Mapping the Chaos: A Risk Register for a Nepali FinTech Startup

--

GRC exercise using a hypothetical startup called NamastePay-Plus

I’m currently learning cybersecurity, and one of the first things my course touched on was Governance, Risk & Compliance or GRC. Honestly, when I first heard “risk register,” it sounded like something only banks with huge compliance departments would care about.

Then I started thinking about the Nepali context. We have digital payment apps growing fast, NRB tightening its Cyber Resilience Guidelines in 2026, and yet a lot of small FinTechs are probably running without a formal risk document. So I decided to try building one myself for a hypothetical startup I’m calling NamastePay-Plus.

This is my first attempt. It’s not perfect. But I learned a lot building it, and I want to share it with anyone else who’s starting out.

The Methodology: Likelihood × Impact

I used the simplest risk scoring method there is:

Risk Score = Likelihood (1–5) × Impact (1–5)

Score Range Level 1–5 🟢 Low 6–12 🟡 Medium 13–19 🟠 High 20–25 🔴 Critical

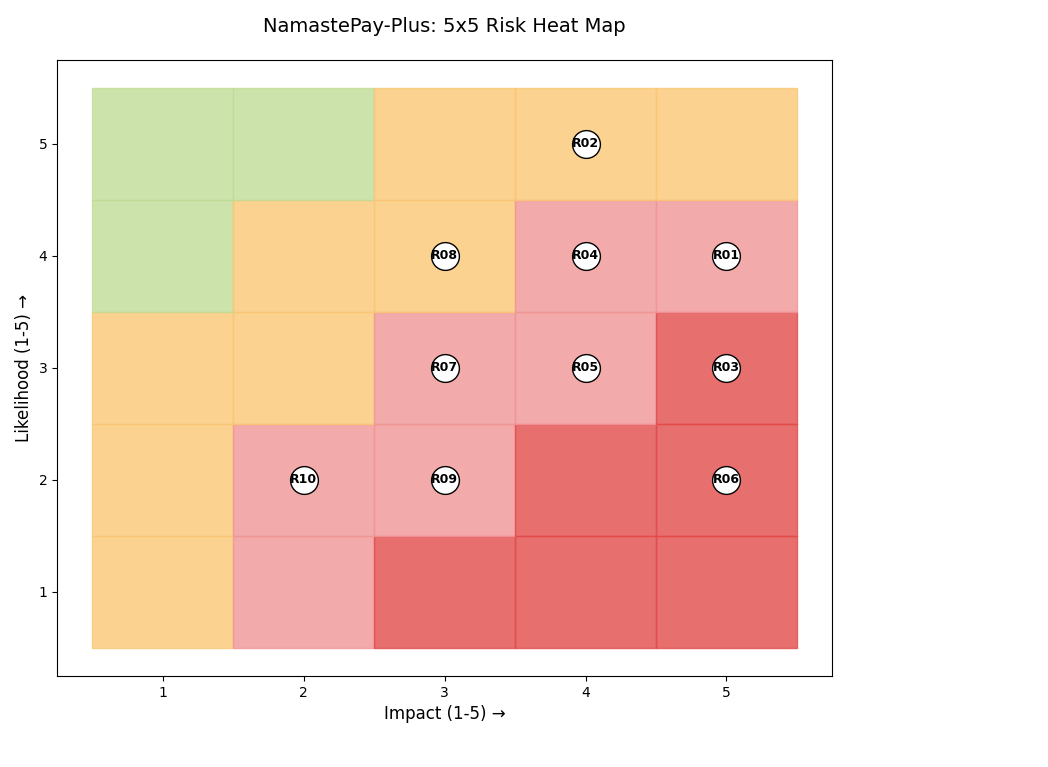

I also plotted everything on a 5×5 Heat Map. The honest truth is I struggled with some of the scores. How do you decide if something is a 3 or a 4 on likelihood? I realized you have to think about your specific context, not just copy scores from a textbook.

The 5×5 Heat Map

- 🔴 Critical (20–25): R01 (4,5=20), R02 (5,4=20)

- 🟠 High (13–19): R03 (3,5=15), R04 (4,4=16)

- 🟡 Medium (6–12): R05, R06, R07, R08, R09

- 🟢 Low (1–5): R10

The Full Risk Register

R01. Single ISP Dependency (Internet Downtime)

Score: 4 × 5 = 20 Critical Heat Map Position: (L=4, I=5) >Danger Zone

Category: Availability Risk Owner: IT / Network Team NRB Reference: Section 4.2 : Business Continuity

NamastePay-Plus relies on one ISP for all payment traffic. When that ISP goes down (and in Nepal, this happens), transactions fail completely. I realized this is actually more dangerous than it sounds for a payment app even one hour of downtime destroys customer trust.

Treatment: Negotiate a secondary ISP contract (e.g., WorldLink + CG Net failover). Implement BGP load-balancing. NRB guidelines also require a Business Continuity Plan that addresses this directly.

R02. Viber / WhatsApp Phishing Targeting Customers

Score: 5 × 4 = 20 Critical Heat Map Position: (L=5, I=4)>Danger Zone

Category: Social Engineering Risk Owner: Customer Support + Marketing NRB Reference: Section 6.1: User Awareness

When looking at the local context, almost every Nepali uses Viber or WhatsApp. Attackers are already sending fake ‘NamastePay-Plus’ messages to trick customers into handing over OTPs. As a student, I think this is the most underestimated risk on the list.

Treatment: In-app fraud warnings, Viber Blue Tick verification, customer SMS alerts for every transaction. Run a short Nepali-language awareness campaign on social media.

