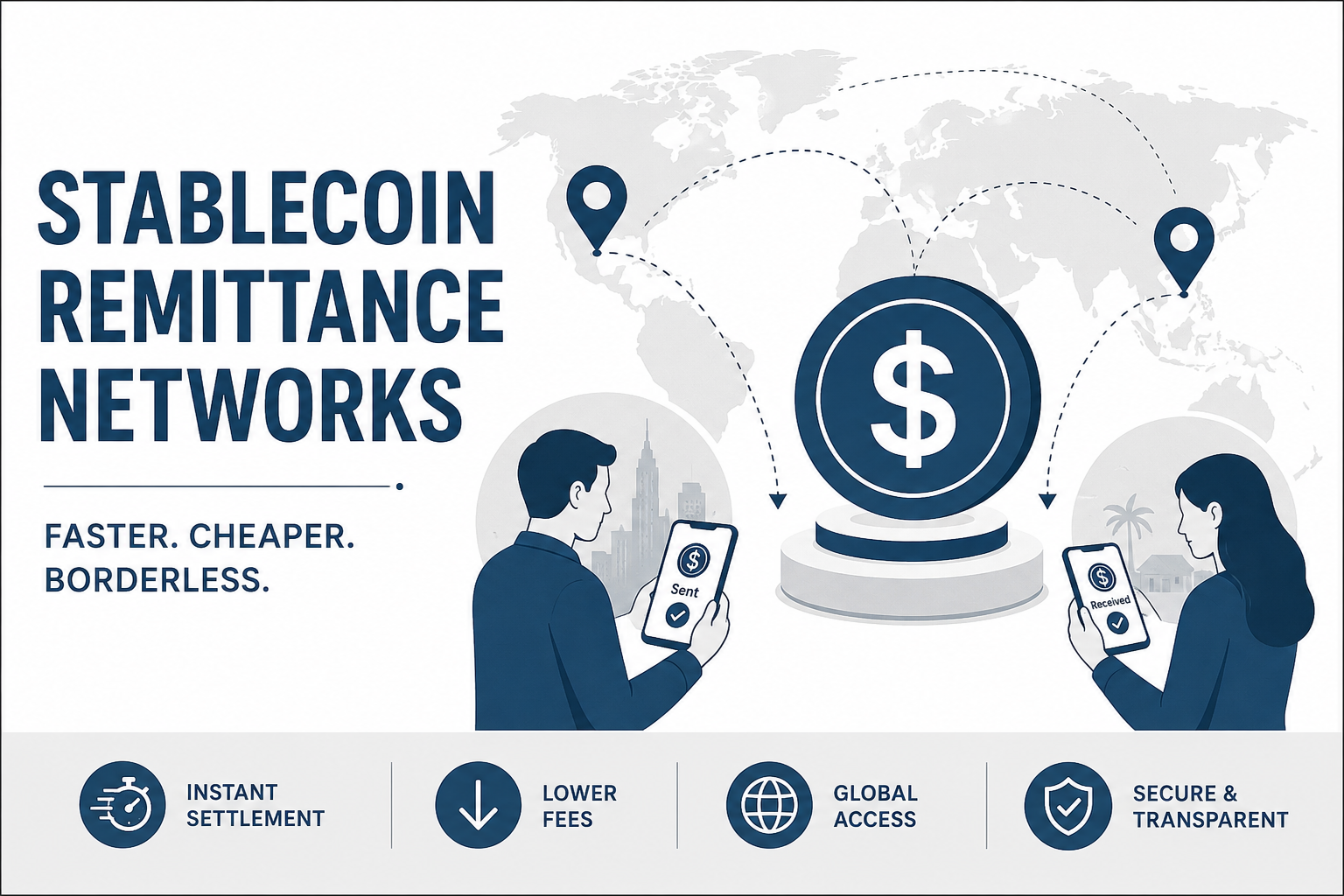

Stablecoin Remittance Networks

How Digital Dollars Are Rewiring Cross-Border Payments for Migrants, Startups, and Emerging Economies

Prashant Thinks6 min read·Just now

Prashant Thinks6 min read·Just now--

For decades, sending money across borders has been expensive, slow, and frustrating. Migrant workers often lose a significant percentage of their wages to transfer fees, while businesses wait days for international settlements to clear.

Traditional remittance systems rely on multiple intermediaries, legacy banking rails, and fragmented regulations that make global money movement inefficient.

