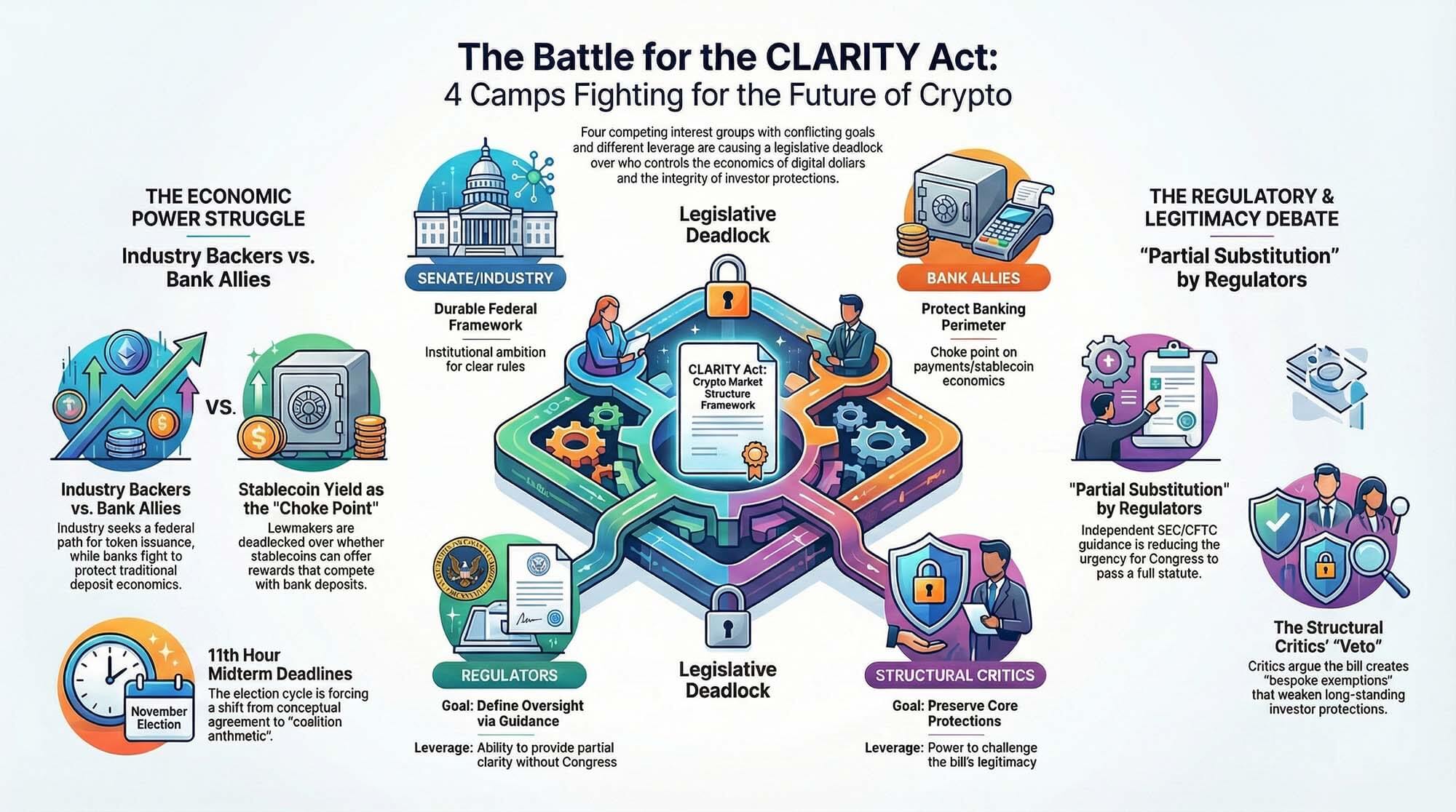

The CLARITY Act entered Washington as a bid to impose a durable market structure on crypto. It now sits at the center of a four-way fight over who gets to define that structure, who gets paid inside it, who supervises it, and how much of the existing financial rulebook survives the rewrite.