R03. NRB 2026 Reporting Non-Compliance

Score: 3 × 5 = 15 High Heat Map Position: (L=3, I=5)

Category: Compliance / Regulatory Risk Owner: GRC / Compliance Team NRB Reference: Section 7 :Incident Reporting 2026

NRB’s 2026 cyber-resilience standards introduced stricter incident reporting windows (under 6 hours for critical events). NamastePay-Plus does not currently have an automated incident logging pipeline. A missed report = regulatory fine + possible license suspension.

Treatment: Deploy a SIEM tool (even a lightweight open-source one like Wazuh). Create an Incident Response Playbook with clear escalation paths. Assign a dedicated compliance officer.

R04. Insider Threat from Under-Trained Staff

Score: 4 × 4 = 16 : High Heat Map Position: (L=4, I=4)

Category: Human Factor Risk Owner: HR + IT Security

NRB Reference: Section 5.3 : Human Resource Security

Staff who don’t understand phishing, password hygiene, or data handling are a major risk vector. I noticed that many small Nepali startups skip security onboarding entirely — people just get handed a laptop and a login. That’s a recipe for accidental (or even intentional) data leaks.

Treatment: Mandatory quarterly security awareness training. Enforce least-privilege access control. Monitor privileged account activity with audit logs.

R05 . Weak API Authentication on Mobile App

Score: 3 × 4 = 12 : Medium Heat Map Position: (L=3, I=4)

Category: Application Security Risk Owner: Dev Team NRB Reference: Section 3.1 : Access Control

The NamastePay-Plus mobile API currently uses basic tokens with no rate limiting. This means brute-force or credential stuffing attacks could work. When looking at the local context, many Nepali users reuse passwords from other apps.

Treatment: Implement OAuth 2.0, add rate-limiting and CAPTCHA on login, enforce multi-factor authentication for all transactions above NPR 10,000.

R06. Unencrypted Customer PII in Database

Score: 2 × 5 = 10: Medium Heat Map Position: (L=2, I=5)

Category: Data Protection Risk Owner: Dev Team + DBA NRB Reference: Section 3.4 : Data Protection

A code audit revealed that some customer PII fields (name, phone, partial card data) are stored in plaintext. If there’s ever a breach, this data is immediately exposed. This one surprised me — it’s a basic fix that just hasn’t been prioritized yet.

Treatment: Encrypt all PII fields using AES-256 at rest. Implement database access logging. Conduct a full data-flow audit quarterly.

R07. No Formal Vendor / Third-Party Risk Assessment

Score: 3 × 3 = 9 : Medium Heat Map Position: (L=3, I=3)

Category: Third-Party Risk Risk Owner: Procurement + IT Security NRB Reference: Section 8 :Third-Party Management

NamastePay-Plus uses third-party SDKs for KYC, payment gateway, and SMS OTP. None of these vendors have been formally assessed for security posture. A compromise in any one of them propagates directly into the app.

Treatment: Create a vendor risk assessment checklist. Require security certifications (ISO 27001, PCI-DSS) from critical vendors before renewing contracts.

R08. Load-Shedding Disrupting Server Uptime

Score: 4 × 3 = 12 Medium Heat Map Position: (L=4, I=3)

Category: Physical / Environmental Risk Owner: IT / Infrastructure NRB Reference: Section 4.1 : Physical Security

Load shedding is still a real issue in many parts of Nepal. If the on-premise components of the infrastructure aren’t on proper UPS/generator backup, even a short power cut could cause transaction failures or data corruption during writes.

Treatment: Move critical workloads to cloud (AWS Mumbai region or Azure). For any on-prem components, ensure UPS + diesel generator with at least 8-hour capacity.

R09 . Insufficient Logging and Monitoring

Score: 2 × 3 = 6 Medium Heat Map Position: (L=2, I=3)

Category: Detection & Response Risk Owner: IT Security NRB Reference: Section 7.1 :Monitoring & Logging

As a student, I think this is often invisible until something goes wrong. Without proper logs, NamastePay-Plus wouldn’t even know if they were being attacked. Right now there’s no centralized log management each service logs locally.

Treatment: Implement centralized logging (ELK stack or Wazuh). Set up alerting thresholds. Assign someone to review security logs weekly (can be part-time initially).

R10 . Weak Password Policy for Staff Accounts

Score: 2 × 2 = 4 Low Heat Map Position: (L=2, I=2)

Category: Identity & Access Risk Owner: IT Admin NRB Reference: Section 3.1 : Access Control

Staff accounts allow short, simple passwords with no mandatory rotation. This is a low-hanging fruit fix but it still counts as a real risk, especially for admin accounts with elevated privileges.

Treatment: Enforce minimum 12-character passwords, complexity requirements, and 90-day rotation. Deploy a password manager (Bitwarden Teams is free for small teams).

Summary Table

What I Learned Building This

A few honest reflections:

Scoring is subjective and that’s okay. I went back and changed several scores multiple times. The point of the exercise isn’t to get a “correct” number; it’s to force you to think about each risk in context.

Local context changes everything. A generic risk register template wouldn’t include Viber phishing or load-shedding. When I adapted it to Nepal, the register became actually useful.

The heat map makes priorities obvious. Seeing R01 and R02 sitting in the red zone at (4,5) and (5,4) made it immediately clear where NamastePay-Plus should focus first. You can’t argue with a visual like that.

Compliance isn’t separate from security. R03 (NRB non-compliance) taught me that regulatory risk is just another row in the same table as technical risks. GRC really does mean all three things together.

This is a student exercise based on publicly available NRB Cyber Resilience Guidelines. NamastePay-Plus is entirely hypothetical. I’d love feedback from anyone working in FinTech security or GRC in Nepal what did I miss?

#cybersecurity #GRC #Nepal #FinTech #NRB #riskmanagement #learnInPublic