Now, stablecoin remittance networks are emerging as a serious alternative.

By combining blockchain infrastructure with fiat-backed digital currencies, stablecoins are transforming how value moves internationally. What began as a niche crypto use case is rapidly becoming a practical financial tool for payroll, family remittances, merchant settlements, and cross-border commerce.

The appeal is straightforward:

- Faster settlement

- Lower fees

- 24/7 transactions

- Greater accessibility

- Reduced dependency on correspondent banking

But beyond the hype, stablecoin remittance networks are creating a structural shift in global finance.

This shift is especially important for emerging economies where millions remain underbanked yet connected through smartphones and digital wallets.

Why Traditional Remittance Systems Are Under Pressure

The global remittance market processes hundreds of billions of dollars annually. Yet the infrastructure behind it still resembles systems built decades ago.

A typical international transfer may involve:

- Sending bank

- Correspondent banks

- Currency conversion providers

- Clearing systems

- Receiving institutions

Each layer introduces:

- Processing delays

- Additional fees

- Compliance overhead

- FX markups

- Operational friction

For many migrant workers, sending even small amounts internationally can result in high transaction costs that directly reduce household income.

In some corridors, transfers can take several business days to settle. Weekend delays, banking holidays, and regional restrictions add further complexity.

Small businesses face similar pain points:

- Delayed supplier payments

- Limited access to global banking

- Expensive wire fees

- Liquidity constraints

- Settlement uncertainty

Stablecoin networks attempt to eliminate many of these inefficiencies.

What Makes Stablecoins Different

Stablecoins are blockchain-based digital assets pegged to traditional fiat currencies such as the US dollar or euro.

Unlike volatile cryptocurrencies, stablecoins aim to maintain consistent value through reserves, collateralization, or algorithmic mechanisms.

The most commonly used remittance stablecoins are fiat-backed tokens supported by cash or treasury reserves.

Examples include:

- USD-backed stablecoins

- EUR-backed stablecoins

- Region-specific digital fiat tokens

The key innovation is not simply digitized money. It is programmable settlement infrastructure.

Transactions can occur:

- Directly between wallets

- Across borders instantly

- Without multiple banking intermediaries

- With transparent blockchain verification

- Around the clock

This creates a fundamentally different model for global payments.

How Stablecoin Remittance Networks Work

A stablecoin remittance transaction usually follows a streamlined flow:

Step 1: Fiat On-Ramp

A sender deposits local currency through:

- Banking apps

- Fintech platforms

- Exchanges

- Mobile wallets

- Payment agents

The funds are converted into stablecoins.

Step 2: Blockchain Transfer

The stablecoins move across blockchain networks in minutes or seconds.

Depending on the infrastructure, transaction costs can remain extremely low compared to traditional international wires.

Step 3: Recipient Access

The recipient can:

- Hold the stablecoins

- Convert to local currency

- Spend digitally

- Withdraw through partner networks

- Use them for savings or commerce

This process bypasses several traditional settlement layers.

Why Emerging Markets Are Leading Adoption

Stablecoin remittance adoption is growing fastest in regions where financial infrastructure gaps are most visible.

Several conditions accelerate adoption:

Currency Instability

In countries facing inflation or currency devaluation, dollar-backed stablecoins provide perceived stability.

Limited Banking Access

Millions of people globally remain underbanked despite having smartphone access.

Digital wallets create alternative financial access points.

Expensive Remittance Corridors

Some remittance routes charge disproportionately high fees.

Stablecoin transfers reduce intermediary costs.

Freelancer and Creator Economies

Remote workers increasingly require borderless payment systems for international earnings.

Stablecoins provide faster settlement compared to conventional banking rails.

The Rise of Wallet-Based Financial Ecosystems

Stablecoin remittance networks are no longer isolated payment tools.

They are becoming part of broader wallet ecosystems that integrate:

- Payments

- Savings

- Merchant acceptance

- Lending

- Payroll

- FX conversion

- Debit card access

This creates a more connected digital financial experience.

For many users, especially younger demographics, mobile wallets may become more important than traditional bank accounts.

The implications are significant.

Financial participation increasingly depends on digital connectivity rather than physical banking infrastructure.

How Fintech Companies Are Building New Payment Rails

Fintech startups are aggressively entering the stablecoin remittance space because blockchain rails reduce operational complexity.

