Cash & Carry: The Market’s Most Honest Trade

StochyAI6 min read·Just now

StochyAI6 min read·Just now--

A practical guide to capturing basis yield in crypto derivatives

Remember the good old days? When cash and carry yields hit 30–50% annualized? I do. You’d sell futures, buy spot, collect the spread, and go to sleep. Life was good. Volatility was higher, basis was fat, and retail was still figuring out arbitrage.

Now? We’re sitting at ~3% on the best contracts. That’s still a risk-free return in a world of subdued rates, but the days of easy money are long gone. Markets mature, spreads compress, and the cycle continues. But who knows — maybe one day we’ll see those glorious 30%+ yields again. Just gotta keep tracking it.

What is cash and carry?

Cash and carry (often called “basis trading” or “spot-futures arbitrage”) is the closest thing crypto has to a risk-free trade. Here’s the idea:

You simultaneously:

- Sell futures contracts at a premium (forward price)

- Buy the spot asset at a lower price

- Hold both until futures expiry

- Pocket the spread minus costs

The market “pays you” that spread because futures are trading higher than spot. That’s contango — and it’s your edge.

Why does the spread exist?

Futures are forward contracts. If everyone expects prices to rise, they’ll pay a premium to lock in today’s price. That premium encodes:

Carry cost: Funding your spot position (borrowing/opportunity cost)

Insurance premium: Buyers want upside protection

Illiquidity: Spot buyers vs. futures buyers are different cohorts

Demand imbalance: Too many long positions chasing contracts

The spread between futures and spot is the

basis. That basis, annualized, is your yield.

What a real trade looks like

Setup (using Deribit as example):

Step 1: Buy spot (and borrow it if needed)

You need the actual asset. Buy 1 BTC on Kraken, Coinbase, wherever the price is decent. If you’re already holding, great — no extra cost. If you have to borrow, factor in the lending rate (typically 1–5% annually, depending on supply/demand).

Step 2: Sell futures on Deribit (or wherever)

Short the same amount on Deribit’s quarterly or perpetual. For a clean arbitrage, use the quarterly (26MAR27, 25SEP26, 25DEC26) so you know your exact exit date. Your futures short is your hedge.

Step 3: Manage the position

Mark-to-market daily. Your P&L doesn’t move (that’s the point), but margin requirements fluctuate. Set aside extra collateral to avoid liquidation ruin if BTC tanks 20%. It won’t affect your arbitrage profit, but it will force you out at the worst time.

Step 4: At expiry, deliver or unwind

When futures expire, they settle to the spot index. Your long spot and short futures converge. Close both (or let futures settle), pocket your basis yield minus fees. Done.

The costs that kill your edge

That 3.51% yield looks beautiful until you account for friction. Let’s break it down:

1. Bid-ask spread (futures)

On 26MAR27 BTC, the spread might be $2–5 depending on volume. You’re selling into the bid when you short, so you lose that immediately. Example: you wanted to sell at $68,722, but the best bid is $68,720. You just lost $2 per contract, or 0.003% on entry alone.

2. Bid-ask spread (spot)

Buying 1 BTC on a major exchange might cost you $10–50 in spread if you’re not patient. Use limit orders, or buy on the cheapest exchange and transfer. But transfer fees add up too.

3. Exchange fees

Deribit charges 0.05% maker / 0.05% taker. On a $68k position, that’s ~$34 per side, or $68 round-trip. Your broker might take 0.1–0.2% on spot. That’s another $68–136. Total: ~$140 in fees. Your gross yield was 3.51% on $68k = ~$2,387. Fees eat ~6% of that.

4. Borrowing cost (if you short-sold spot)

Some strategies borrow spot to sell it, buying futures instead (reverse carry). Don’t do that in contango — you’re paying to fund the wrong side. Stick to owning spot.

5. Funding rate (if using perps instead of quarterly)

Perpetual futures have 8-hour funding rates. If longs are paying shorts, you earn it; if shorts are paying, you bleed. Over 363 days, a 0.03% daily rate eats 11% of your return. Avoid perpetuals for long-dated carry.

6. Slippage on the unwind

At expiry, you’re closing both legs. If you’re a big position, you move the market. Small positions? Probably fine. Large ones? Budget another 0.1–0.3% slippage.

7. Custody/wallet risk

If you’re holding spot in a self-custodied wallet, you pay transfer fees (2–10 USD per move). If on an exchange, you have counterparty risk. If lending, you have yield-farm risk (no FDIC here). Pick your poison.

When to enter (and exit)

