114 Million Reasons

The numbers don’t lie: What Nubank’s 114 million customers mean for the rest of the fintech-MVNO convergence thesis.

Mike McLaren6 min read·Just now

Mike McLaren6 min read·Just now--

Mike McLaren · 6 min read · April 2026

Introduction

In my previous article entitled “Africa Didn’t Follow. It Led”, I argued that Africa did not follow the fintech-MVNO convergence — it originated it. Mobile money, bank-embedded MVNOs, and the migration of the switching cost is already underway. The continent built the conceptual template before the term “fintech-MVNO” even existed in the Western vocabulary.

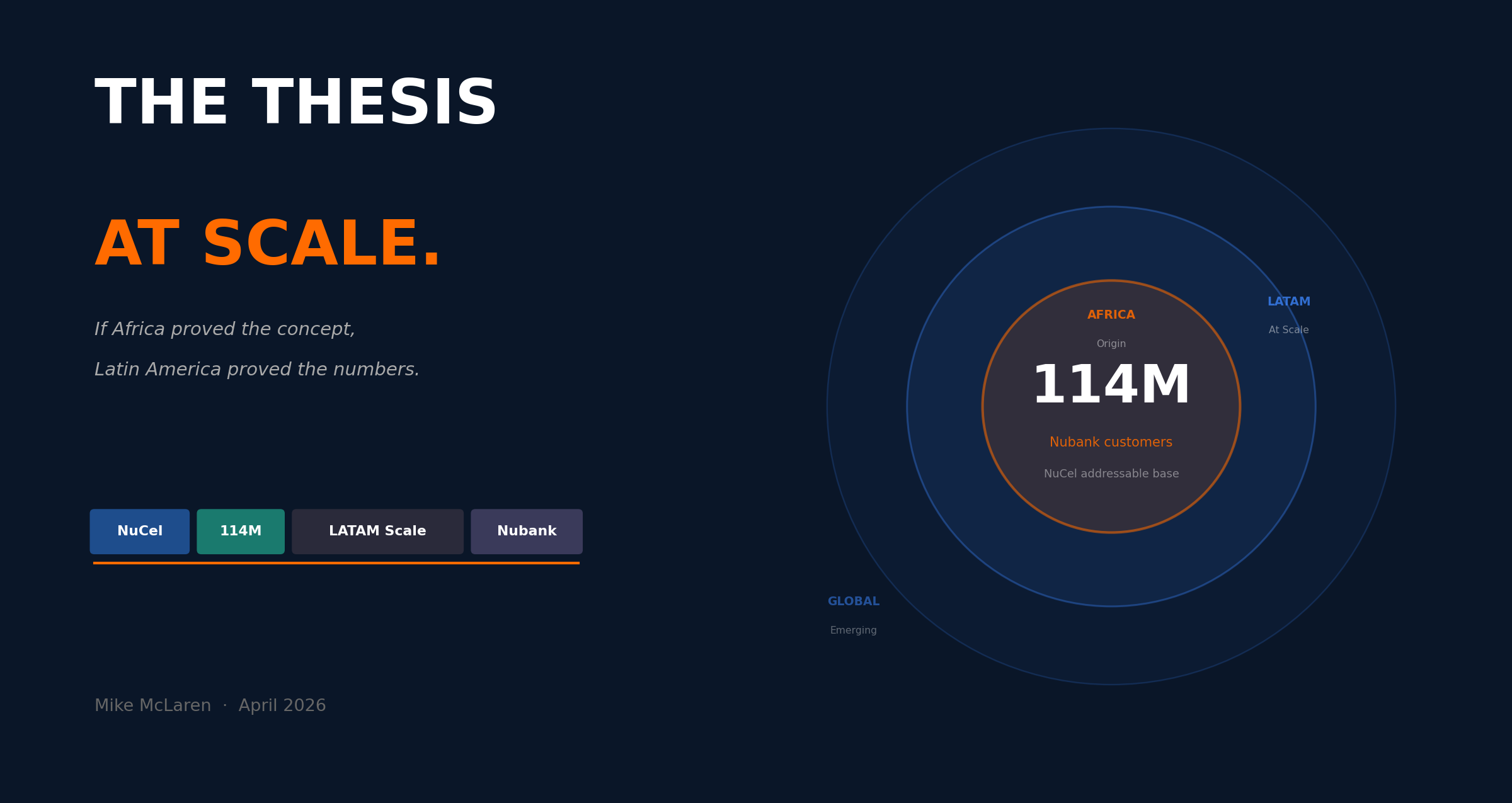

But origination and scale are vastly different arguments. Whereas Africa proved the model works, Latin America (LATAM) is now proving how large it can get.

In October 2024, Nubank — the world’s largest digital bank by customers — launched NuCel, its own MVNO service, on Claro Brasil’s 5G network, covering 93% of Brazil. Their potential customer base exceeds 114 million people.

This is not just a fintech experimenting with mobile and connectivity, but one of the most important neobanks in the developing world making a very deliberate structural move — from financial services platform to mobile operator to, eventually, something that looks less like a bank and more like a complete operating system for its customers’ financial lives.

It is also the clearest single data point that this article series has produced. If you needed an example to demonstrate that the fintech-MVNO convergence is not a niche phenomenon or a market-specific anomaly, this is it. This is not a startup, or a pilot. This is the world’s largest digital bank by customers, building its own mobile network, in the tenth largest economy in the world.

