Black-Scholes Option Pricing, Black-Scholes Model, Options Greeks explained with Python

🧠 Why Black-Scholes Option Pricing matters

If you trade options, you are not just trading direction.

You are trading:

- Probability

- Time

- Uncertainty

The Black-Scholes model converts all of this into:

Price + Greeks → actual P&L behavior

🎯 What you will build

From your notebook:

- Real data using yfinance

- A contract → model → output pipeline

- Visual understanding of:

- Delta

- Gamma

- Theta

- And finally: P&L intuition

🧠 Step 1: Black-Scholes Engine

import numpy as np

from scipy.stats import norm

def black_scholes_call(S, K, T, r, sigma):

d1 = (np.log(S / K) + (r + 0.5 * sigma**2) * T) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

call_price = S * norm.cdf(d1) - K * np.exp(-r * T) * norm.cdf(d2)

delta = norm.cdf(d1)

gamma = norm.pdf(d1) / (S * sigma * np.sqrt(T))

theta = (-S * norm.pdf(d1) * sigma / (2 * np.sqrt(T))

- r * K * np.exp(-r * T) * norm.cdf(d2)) / 365

vega = (S * norm.pdf(d1) * np.sqrt(T)) / 100

return {

"price": call_price,

"delta": delta,

"gamma": gamma,

"theta": theta,

"vega": vega

}

Step 2: Get Market Data

import yfinance as yf

ticker = yf.Ticker("AAPL")

spot = ticker.history(period="1d")["Close"].iloc[-1]

expiry = ticker.options[0]

calls = ticker.option_chain(expiry).calls

👉 This gives you the real option chain

🧠 Step 3: Parse Contracts

def parse_contract_symbol(symbol):

underlying = symbol[:-15]

expiry_str = symbol[-15:-9]

option_type = symbol[-9]

strike_str = symbol[-8:]

expiry = pd.to_datetime(expiry_str, format="%y%m%d")

strike = int(strike_str) / 1000

return pd.Series([underlying, expiry, option_type, strike])

Step 4: Build Selection Layer (df1)

Contracts = calls[[

'underlying',

'parsed_strike',

'expiry',

'option_type',

'contract_size',

'lastPrice',

'impliedVolatility',

'inTheMoney'

]].rename(columns={

'parsed_strike': 'strike',

'lastPrice': 'market_price'

})

👉 This is your decision layer (what to trade)

🧠 Step 5: Build Model Inputs (df2)

def build_bs_inputs(row, spot, r=0.05):

delta = row['expiry'] - datetime.now()

T = delta.total_seconds() / (365 * 24 * 60 * 60)

if T <= 0:

T = 1 / 365

sigma = row['impliedVolatility']

if pd.isna(sigma) or sigma < 0.01:

sigma = 0.2

return pd.DataFrame([{

"Spot Price": spot,

"Strike Price": row['strike'],

"Time to Expiry": T,

"Volatility": sigma,

"Interest Rate": r

}])

Step 6: Run Model

res = black_scholes_call(

S=df2["Spot Price"].iloc[0],

K=df2["Strike Price"].iloc[0],

T=df2["Time to Expiry"].iloc[0],

r=df2["Interest Rate"].iloc[0],

sigma=df2["Volatility"].iloc[0]

)

📊 Output Interpretation

From your notebook:

Price ≈ 23.86

Delta = 1.00

Gamma ≈ 0

Theta ≈ -0.032

Vega ≈ 0

🧠 Meaning

- Delta = 1 → behaves like stock

- Gamma ≈ 0 → no convexity

- Vega ≈ 0 → no uncertainty

- Theta small → mostly intrinsic

👉 This is a deep ITM option

📈 Step 7: Delta vs Stock Price

S_range = np.linspace(200, 300, 100)

deltas = [

black_scholes_call(

S,

df2["Strike Price"].iloc[0],

df2["Time to Expiry"].iloc[0],

df2["Interest Rate"].iloc[0],

df2["Volatility"].iloc[0]

)['delta']

for S in S_range

]

plt.plot(S_range, deltas)

Interpretation

- Delta moves 0 → 1

- ATM = steep region

- ITM/OTM = flat

👉 Transition from lottery → convex → stock

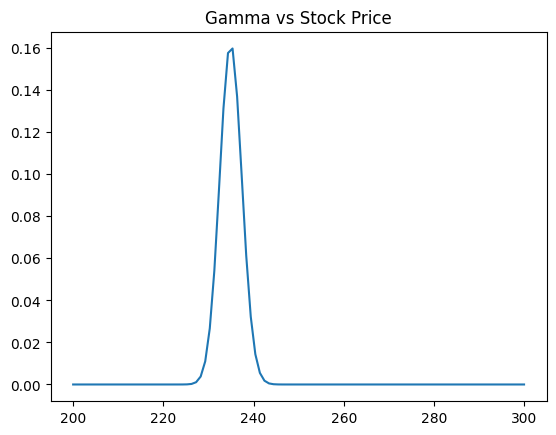

📈 Step 8: Gamma vs Stock Price

gammas = [

black_scholes_call(

S,

df2["Strike Price"].iloc[0],

df2["Time to Expiry"].iloc[0],

df2["Interest Rate"].iloc[0],

df2["Volatility"].iloc[0]

)['gamma']

for S in S_range

]

