Bitcoin mining data shows why institutions may not want a Bitcoin supercycle yet. Discover the hidden signals shaping 2026.

First, let’s examine the official data provided by leading research firms. “Q1 2026 has become the most brutal test for Bitcoin miners since the 2024 halving. As the Bitcoin price dipped below $70,000, the Hash Price collapsed to historic lows of $28–$30 per PH/s/day, while the average cost of production for public companies exceeded $80,000 per BTC. The industry has officially entered a phase of deep cleansing.”

Mining company

1. Bitcoin Price Dynamics

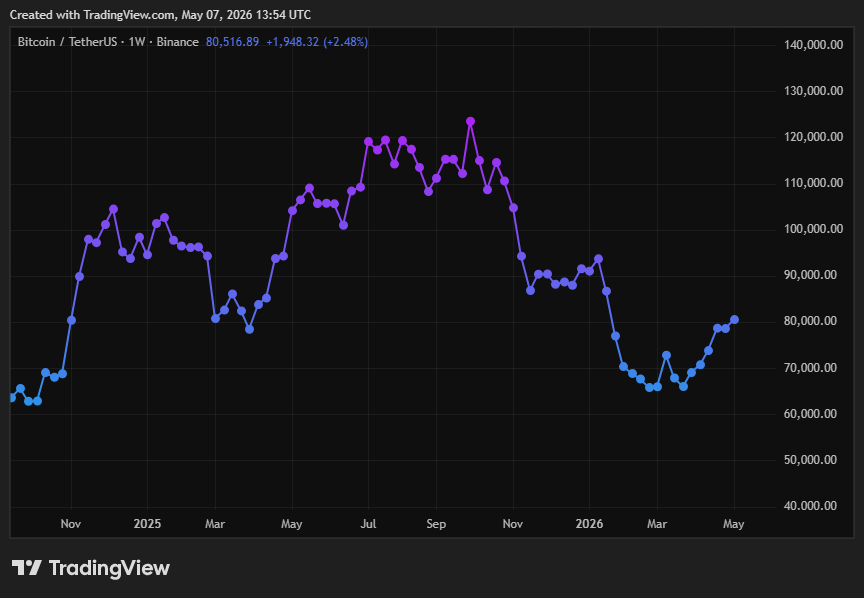

- Q4 2025: This period marked the most challenging timeframe for miners post-2024 halving. The BTC price fell from an all-time high of approximately $124,500 (early October) to roughly $86,000 (late December) — a 31% correction.

- Q1 2026: Price pressure persisted, with Bitcoin touching the $62,000 mark at the start of the year.

2. Mining Economics: A Critical State

The Hash Price (revenue per unit of computing power) has plummeted to unprecedented lows:

- July 2025: ~$63/PH/s/day.

- November 2025: ~$35–37 (a 5-year low).

- March 2026: A new record low of $28–30/PH/s/day.

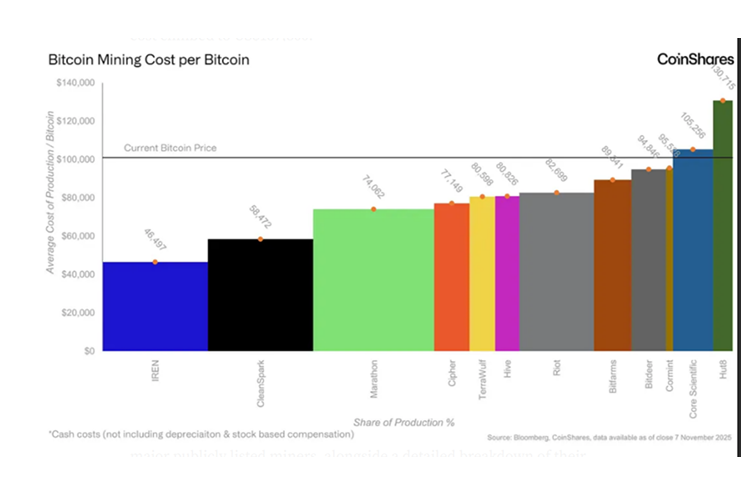

Production Costs Q4 2025:

The average Cash Cost for public miners rose to $79,995 per BTC in Q4 2025.

