Optimizing Debt Recovery: How Behavioral Segmentation Cut Collection Costs

Shreya Rai5 min read·Just now

Shreya Rai5 min read·Just now--

Lessons from turning a chaotic collections system into a decision engine.

Why Collections Efficiency Matters More Than It Seems

During my stint at Uni Cards, I saw our collections team doing everything right. More calls, faster follow-ups, tighter processes. Yet, costs kept rising, and the impact wasn’t improving proportionally. Something didn’t add up. This forced us to step back and rethink how we approached collections.

In any fintech, collections is one of the most critical yet least visible parts of the business. It sits at the intersection of revenue protection, risk management, and customer operations. At a basic level, collections efficiency refers to how effectively a company is able to recover overdue payments while minimizing the cost and effort involved. This includes not just recovery rates, but also metrics like cost per recovery, agent productivity, and the time taken to bring an account back to good standing.

At small scale, inefficiencies in collections are often absorbed into the system. A few extra calls, slightly delayed recoveries, or redundant efforts don’t immediately show up as major problems. But as the user base grows, these inefficiencies begin to compound. What was once a manageable operational overhead can quickly turn into a significant cost center, requiring more agents, more infrastructure, and more coordination just to maintain the same level of performance.

Collections is also not just a backend function, it directly interacts with users. The way a company approaches recovery, the timing of its interventions, and the intensity of its actions all contribute to how users perceive the company. In that sense, collections is not only about recovering money, it is also about managing ongoing relationships with users during sensitive moments.