The bill still includes broad language for jurisdictional clarity, with the Senate Banking Committee majority outlining a framework that draws lines between the SEC and the CFTC while adding tailored disclosures and anti-fraud protections.

Around that frame, the coalition has fractured into four camps with different definitions of success. Senate and industry backers still want a federal market-structure bill that gives crypto firms a workable path into US regulation.

Bank-aligned critics want to seal off stablecoin yield and keep deposit economics from migrating out of the banking system. Regulators have begun moving through their own channels, with the SEC and CFTC signing a new memorandum of understanding and the SEC issuing a fresh interpretation of crypto assets that begins to deliver some of the clarity Congress had reserved for itself.

Structural critics still argue the bill would carve crypto out of core investor protections, a case advanced by groups such as Better Markets and by former CFTC Chair Timothy Massad in prior congressional testimony.

That collision changed the shape of the bill. What began as a question of statutory design has become a contest over bargaining power.

Each camp can slow the process, each camp can claim some version of consumer protection, and each camp enters the next phase with a different source of leverage. Senate and industry backers hold the broadest institutional ambition.

Why this matters: The CLARITY Act was intended to anchor crypto within US law, with clear rules for exchanges, tokens, and custody. If it stalls or narrows, firms remain in a patchwork regime shaped by enforcement and agency guidance, while banks retain tighter control over dollar-based financial activity. The outcome will determine whether crypto can compete directly with traditional deposits and payment rails, or operate inside a more constrained perimeter.

Related Reading

Related Reading

CLARITY Act deadline in weeks could kill stablecoin earnings and push money into Bitcoin

A Senate breakthrough on CLARITY could formalize a US market structure in which Bitcoin becomes the clearest institutional winner.

Mar 31, 2026 · Gino MatosBanks and their allies hold a choke point around payments, economics, and stablecoin rewards. Regulators hold the power of partial substitution, because every piece of interpretive guidance from the SEC and CFTC narrows the pool of uncertainty that once made CLARITY the singular prize.

Structural critics hold a veto over the debate on legitimacy because their argument speaks to a long-standing Washington fear that crypto bills could create bespoke exemptions that would replace the exemptions older laws once carried.

The calendar tightened the pressure. In January, Senate Banking Chairman Tim Scott said the committee would postpone its markup while bipartisan negotiations continued.

Later that month, the Senate Agriculture Committee advanced related market-structure legislation, keeping momentum alive while underlining that the main bottleneck had shifted into the negotiating room.

By March, the fight over stablecoin rewards had become the central pressure point in the bill, with public reporting and congressional chatter converging on the same conclusion: a framework bill could move forward only if lawmakers found a way to reconcile crypto’s push for broader utility with banking concerns about disintermediation and deposit competition.

That left CLARITY in a familiar Washington posture, broad enough to attract coalitions in theory, specific enough to trigger fracture once the revenue lines came into view.

The first two camps are fighting over the economic core of the bill. The first camp still sees CLARITY as the vehicle that can finally anchor crypto market structure in federal statute.

That camp includes Senate Republicans who have spent months arguing that the industry needs rules written through Congress rather than through case-by-case enforcement, along with a large swath of the industry that wants a lawful path for token issuance, exchange activity, brokerage, custody, and participation in decentralized networks.

The core attraction has always been the same. A federal framework promises a clearer allocation of authority among agencies, a more predictable compliance process, and a narrower zone of ambiguity about what falls under securities law and what falls under commodities regulation.

The Senate Banking majority’s summary reflects that approach, leaning on the idea that a single framework can impose definitional order on a market that has spent years operating inside regulatory overlap.

For crypto firms, the appeal runs deeper than process. A statute holds out the prospect of capital formation under rules that institutions can underwrite, boards can sign off on, and legal teams can defend without having to rebuild the analysis around every enforcement cycle.

Yield politics turned CLARITY into a fight over the economics of digital dollars

The first camp’s ambition runs straight into the second camp, which has focused the fight around stablecoin yield and the economics of digital dollars. The Bank Policy Institute has made the bank-aligned position unusually plain.