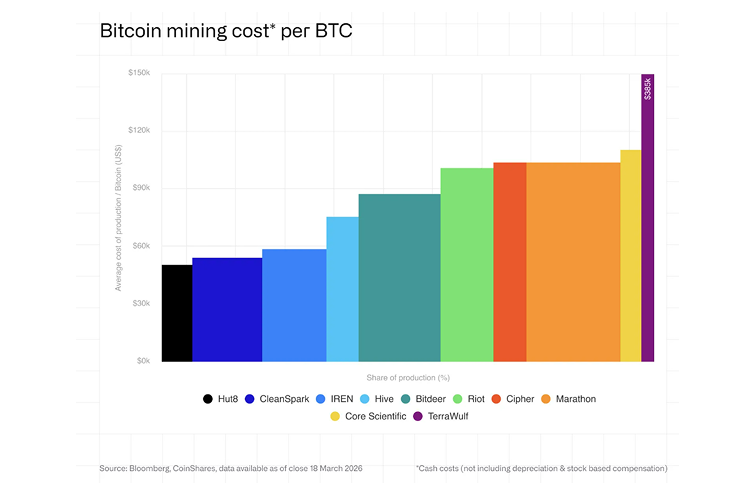

Production Costs Q1 2026:

The average Cash Cost for public miners rose to $100,000 per BTC by Q1 2026.

The All-in Cost is significantly higher due to depreciation and debt servicing. For instance, MARA reported costs of $153,040 ($240,407 without tax incentives), while CleanSpark stood at $118,932.

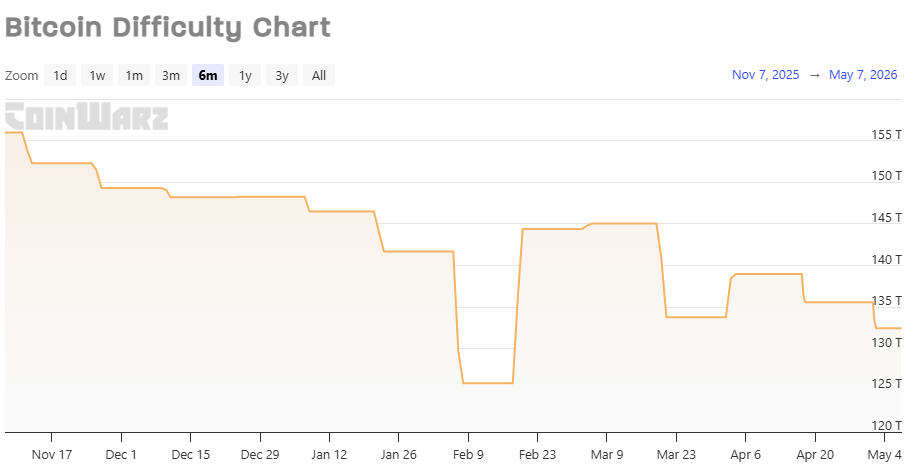

3. Network Metrics (Hashrate and Difficulty)

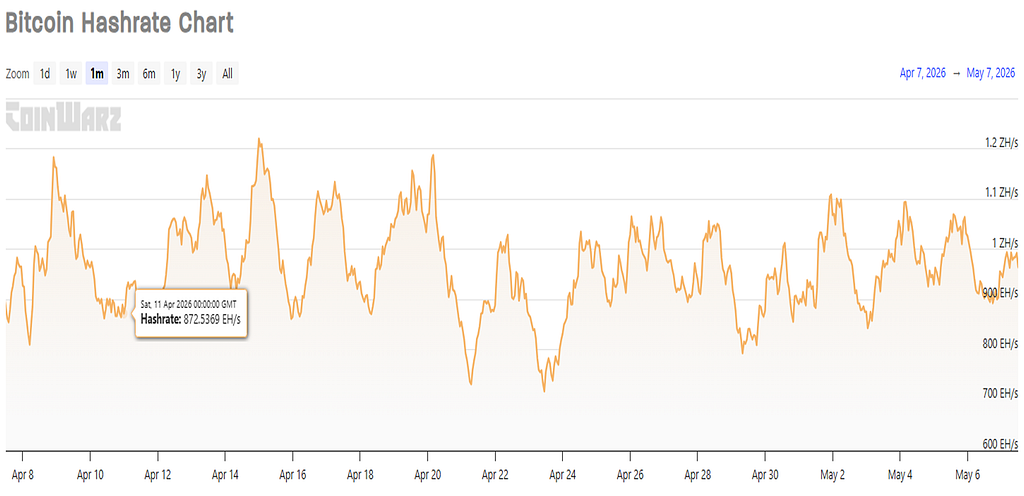

- The 2025 Records: In August 2025, the network exceeded a capacity of 1 Zettahash/s (ZH/s) for the first time, peaking at 1,200 EH/s in Octobery.