Interpretation

- Peak at ATM

- Low elsewhere

👉 Maximum convexity happens at the strike

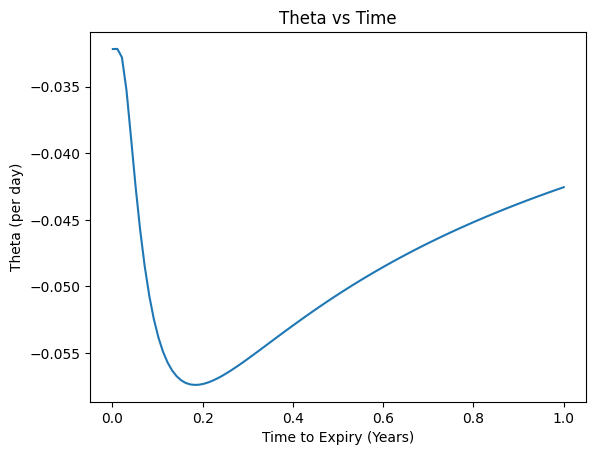

📉 Step 9: Theta vs Time

T_range = np.linspace(0.001, 1, 100)

thetas = [

black_scholes_call(

df2["Spot Price"].iloc[0],

df2["Strike Price"].iloc[0],

T,

df2["Interest Rate"].iloc[0],

df2["Volatility"].iloc[0]

)['theta']

for T in T_range

]

plt.plot(T_range, thetas)

Interpretation

- Theta becomes more negative near expiry

- Decay accelerates

- Longer time = slower decay

👉 Time is not linear

Step 10: Theta vs Time (ATM vs ITM vs OTM)

🟦 ATM (Blue)

- Massive decay near expiry

- Highest uncertainty collapse

- 👉 Most dangerous zone

🟧 ITM (Orange)

- Stable decay

- Mostly intrinsic

- 👉 Stock-like behavior

🟩 OTM (Green)

- Small decay early

- Sudden drop near expiry

- 👉 Lottery behavior

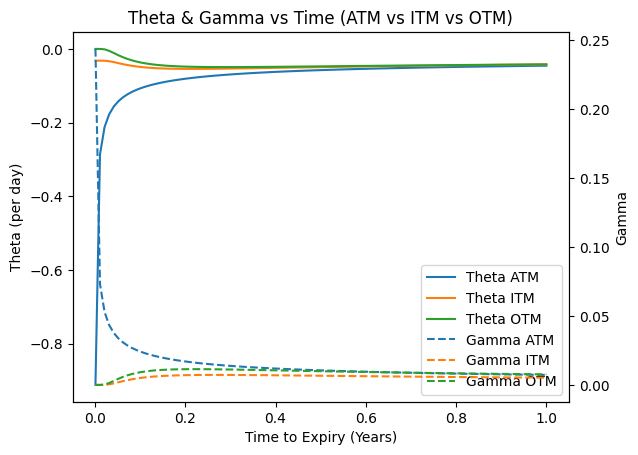

📊 Step 11: Theta + Gamma Overlay (MOST IMPORTANT)

🟦 ATM (Battlefield)

- Gamma spikes

- Theta crashes

👉 Move fast → big gain

👉 No move → fast loss

🟧 ITM (Stable)

- Low gamma

- Mild theta

👉 Linear exposure

🟩 OTM (Lottery)

- Low gamma

- Late theta

👉 Nothing → then collapse

🔥 THE BIG INSIGHT

Gamma (reward) and Theta (cost) peak together

🎯 What charts prove

- ATM = high risk, high reward

- ITM = stable, low convexity

- OTM = low probability, asymmetric

⚠️ Critical trading insight

The most attractive trades (high gamma)

are also the ones bleeding the fastest (high theta)

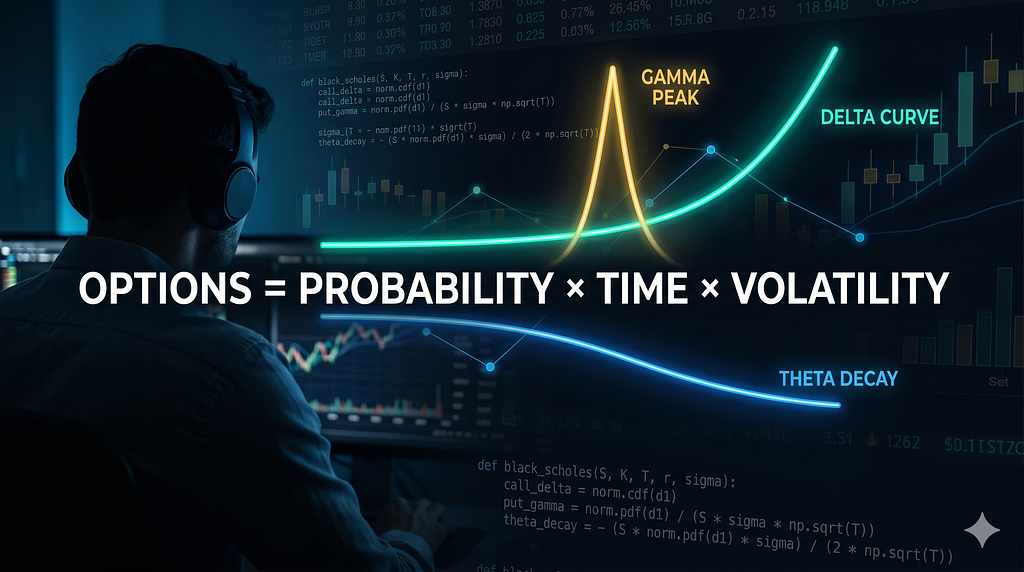

🧠 Final Mental Model

Options = Probability × Time × Volatility

One-line takeaway

You are always paying Theta to own Gamma

Black-Scholes Option Pricing Explained: Black-Scholes Model with Code, Charts & Intuition was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.