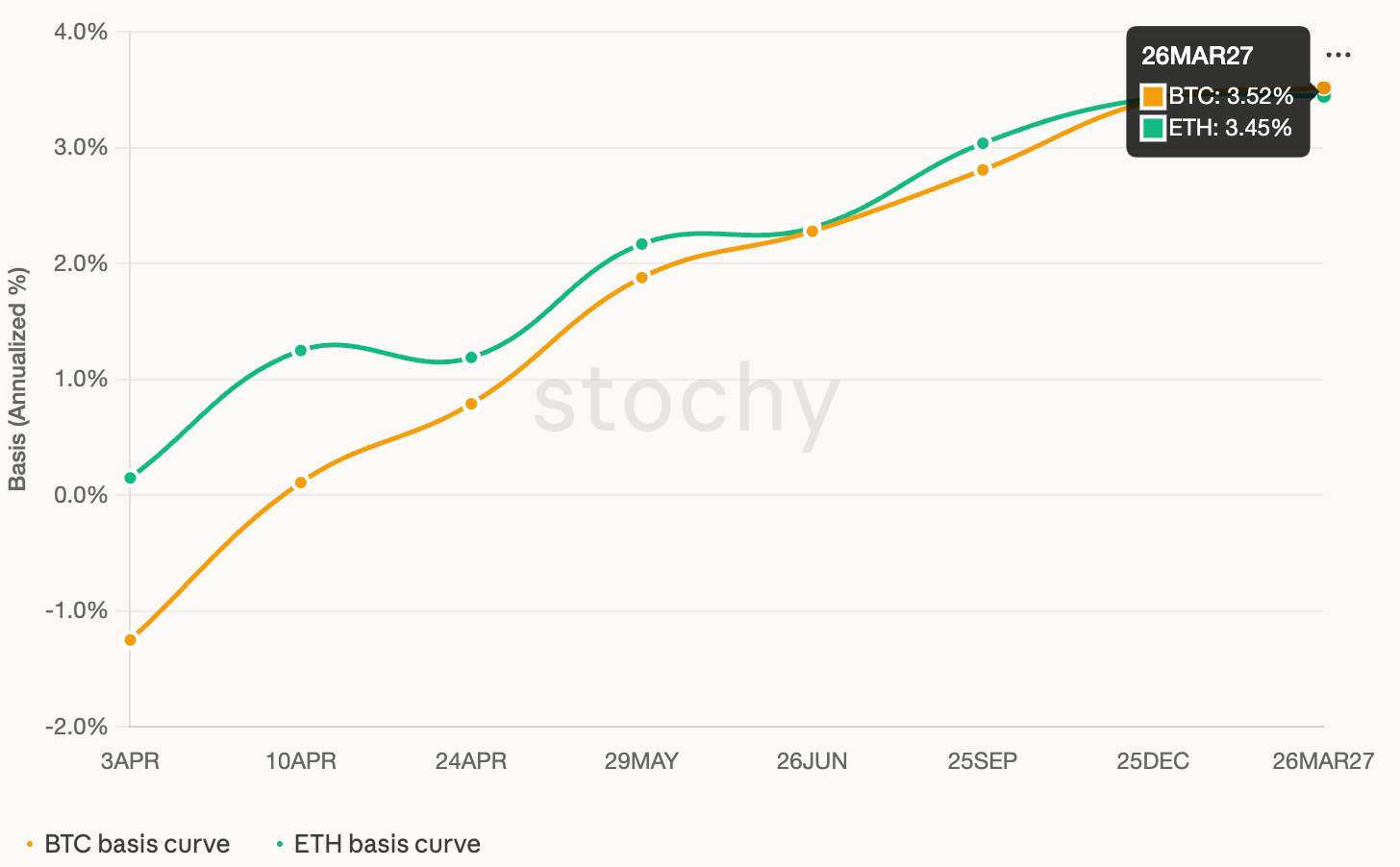

Entry signal: The basis is fat

Look at the annualized basis (shown in the table as BASIS ANN.). For March 26, BTC is at 3.51% — decent, but not crushing. You’d want to see at least 2–3% after subtracting expected fees. Anything under 2% is probably not worth the operational headache for retail.

Pro tip: Check the curve. If March is 3.51% but June is 2.26%, consider rolling. You get paid to extend, but the curve tells you when the market stops caring about carry.

Risk management: Liquidation buffer

If BTC drops 30%, your spot is down $20k but your futures are hedged (unrealized gain of ~$20k). Your P&L is stable. But if you’re on 2x leverage to juice returns, a 50% drop liquids you. Don’t do this.

Rule: Keep at least 3–4x more collateral than required. Deribit liquidations are messy.

Exit signal: Basis compresses to nothing

If the spread tightens to 0.2% annualized, close it out. Your edge disappeared. Move to the next contract or take a break.

Why this still matters at 3%

Sure, 3% isn’t 30%. But compare it to what you’d earn elsewhere:

- US Treasuries: ~4.5% (but taxable, duration risk)

- Stablecoins on Lido: ~3–4% (smart contract risk)

- Equity dividends: ~2% (market risk, volatility)

Cash and carry is the only one that’s truly insulated from directional risk. Your P&L is determined on day one. You’re not betting on price; you’re collecting a spread. That’s rare.

The practical checklist

Before you pull the trigger:

- ✓ Annualized basis > 2.5% (or 3.5% if you have high fees)

- ✓ Spot liquidity on at least 2 exchanges (so you can exit)

- ✓ Futures volume > $100M daily (so spreads are tight)

- ✓ Collateral buffer = 3–4x minimum requirement

- ✓ No leverage on the spot side

- ✓ Time horizon matches the futures expiry (don’t fight the curve)

- ✓ Fees + slippage < 0.5% of the gross yield

The cyclical game

Basis trading is a Darwinian game. High yields attract capital. Capital narrows spreads. Spreads compress basis. Yields fall. Capital leaves. Spreads widen. Yields rise. Repeat.

The 30–50% days will come again — probably during the next bull peak when retail FOMO drives funding rates through the roof. For now, 3% is solid. It’s honest. It’s repeatable. And it doesn’t require you to predict markets.

⚠️ Disclaimer: This is educational content, not financial advice. Crypto is volatile, exchanges can go down, smart contracts can have bugs, and your assumptions about borrowing costs / transfer fees / slippage might be completely wrong by the time you read this. Past basis yields are not indicative of future basis yields. You could lose money. Your favorite exchange could get hacked. Deribit could add new fees tomorrow. The tax code might change. Do your own research, stress-test your assumptions, and never bet more than you can afford to lose. This is especially true for leveraged or complex positions. The author of this article is not a financial advisor, is not your fiduciary, and is not responsible for your trading losses. Trade at your own risk. 🎯