- The 2026 Correction: Due to the price drop, the hashrate declined to ~1,045 EH/s in December and bottomed out at 750 EH/s in February 2026.

This triggered three consecutive negative difficulty adjustments for the first time since July 2022.

As of March 31, 2026:

- Miner Revenue: The 7-day average revenue is $32.32 million — a 17.3% decrease over the last 90 days and an 18.5% year-over-year drop.

- Treasury Performance: For public companies holding BTC, the profit ratio turned negative, shifting from +0.09 to -0.16 during the quarter, signaling a move from unrealized gains to losses.

Insight: This is a classic end-of-cycle pattern. Innovative companies with efficient, new-generation hardware remain operational, while those with legacy equipment are forced offline. However, we are not seeing a “classic” miner capitulation (a steady, terminal decline in hashrate). Instead, we see a balancing range between 850–1,100 EH/s. This suggests that major players have reached a new level of resource management — utilizing AI tools for optimization, dynamic power scaling, and better price adaptation. The network difficulty remained in a tight corridor of 132–135T throughout Q1, indicating that a specific group of miners is “throttling” the hashrate to create a safety buffer and maintain operational space during low-price periods.

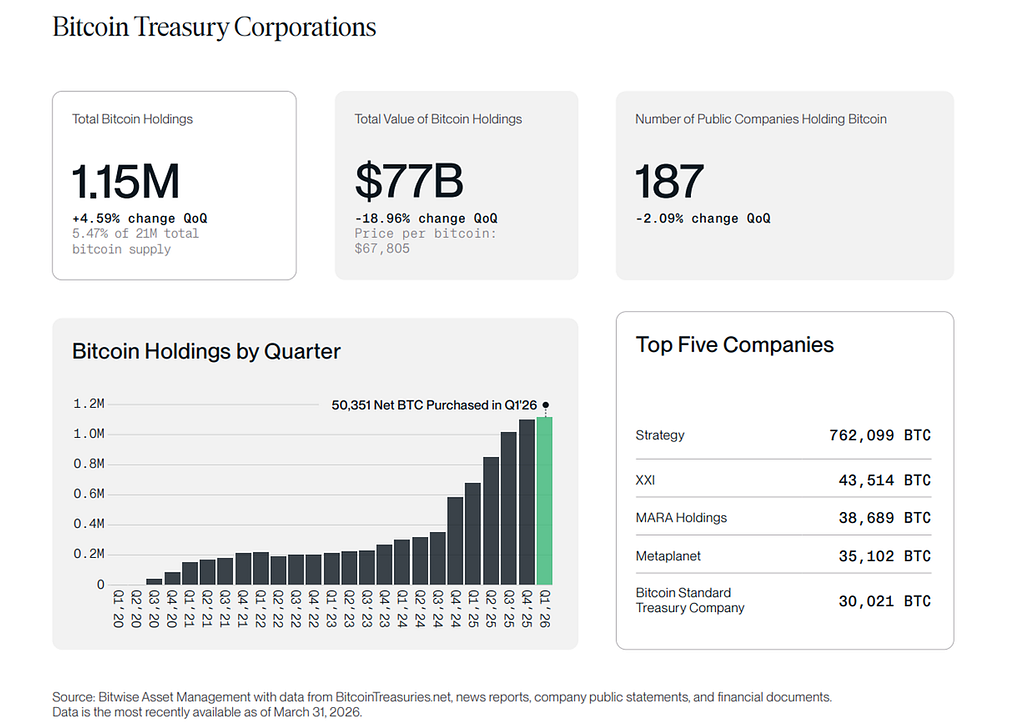

Institutions and Public Companies: The Great Accumulation

1. Accumulation Dynamics

Comparing cycles reveals a massive shift:

- 2022 Bear Market (Q4): Public companies held over 200,000 BTC.