Lawmakers, in that view, need to prevent stablecoin structures from recreating deposit-like products outside the traditional banking perimeter, especially if those products begin passing through rewards or yield that look and feel like interest. Under that logic, the danger is structural.

If tokenized dollars can offer returns or functionally similar incentives at scale, then commercial bank deposits face a new form of competition, payments activity migrates, and the prudential perimeter gets thinner exactly where regulators spent years trying to harden it. That is why the stablecoin rewards fight turned into the bill’s main choke point.

It is the place where market structure meets balance-sheet politics.

Those two camps can still describe their goals with overlapping language. Both can say they want consumer protection, operational integrity, and a framework that channels crypto activity into supervised forms.

The overlap ends when the discussion reaches who captures the economics created by digital dollars. The industry camp wants enough room for product development, distribution, and economic pass-through to make federally compliant crypto businesses worth building.

The bank-aligned camp wants a bright barrier around any feature set that could pull value from deposits into tokenized alternatives. That conflict reaches beyond one provision.

It shapes how lawmakers think about payments, exchange design, brokerage economics, wallet architecture, and the degree of freedom crypto firms would have to compete with institutions that already dominate dollar intermediation. Every concession made to one side tends to drain utility from the bill as imagined by the other.

The result is a negotiation whose formal subject is market structure and whose real center of gravity is control over monetary rails. That is why this phase of the CLARITY debate feels more compressed and more political than the earlier debate over jurisdiction.

Jurisdiction can be split in text. Economic control creates winners and losers with organized lobbies, committee relationships, and a direct financial interest in the final wording.

The first camp still wants a durable federal framework. The second camp wants that framework shaped tightly enough that it does not redraw the economics of digital money in a way that benefits crypto firms at the expense of banks.

Both camps can live with progress. Each one defines progress differently, and that difference is what keeps the bill from moving forward.

The third camp sits within the regulatory apparatus itself and introduced a fresh complication into the bill by moving ahead with practical coordination and interpretive guidance. On March 11, the SEC and CFTC announced a new memorandum of understanding designed to improve coordination on crypto oversight.

Days later, on March 17, the SEC issued a new interpretation clarifying how federal securities laws apply to crypto assets, with the CFTC aligning publicly with the effort. By March 20, the CFTC had added crypto-related FAQs that continued the same line of work.

Those actions did not write a statute, and they did not resolve every contested edge case, yet they changed the terrain around CLARITY in a way lawmakers can feel. Congress had been negotiating a bill designed to provide clarity.

Regulators started supplying pieces of that clarity themselves.

Regulators are shaping the field while structural critics keep the legitimacy fight alive

That shift created two immediate effects. First, it gave industry participants some of the operational breathing room they had been seeking, particularly regarding how certain crypto activities are analyzed through the lens of securities law.

Legal practitioners quickly seized on the importance of the change. In a March 19 analysis, Katten described the SEC and CFTC guidance as a major event for the sector, pointing to a more legible treatment of activities such as airdrops, mining, staking, and wrapping.

Second, the guidance changed congressional leverage. Every increment of clarity delivered through agency action reduces the urgency that once surrounded CLARITY as the exclusive route to order.

That creates a subtle but powerful dynamic. A bill under pressure usually gains energy from scarcity.

Once regulators start producing partial substitutes, lawmakers face a harder sell when they ask wavering factions to make politically costly concessions in the name of a breakthrough.

That shift does not weaken the case for statute across the board. A regulatory interpretation sits lower in the durability hierarchy than a congressional framework, and industry participants with long investment horizons still prefer statutory architecture to agency guidance.

Yet the third camp need not erase the case for CLARITY to affect the negotiation. It only needs to be shown that immediate passage is the only way to restore order.

That is already happening. The more the agencies coordinate, the easier it becomes for lawmakers to accept delay, narrower text, or a compromise version of the bill that settles the most acute fights while leaving some larger structural ambitions for another cycle.

For some senators, that can feel like prudence. For some industry players, it can feel like the center of the bill is being negotiated away in real time.

The regulatory camp also exerts pressure in a second way. It offers a political release valve.