The progression that the fintech-MVNO thesis predicted

Nubank’s path to NuCel was not an impulsive decision as, in May 2024, it had already launched a travel eSIM product — a limited, low-commitment stepping stone that let it test connectivity as one of its product categories without the full regulatory and operational overhead of an MVNO. That product ran on Gigs .

Five months later, NuCel launched as a full MVNO on Claro Brasil’s 5G network. A further nice months after that, in July 2025, Nubank added a physical SIM option. Physical SIMs are not a technological necessity in 2026, but they are a statement about who Nubank is building for. They mean Nubank is targeting the segment of its customer base that has not yet made the leap to eSIM — which in Brazil is still the majority.

The progression from travel eSIM to full MVNO, then physical SIM is precisely the migration the fintech-MVNO convergence thesis predicts. A fintech tests connectivity at the margins, it validates commercial demand, and it deepens the product. Each step moves the switching cost upward, and each step makes the customer relationship stickier.

The regulatory response by the National Telecommunications Agency (Brazil) (ANATEL) confirmed the direction of travel. On August 7, 2025, ANATEL’s Board of Directors voted to permit an exclusivity clause in the agreement between Claro Brasil and NuCel, overruling its own technical staff, who had initially opposed it. The ruling locked the partnership in at the regulatory level and confirmed that NuCel is a structural commitment in Brazil.

What LATAM contributes that Africa does not

What Africa contributed was origination: the proof that mobile and financial services could converge before anyone in the West had a word for it. What LATAM contributes is something entirely different. LATAM validates this convergence across a different economic context at a scale that makes the commercial logic undeniable.

Brazil is the tenth largest economy in the world. Yet before Nubank launched in 2013, roughly 30% of Brazilians were unbanked. Five large incumbents dominated the sector, charging some of the highest banking fees anywhere in the world. Digital transactions accounted for just 54% of all banking operations in 2014. Nubank didn’t enter a sophisticated digital banking market. It built one.

That context matters for what NuCel currently represents. The 114 million customers Nubank has accumulated were not waiting for a SIM card. They were people who had been failed by their financial system and won, one by one, by a company that gave them something better. The MVNO move is the next step in a customer relationship that Nubank constructed from scratch, in a country that had every structural reason to resist it.

That breadth is this argument. The fintech-MVNO convergence is not a product of African necessity or European experimentation, but rather a structural response to where value consolidates in a world where the mobile phone is the primary financial interface for a customer — and that logic holds true across income levels, regulatory environments, and market structures.

OXIO’s consumer research adds a data point worth considering: more than 20% of American consumers say they would buy their mobile plan directly from their bank. This is not an emerging market, and not from a mobile money provider. This is in the United States, from a bank. The consumer appetite for this convergence is not limited to geography. It has become universal.

The infrastructure architecture in LATAM

Behind NuCel’s growth, though, lies an infrastructure debate that has not yet been fully surfaced in Africa or Western markets, and introduces a question that will likely shape the industry for the next decade.

In the Western market, the dominant MVNE architecture is the carrier-partnership model. Gigs , for example, partners with MNOs — AT&T, Vodafone — and provides its API-first platform on top of those relationships. The model is highly portable geographically, capital-light, and extremely fast to deploy. Its value is entirely in the software.

OXIO, ranked number one in Juniper Research’s MVNO in a Box Market 2026–2030 report, takes a fundamentally different approach. Founded in 2018 with offices now in New York, Mexico City, Montreal, and Colombia, OXIO owns its own carrier-grade core network — Packet Core, IMS, and Messaging Core, all cloud-native. It is not brokering access to someone else’s infrastructure because it is the carrier.

Strategically, this is an important distinction. Because OXIO owns the core, it can offer wholesale pricing that carrier-partnership platforms cannot match, deeper network-level feature access, and a structural cost advantage that compounds with scale. OXIO surpassed two million activated lines in 2025. The unit economics improve with every additional line on the platform.

The trade-off though is the capital intensity and geographic concentration. Building and operating a core network is expensive, and it does not travel easily. Gigs’ model scales geographically; OXIO’s model compounds economically within its footprint. They are serving overlapping customer segments from fundamentally different infrastructure positions — and in the markets where OXIO has established its network, that owned-core model appears to offer structural advantages the carrier-partnership model cannot easily replicate.

OXIO’s Latin American traction offers a preview of what that compounding looks like in practice. OXIO cites one unnamed LATAM fintech unicorn that was processing nearly one million monthly mobile top-up transactions through its banking app — and has since converted those to its own branded MVNO — removing the intermediary entirely and owning the customer relationship from the point of connectivity. That is the distribution control argument from article 3 in this series, playing out in the infrastructure layer itself.

This is not a settled debate. It is the central tension of the infrastructure layer, and LATAM is where it is truly highlighted.

What the argument looks like now

Africa is where the model was born, but LATAM is where it is being validated at real scale.

The pattern now visible across three geographies — African bank MVNOs running for over a decade, Western API-first platforms powering fintech launches in weeks, and a 114-million-customer Brazilian neobank building its own mobile network from the ground up — is not coincidence. It is convergence. Different paths, different infrastructure, different markets, but the same conclusion.

The SIM card is becoming the anchor for the financial customer relationship, and the companies that own it will capture the customer. The infrastructure that enables them to own it will capture the margin.

The only question left is which infrastructure wins. That is the argument of a future article.

This article forms part of The Fintech-MVNO Convergence series. Next in the series: Southeast Asia — where the super-app has already arrived. Views are my own and not investment advice. Happy to share sources — as always, just ask.