- Current Cycle (Q1 2026): Total BTC on public company balance sheets has exceeded 1.1 million BTC.

This is a five-fold increase in just over three years, highlighting a pivot from aggressive hedging/selling to a long-term “HODL” strategy.

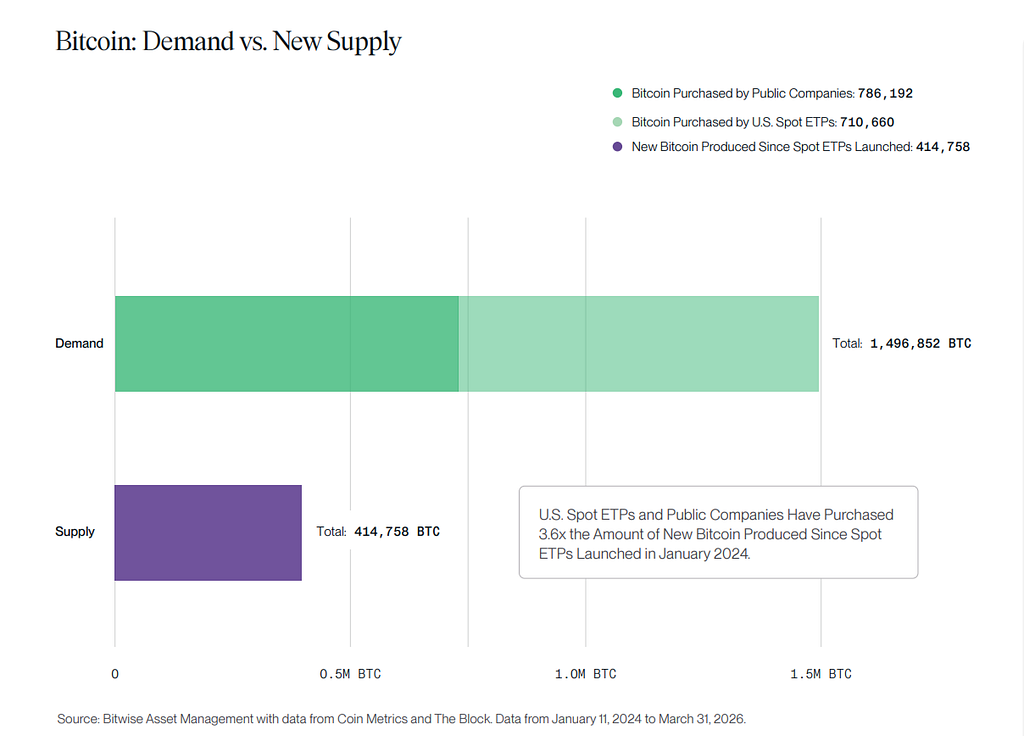

2. Supply and Demand Structure

The institutional demand is now reaching a scale where it dwarfs production:

- Total BTC Demand (Q1 2026): 1.496 million BTC.

- Spot Demand (ETPs/ETFs): ~700,000 BTC (47% of total demand).

- Miner Supply: Only ~400,000 BTC for the same period.

The demand-supply gap will only widen, especially after the 2028 halving, when annual issuance drops to approximately 200,000 BTC.

Insight: Real demand for Bitcoin already exceeds available supply, a reality that institutional players are acutely aware of. They recognize that this disparity will only intensify over time — particularly after the 2028 halving, when annual issuance will be slashed to approximately 200,000 BTC.The fundamental question keeping them occupied is this: How can the massive, long-term demand — primarily driven by retail investors through ETPs and ETFs — be satisfied?As is often the case, the answer is hiding in plain sight. It is already being quietly implemented in the market at this very moment.