Lawmakers who want to say Washington is making progress on crypto can point to the SEC and CFTC without forcing immediate resolution of every issue inside CLARITY. That lowers the cost of postponement and raises the threshold for what kind of final agreement is worth bringing to the floor.

A bill that once looked indispensable now has to demonstrate added value against the backdrop of agency-led adaptation. That is a difficult standard, especially for a coalition already carrying internal conflict over stablecoin rewards, federal preemption, DeFi treatment, and investor-protection language.

The fourth camp continues to ask the question that lies beneath every crypto bill in Washington: Does this framework integrate the sector into existing law, or does it carve out a special lane that weakens protections the rest of finance still carries?

That concern has animated groups such as Better Markets and has appeared in prior testimony from former CFTC Chair Timothy Massad, who argued that proposals such as CLARITY can create artificial distinctions between securities and commodities in ways that reduce the reach of investor protections.

This camp does not have to win the whole argument to shape the bill. It only has to keep the legitimacy challenge alive.

Once that challenge enters the center of the debate, every provision gets viewed through a second lens. A disclosure regime becomes a question about whether disclosure replaces stronger obligations.

A jurisdictional transfer becomes a question about whether oversight is being softened through classification. A pathway for token markets becomes a question about whether the path relies on exemptions that older sectors would never receive.

This is where the four camps collide most sharply. Senate and industry backers want a framework that firms can use at scale.

Bank-aligned critics want to close off yield dynamics that could pressure deposits and payments economics. Regulators are already showing that some clarity can emerge through agency action, reducing the pressure to accept a broad legislative bargain on weak terms.

Structural critics keep pushing on the question of whether the bill preserves the integrity of long-standing protections. A compromise that satisfies the first camp by preserving broad utility may alarm the second and fourth camps.

A compromise that satisfies the second and fourth camps by tightening the perimeter may leave the first camp with a framework that carries less strategic value. A compromise that leans heavily on regulator-led clarity may satisfy lawmakers seeking incremental progress while leaving industry participants with a less durable settlement.

That is why the final question has become a matter of coalition arithmetic rather than conceptual agreement. All four camps can say they want order.

Their conditions for the order point are in different directions.

Midterm pressure is turning a policy negotiation into coalition arithmetic

The midterm calendar sharpens every one of those contradictions. November imposes deadlines on attention, legislative bandwidth, and political appetite for complex financial legislation, generating cross-pressures within both parties.

As the calendar advances, the value of waiting rises for any camp that thinks the current bargain costs too much. Banks can wait if the alternative is stablecoin economics they dislike.

Structural critics can wait if the alternative is a framework they view as too permissive. Regulators can keep moving within their own lane.

Industry groups can keep arguing that delay carries a cost, yet that message weakens if the agencies continue to supply enough guidance to keep large parts of the market functioning.

The coalition that can pass CLARITY, therefore, needs more than a shared talking point around clarity. It needs a settlement that provides the first camp with enough usable structure, the second camp with enough protection around dollar economics, the third camp with a role that fits the statute rather than competes with it, and the fourth camp with enough assurance that core protections remain intact.

That path is narrow. It is still navigable, although the room for error has tightened.

A workable reconciliation would likely require lawmakers to frame the bill less as a maximal rewrite and more as a disciplined allocation of authority, paired with narrow guardrails on stablecoin rewards and stronger language on anti-fraud, disclosure, and supervisory obligations. Even then, the politics stay hard.

Each camp would have to accept a result that falls short of its preferred endpoint. The first camp would accept tighter limits than many crypto firms want.

The second camp would accept a federal framework that still gives compliant crypto business lines room to grow. The third camp would accept that agency guidance is a bridge into statute rather than a substitute for it.

The fourth camp would accept that integration can occur without dismantling the regulatory perimeter. Whether that bargain is possible before November is now the central test around CLARITY.

The bill can still move. The harder question is whether these four camps can converge on a version of movement that each side can live with once the votes are counted.

The post A four-way deadlock is now blocking the US Clarity Act crypto bill — and each side can stop it appeared first on CryptoSlate.