Instead of relying entirely on legacy correspondent banking systems, companies can leverage:

- Blockchain settlement layers

- API-based infrastructure

- Digital compliance systems

- Automated treasury management

- Smart routing mechanisms

This allows faster product innovation.

Some firms now offer:

- Near-instant international payroll

- Stablecoin merchant settlements

- Multi-currency wallet services

- Cross-border B2B payments

- Global contractor payouts

These capabilities are reshaping expectations around international money movement.

Compliance Is Becoming the Competitive Advantage

Despite rapid innovation, compliance remains central to sustainable growth.

Stablecoin remittance providers must navigate:

- AML regulations

- KYC requirements

- Sanctions screening

- Licensing frameworks

- Data protection rules

- Transaction monitoring obligations

Regulators worldwide are increasing scrutiny on digital asset payment systems.

As a result, successful remittance networks increasingly invest in:

- Automated compliance infrastructure

- Real-time monitoring

- Blockchain analytics

- Identity verification systems

- Risk scoring engines

The industry is shifting from a “move fast” mindset toward institutional-grade infrastructure.

Trust is becoming as important as speed.

Challenges That Still Need Solving

While stablecoin remittance networks offer clear advantages, several obstacles remain.

Regulatory Uncertainty

Global regulations differ significantly across jurisdictions.

Some countries encourage innovation while others impose restrictions on digital assets.

Off-Ramp Limitations

Users still need efficient local currency conversion channels.

Weak banking integration can reduce usability.

User Education

Many consumers remain unfamiliar with wallet security, blockchain transactions, and digital asset risks.

Network Fragmentation

Different blockchain ecosystems can create interoperability challenges.

Reserve Transparency

Trust depends heavily on the quality and transparency of stablecoin reserves.

These issues will likely shape the next phase of industry development.

The Role of Governments and Central Banks

Governments are paying close attention to stablecoin payment growth because cross-border finance affects monetary policy, taxation, and financial stability.

Some policymakers view stablecoins as:

- Innovation opportunities

- Financial inclusion tools

- Competitive payment infrastructure

Others worry about:

- Capital flight

- Currency substitution

- Consumer protection

- Systemic risk

Central Bank Digital Currencies (CBDCs) are also entering the conversation.

In the future, hybrid systems may emerge where:

- Stablecoins

- CBDCs

- Traditional banking rails

- Fintech wallets

operate together within interoperable payment ecosystems.

The long-term landscape is still evolving.

Why Businesses Are Watching Closely

Stablecoin remittance infrastructure is not just for consumers.

Businesses increasingly recognize potential operational advantages.

Key use cases include:

Cross-Border Payroll

Global teams can receive payments faster with reduced settlement delays.

Supplier Payments

International vendors can access quicker settlements with lower transfer costs.

Treasury Management

Firms operating across multiple countries may optimize liquidity movement.

Marketplace Payouts

Platforms serving freelancers and creators benefit from faster global disbursements.

As stablecoin infrastructure matures, enterprise adoption may accelerate significantly.

The Human Side of Faster Remittances

Technology discussions often focus on infrastructure, compliance, and market growth.

But remittances are ultimately personal.

For millions of families, international money transfers pay for:

- Education

- Rent

- Healthcare

- Food

- Emergency expenses

Reducing transfer fees by even a small percentage can have a meaningful economic impact at the household level.

Faster settlement also matters during crises, natural disasters, or urgent medical situations where waiting several days for funds creates real hardship.

This human dimension explains why stablecoin remittance adoption continues gaining momentum despite regulatory complexity.

The Future of Stablecoin Remittance Networks

The next few years will likely determine whether stablecoin remittances remain a fintech niche or become a foundational layer of global finance.

Several trends suggest continued momentum:

- Expansion of regulated stablecoins

- Institutional blockchain adoption

- Improved wallet usability

- Growth of compliant digital banking platforms

- Enhanced interoperability

- Increased fintech partnerships

- Greater merchant acceptance

At the same time, regulation will shape market structure.

The companies most likely to succeed may not be the fastest-moving startups alone, but the platforms capable of combining:

- Compliance

- Scalability

- Security

- User trust

- Global accessibility

Stablecoin remittance networks are no longer experimental technology projects.

They are becoming real financial infrastructure.

And for a world demanding faster, cheaper, and more inclusive cross-border payments, that infrastructure may arrive sooner than many expected.