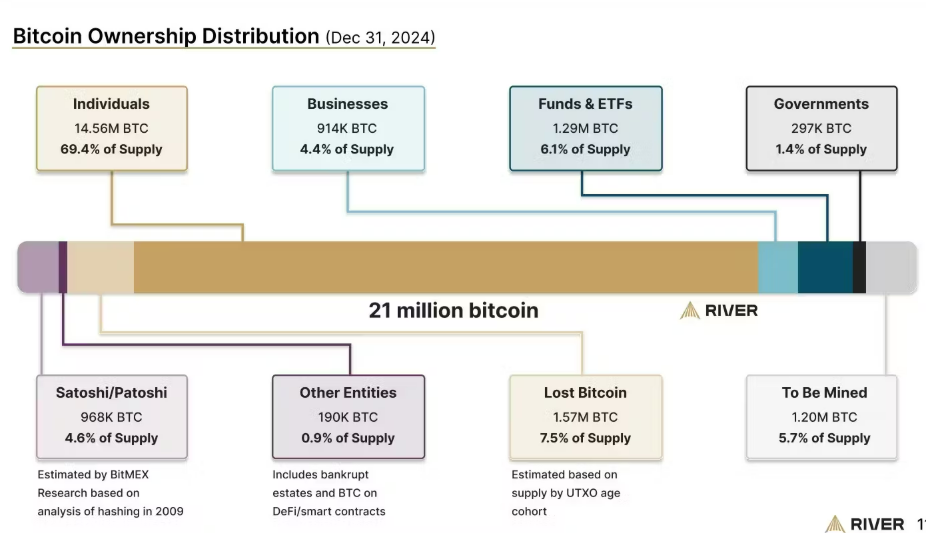

The Strategy: Resolving the Imbalance

Institutional players are looking for a “master supplier” to cover this deficit. Looking at the ownership structure, Individual Investors (including CEXs, DEXs, retail, and miners) hold 69.4% of all Bitcoin.

1. Miner Reserves and Behavior

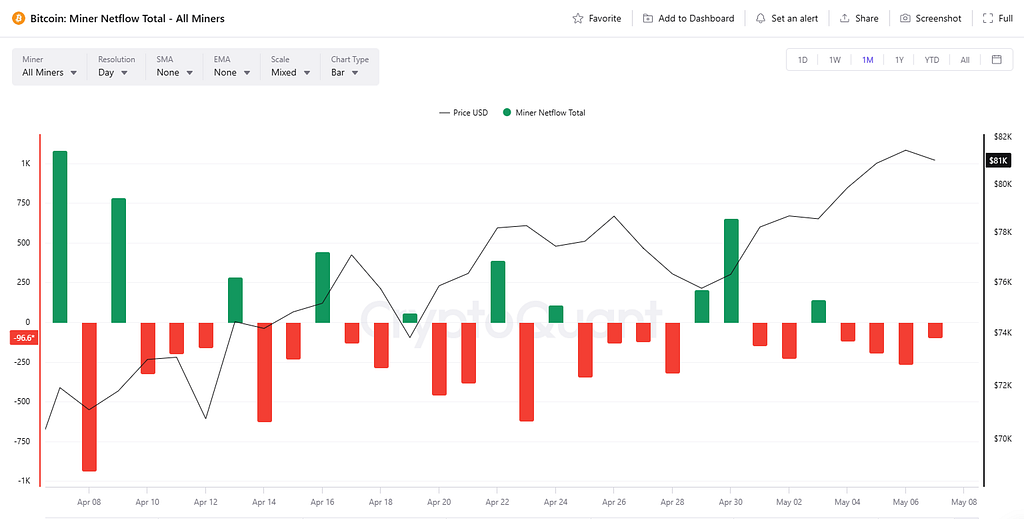

As of early 2026, total miner reserves sit at approximately 1.81 million BTC. On-chain data from CryptoQuant shows a clear trend:

- Declining Reserves: Miner balances dropped to 1.8026 million BTC by May 7, 2026.

- Negative Netflow: Frequent outflows to exchanges in April-May 2026 indicate that miners are selling “stockpiles” (accumulated in previous years) to cover operational overhead, rather than just selling current production.

2. Strategy

As we can observe, throughout the entire price recovery following the $62,000 level, miners have been actively selling off their reserves. It is crucial to emphasize the word “reserves” — this refers not to current production, but to previously accumulated BTC held on their balance sheets.

Even despite relatively high prices (compared to 2022–2023 levels), most miners continue to fix profits and reduce their holdings rather than accumulate. This indicates they consider current prices sufficient to liquidate a portion of previously stored capital, especially against the backdrop of high production costs and the urgent need to cover operating expenses.

This behavior differs sharply from previous cycles and signals a fundamental shift in strategy: miners no longer strive to maintain large reserves on their balance sheets in an environment of high costs and uncertainty.

Today, the market functions through a very tight cooperation between institutional capital and the mining sector. If we return to the beginning of our report and recall the hashrate dynamics and difficulty levels, a rather compelling picture emerges.