Discovering the Pattern in Repayments

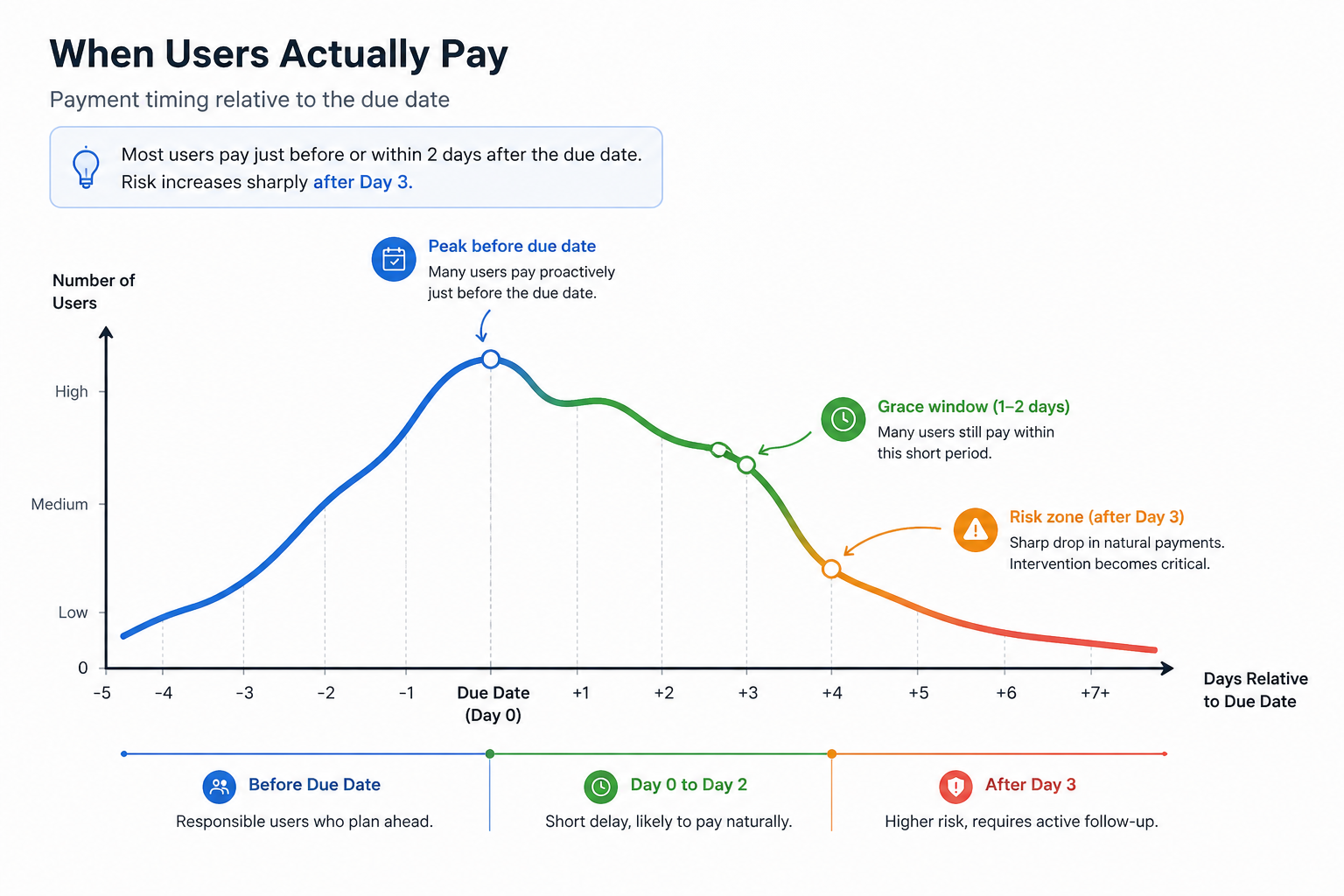

We wanted to optimize the collections process and reduce the costs associated with it. For this, we went back to the data. We started by looking at the timeline of repayments, specifically, when users actually chose to pay relative to their due date. Instead of focusing only on whether a user eventually paid or not, we tried to understand how long it typically took them to clear their dues.

What emerged was a pattern that wasn’t immediately obvious at an aggregate level. A large portion of users were making payments one to two days before the due date, or within the first one to two days after it. Beyond Day 3, however, the curve changed significantly, repayment rates began to decline sharply, and the behavior of users started to look very different.

To validate whether this pattern was meaningful, we layered in call activity data. This helped us understand not just when users were paying, but whether those payments were actually influenced by collections efforts. What we found was revealing. Many users in this early window were completing their payments without ever speaking to an agent. In some cases, repayment happened even before a successful call connection was established.

This shifted our understanding of delinquency. Instead of viewing all late users as a single group, it became clear that there were fundamentally different behaviors at play.

From “Who Owes” to “Who Needs Intervention”

We reframed the problem. Instead of asking who owed money, we asked how to distinguish between “forgetful” users and “risky” ones. This led us to shift from static snapshots to behavioral trajectories. We analyzed six months of user data, focusing on repayment history, credit score, credit velocity, etc. One insight stood out clearly: a sudden spike in credit utilization was a stronger predictor of near-term delinquency than credit score. A high-score user who had recently ramped up borrowing aggressively was often riskier in the short term than a lower-score user with stable behavior. This marked a shift from evaluating who the user is to understanding what the user is doing right now.

Turning Insights Into a Decision System

But insight alone doesn’t change operations. We needed a way to translate this into something actionable. We anchored our approach on a simple metric: how many days after the due date does a user typically repay? This became the lens through which we evaluated all signals. Using SPSS Modeler, we built a decision tree to segment users, prioritizing clarity and business usability. We removed weak predictors, focused on high-signal variables to simplify the logic so that it could be easily understood and trusted by the business. The strongest predictors were income category, recent credit velocity (credit lines taken in the last three months), and changes in utilization.

We finally arrived at three segments that broadly classified users into distinct behavioral categories based on their likelihood and urgency of repayment.

1 : Self-Serve (~45%): Users with stable financial behavior, consistent repayment history, and no recent signs of stress.

2 : Prompted (~40%): Users showing some deviations, such as slight delays or changes in utilization, but still somewhat reliable.

3 : Priority (~15%): Users with persistent delinquency patterns, low engagement, and a history of not responding to outreach.

For the Self-Serve group, we introduced a 48-hour silence window, relying only on automated nudges and allowing users to repay within their natural timeline. The most counterintuitive part of this strategy was the silence window. To validate it, we ran a Champion–Challenger test with around 500 users initially, comparing a 24-hour intervention strategy against a 48-hour silence window. We measured recovery rate, cost per recovery, and cost per tier. The results were clear: even without calling, recovery rates remained almost identical within the 48-hour window.

The Prompted group received light-touch intervention, starting with digital reminders on the first day and immediate and proactive agents began outreach from Day 2, focusing their effort where early intervention could prevent deeper delinquency. Finally, for AWOL or chronic users, traditional call-based approaches were often ineffective, so we bypassed them entirely and escalated directly to field interventions.

To operationalize this framework, we integrated it into existing workflows by classifying users as paid or unpaid each morning and applying segmentation alongside it. Agents accessed these segments through dashboards, with updates reflected in the CRM. We chose not to dynamically change segments after initial classification to avoid operational confusion and any unpaid users after day 4 were considered with high urgency.

Final Thoughts

This approach led to a 25% reduction in monthly collection costs, driven by a significant drop in unnecessary calls and better allocation of agent effort. Operational efficiency improved as teams focused their attention on users who truly required intervention. High-risk accounts received more timely and targeted follow-ups, improving recovery outcomes where it mattered most. At the same time, the overall customer experience became smoother and less intrusive for users who were likely to repay on their own.