- On one hand, the network is controlled by mining companies that possess both a technological and financial edge due to institutional backing. We clearly see the network being held within a specific difficulty range — effectively maintaining a high barrier to entry for new players. This creates artificial conditions for the idling of less efficient miners, forcing them to burn through their accumulated reserves to cover costs.

- On the other hand, institutional players, who have already amassed a significant supply, can act as the primary force capable of swaying the market and shaping demand through ETPs and ETFs.

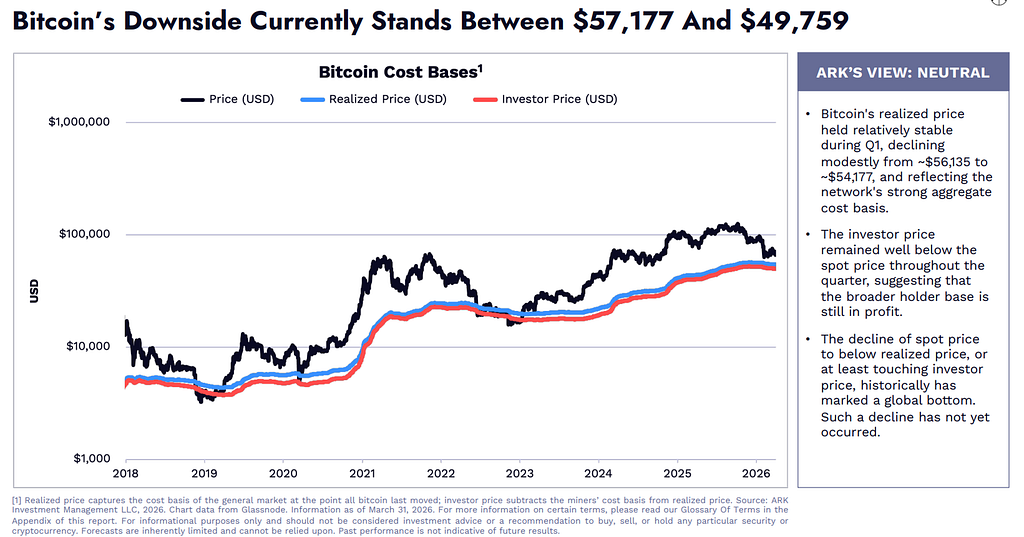

A recent report provided an intriguing analysis of average BTC realization prices, showing a telling range: from $49,759 to $57,177. This suggests that the execution of the final distribution strategy is still far from completion.

Fresh updates confirming this strategy:

- Reserve Liquidations: Miners continue to aggressively sell BTC holdings to cover expenses. Specifically, in January 2026, Core Scientific planned to liquidate nearly all of its holdings, while Riot sold 1,818 BTC as early as December 2025.

- New Hardware: The first half of 2026 expects a mass deployment of the Bitmain S23 and SEALMINER A3 series with energy efficiency under 10 J/TH, which will further squeeze inefficient players out of the market.

Insight: This is the strategy in its purest form — a structural flushing of reserves, stretched out over time. In this game, time is entirely on the side of institutional players. Every week of downtime, every month of negative or zero margin for less efficient miners, exerts additional pressure on their balance sheets. They are forced to sell previously accumulated BTC to cover operating costs, debt, and equipment depreciation.

Meanwhile, institutional players and their affiliated mining companies gain a double advantage: they control the hashrate, keep difficulty in a comfortable range, gradually accumulate BTC at acceptable prices, and displace weaker players from the market.

This is not a classic capitulation with a sharp hashrate crash, but a controlled, systemic redistribution of Bitcoin from old miners into “stronger hands” — institutional players and public companies with access to cheap capital and AI infrastructure.

Final Conclusion

The Bitcoin mining industry in 2026 is undergoing more than just a correction; it is a structural transformation. The winners will not be those who mine the most BTC today, but those who have the best access to capital, cheap energy, and alternative revenue streams (AI/HPC). The market clearly shows: the era of “a little for everyone” is ending. An era of concentration and professionalization is arriving. And at this very moment, a quiet but massive redistribution of Bitcoin is taking place — moving from weak hands to strong ones.

Bitcoin Mining Reveals: Why Institutions Don’t Want Bitcoin’s Supercycle Yet was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.